{kind=link}

Dollar and Yen are consolidating this week’s gains in Asian session today. There is no clear sign of topping in both Dollar and Yen. Yet, there is also no follow through buying to push Dollar through main near term resistance against other major currencies. Fed looks on track to start tapering later in the year, but that would very much depend on upcoming economic data. Volatility could surge as we’d have ADP employment today, ISM manufacturing tomorrow, and non-farm payroll on Friday.

Technically, focuses will remain on when Dollar could break through near term resistance levels. Levels to watch include 1.1846 support in EUR/USD, 1.3785 support in GBP/USD, 0.9237 resistance in USD/CHF, 0.7476 support in AUD/USD, and 1.2485 resistance in USD/CAD.

In Asia, at the time of writing, Nikkei is down -0.01%. Hong Kong HSI is down -0.16%. China Shanghai SSE is up 0.24%. Singapore Strait Times is up 1.34%. Japan 10-year JGB yield is up 0.0040 at 0.064. Overnight, DOW rose 0.03%. S&P 500 rose 0.03%. NASDAQ rose 0.19%. 10-year yield rose 0.002 to 1.480.

Fed Waller: Appropriate to start thinking about pulling back some stimulus

Fed Governor Christopher Waller told Bloomberg TV yesterday that “the unemployment rate would have to drop fairly substantially, or inflation would have to really continue at a very high rate, before we would take seriously a rate hike in 2022”. Nevertheless, “I’m not ruling it out,” he added.

The US is now in a “different phase of economic policy,” he noted. Hence, “it’s appropriate to start thinking about pulling back on some of the stimulus.” He’d be “all in favor” to phase out MBS purchases first, as “right now the housing markets are on fire; they don’t need any other unnecessary support.”

“I think everybody anticipates that tapering could move up earlier than when they originally thought,” Waller said. “Whether that’s this year, we’ll see, but it certainly could.”

“I myself would like to see tapering over before we consider raising rates; therefore if you think you may have to raise rates in late ’22 or early ’23, you pretty much want to get tapering done by the end of next year if possible,” he said.

China PMI manufacturing dropped to 50.9 in Jun, PMI non-manufacturing dropped to 53.5

China official PMI Manufacturing dropped slightly to 50.9 in June, down from 51.0, above expectation of 50.7. Production index dropped from 52.7 to 51.9, hitting a four-month low. Total new orders rose from 51.3 to 51.5. But new export orders dropped further from 48.3 to 48.1. Raw material costs eased from 72.8 to 61.2, after the government’s crackdown on prices.

PMI Non-Manufacturing dropped to 53.5, down from 55.2, below expectation of 50.7.

New Zealand ANZ business confidence dropped to -0.6, enormous cost pressures

New Zealand ANZ business confidence dropped to -0.6 in June, down from May’s 1.8. Own activity outlook rose to 31.6, up form 27.1. Looking at some details, export intentions rose form 12.2 to 13.4. Investment intentions rose from 18.9 to 25.5. Cost expectations rose from 81.3 to 86.2. Employment intentions dropped from 20.5 to 19.7. Pricing intentions rose from 57.4 to 62.8. Inflation expectation jumped further from 2.22% to 2.41%.

ANZ said: “The New Zealand economy is stretched, and firms are clearly facing enormous cost pressures. Increasingly, they are planning on raising their prices in response, with little fear evident that demand will collapse as a result. Shortages of labour are driving investment decisions to a greater extent, but it’s confidence in the economic outlook that will always be key here.

With firms keen to invest and employ, and both cost-push and demand-pull factors suggesting strong inflation ahead, it’s past time to unwind the emergency OCR stimulus. We are forecasting the RBNZ to raise the OCR in February next year, but odds are rising that we’ll see hikes this year.”

Elsewhere

Japan industrial production dropped -5.9% mom in May, versus expectation of -1.9% mom. Australia private sector credit rose 0.4% mom in May, versus expectation of 0.1% mom.

UK Q1 GDP final and current account; France CPI and consumer spending, Swiss KOF and economic expectations, Germany unemployment, and Eurozone CPI will be featured in European session.

Later in the day, US will release ADP employment, Chicago PMI and pending home sales. Canada will release GDP, IPPI and RMPI.

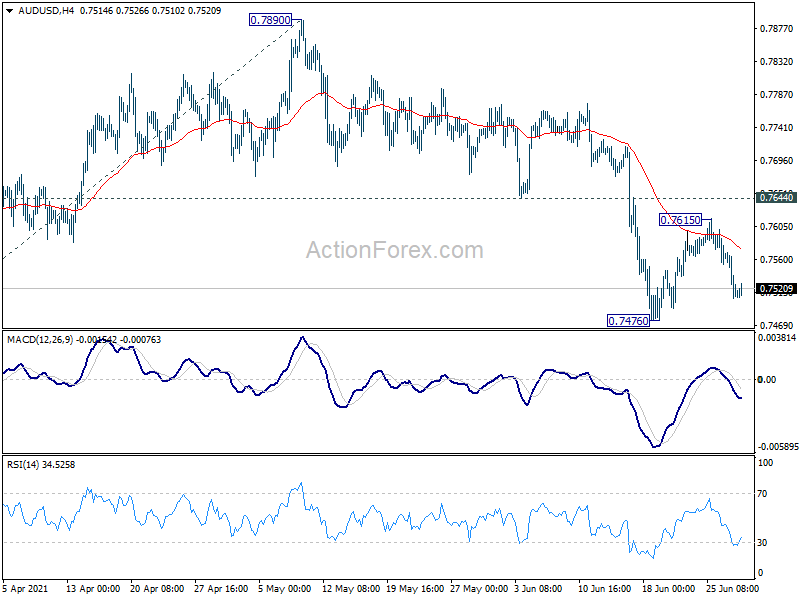

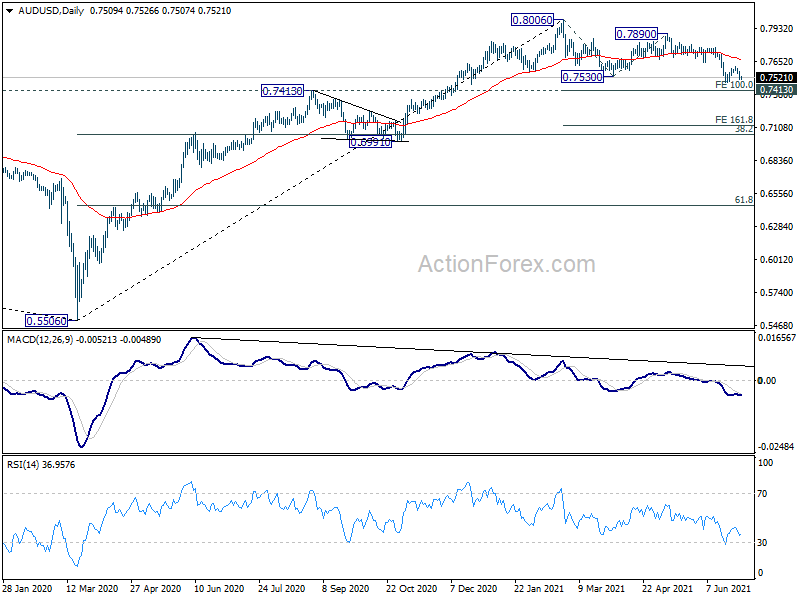

AUD/USD Daily Report

Daily Pivots: (S1) 0.7489; (P) 0.7530; (R1) 0.7552; More…

AUD/USD is staying in range of 0.7476/7615 and intraday bias remains neutral first. On the downside, break of 0.7476 will resume the corrective pattern from 0.8006 towards 100% projection of 0.8006 to 0.7530 from 0.7890 at 0.7414. We’d expect strong support from there to bring rebound. On the upside, break of 0.7644 support turned resistance will turn bias back to the upside for 0.7890 resistance. However, sustained break of 0.7414 will argue it’s at least in larger scale correction, and target 161.8% projection at 0.7120 next.

In the bigger picture, rise from 0.5506 medium term bottom could either be the start of a long term up trend, or a corrective rise. Reactions to 0.8135 key resistance will reveal which case it is. Rejection by 0.8135 key resistance, followed by firm break of 0.7413 resistance turned support, will favors the latter case. Deeper decline would be seen to 38.2% retracement of 0.5506 to 0.8006 at 0.7051 first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y May | -0.70% | -0.60% | ||

| 23:50 | JPY | Industrial Production M/M May P | -5.90% | -1.90% | 2.90% | |

| 01:00 | CNY | Manufacturing PMI Jun | 50.9 | 50.7 | 51 | |

| 01:00 | CNY | Non-Manufacturing PMI Jun | 53.5 | 55.5 | 55.2 | |

| 01:00 | NZD | ANZ Business Confidence Jun F | -0.6 | -0.4 | ||

| 01:30 | AUD | Private Sector Credit M/M May | 0.40% | 0.10% | 0.20% | 0.30% |

| 05:00 | JPY | Housing Starts Y/Y May | 8.30% | 7.10% | ||

| 05:00 | JPY | Consumer Confidence Index Jun | 35.6 | 34.1 | ||

| 06:00 | GBP | GDP Q/Q Q1 F | -1.50% | -1.50% | ||

| 06:00 | GBP | Current Account (GBP) Q1 | -13.8B | -26.3B | ||

| 06:45 | EUR | France CPI M/M Jun P | 0.20% | 0.30% | ||

| 06:45 | EUR | France CPI Y/Y Jun P | 1.80% | 1.80% | ||

| 06:45 | EUR | France Consumer Spending M/M May | 8.90% | -8.30% | ||

| 07:00 | CHF | KOF Leading Indicator Jun | 145.3 | 143.2 | ||

| 07:55 | EUR | Germany Unemployment Change Jun | -16K | -15K | ||

| 07:55 | EUR | Germany Unemployment Rate Jun | 5.90% | 6.00% | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Jun | 72.2 | |||

| 09:00 | EUR | Eurozone CPI Y/Y Jun P | 1.90% | 2.00% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun P | 0.90% | 1.00% | ||

| 12:15 | USD | ADP Employment Change Jun | 600K | 978K | ||

| 12:30 | CAD | GDP M/M Apr | -0.80% | 1.10% | ||

| 12:30 | CAD | Industrial Product Price M/M May | 3.00% | 1.60% | ||

| 12:30 | CAD | Raw Material Price Index May | 2.10% | 1.00% | ||

| 13:45 | USD | Chicago PMI Jun | 70.2 | 75.2 | ||

| 14:00 | USD | Pending Home Sales M/M May | 0.00% | -4.40% | ||

| 14:30 | USD | Crude Oil Inventories | -4.2M | -7.6M |