{kind=link}

Dollar jumps in early US session after strong, record making, PPI inflation data. The worse than expected retail sales and manufacturing data were shrugged off. Yen and Euro are following as next strongest for now. Sterling continues to be weighed down by delay in reopening and it’s trading and worst ones a long with commodity currencies. Though, Canadian Dollar is so far the weakest despite resilience in oil price.

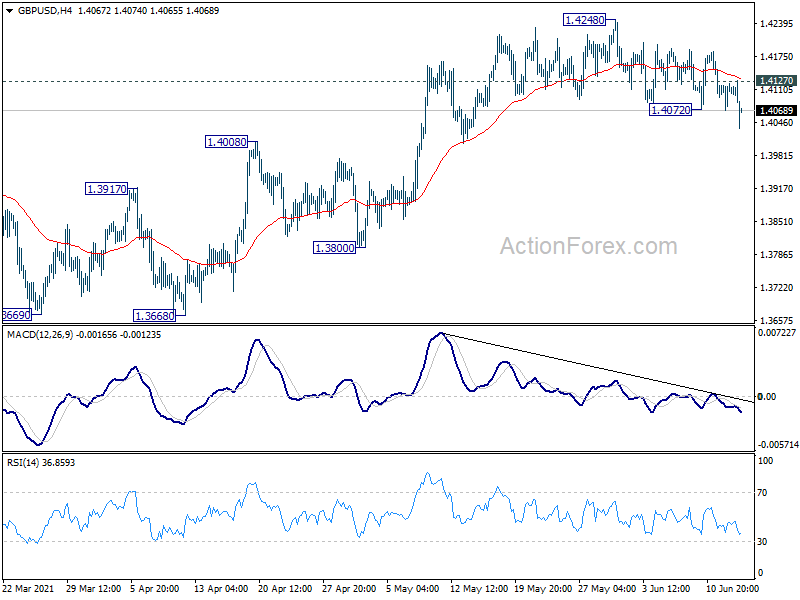

Technically, GBP/USD’s break of 1.4072 support is either a sign of Dollar strength, or Sterling weakness or both. As for the Dollar, break of 1.2201 key near term resistance in USD/CAD would give us more confidence on more sustainable rally in the greenback. As for the Pound, focus will be on 0.8670 minor resistance in EUR/GBP.

In Europe, at the time of writing, FTSE is up 0.47%. DAX is up 0.55%. CAC is up 0.56%. Germany 10-year yield is up 0.0107 at -0.237. Earlier in Asia, Nikkei rose 0.96%. Hong Kong HSI dropped -0.71%. China Shanghai SSE dropped -0.92%. Singapore Strait Times rose 0.69%. Japan 10-year JGB yield rose 0.0082 to 0.049.

US retail sales dropped -1.3% in May, ex-auto sales dropped -0.7%

US retail sales dropped -1.3% mom to USD 620.2B in May, worse than expectation of -0.4% mom. Ex-auto sales dropped -0.7% mom, worse than expectation of 0.5% mom rise. Ex-gasoline sales dropped -1.5% mom. Ex-auto, ex-gasoline sales dropped -0.8% mom. Total sales for March through May period were up 36.2% from the same period a year ago.

US PPI rose 0.8% mom, 6.6% yoy in May, record rise

US PPI for final demand rose 0.8% mom in May, above expectation of 0.6% mom. Annually, PPI accelerated to 6.6% yoy, up from 6.2% yoy, above expectation of 6.4% yoy. That’s also the largest increase since 12-month data were first calculated in November 2010.

PPI less foods, energy and trade services, rose 0.7% mom, above expectation of 0.5% mom. For the 12-month ended in May, PPI accelerated to 5.3% yoy. That’s the largest increase since 12-month data were first calculated in August 2014.

Also released, Empire State manufacturing index dropped to 17.4 in June, down from 24.3, below expectation of 22.5.

ECB Rehn sees no signs of rise in broader price pressures

ECB Governing Council member Olli Rehn said that recent rise in inflation is due to “one-off and temporary factors” only. He added there are currently “no signs of a rise in broader price pressures”, and “slack remains high”. Policymakers need to “look through short-term variation in inflation”.

For now, the ECB “need to continue with significant purchases under PEPP”. The program will be conducted in “flexible manner” and “accommodative financing conditions are key to support euro are recovery”. He added that ECB did not discuss the issue of transitioning away from PEPP yet.

Eurozone exports rose 4.32% yoy, imports rose 37.4% yoy in Apr

Eurozone exports rose 43.2% yoy to EUR 193.8B in April. Imports rose 37.4% yoy to EUR 18.2B. Trade surplus came in at EUR 10.9B, comparing to EUR 2.3% a year ago. Intra-Eurozone trade rose 61.9% yoy to EUR 178.9B.

In seasonally adjusted terms, Eurozone exports dropped -2.4% mom to EUR 193.4B. Imports rose 2.4% mom to EUR 184.0B. Trade surplus narrowed to EUR 9.4B, down from EUR 18.3B, below expectation of EUR 15.2B. Intra-Eurozone trade rose from EUR 171.7B to EUR 177.5B.

Swiss SECO upgrades 2021 GDP forecasts to 3.6%

Swiss government’s Expert Group upgraded GDP growth forecast for 2021 to 3.6% (from March’s 3.0%), as “easing of coronavirus measures has triggered a swift recovery in the domestic economy”. That also means, GDP would climb “well above the pre-crisis level” in H2. Unemployment rate is expected to come to an annual average of 3.1% (March forecast at 3.3%).

For 2022, The Expert Group expect another year of “above-average growth” at 3.3% (unchanged forecast”. It added that foreign trade is set to “stimulate growth substantially again” while services trade such as tourism is “likely to gather pace”. Unemployment rate is expected to drop further to an annual average of 2.8% (March forecast 3.0%).

UK unemployment rate dropped to 4.7% in Apr, still 0.8% above pre-pandemic level

UK unemployment rate dropped to 4.7% in the three months to April, down from 4.8%, matched expectations. That’s still 0.8% higher than the level before the pandemic Nevertheless, it’s -0.3% lower than the previous quarter. Average earnings excluding bonus rose 5.6% 3moy, above expectation of 5.3% 3moy. Average earnings including bonus rose 5.6% yoy, above expectation of 4.9% 3moy. Claimant count dropped -92.6k in May.

RBA discussed four options on bond purchases

RBA reiterated in the June minutes that it will make the decision on 3-year yield target and government bond purchase program at the July meeting. It emphasize “a return to full employment as a priority for monetary policy that would assist with achieving the inflation target”.

It will consider whether to extend the 3-year yield target from April 2024 bond to November 2024 bond. A key considering would be the prospect of having inflation sustainably within the 2-3% target rate some time in 2024.

Four options regarding future bond purchases after completion of the second AUD 100B of purchases in early September were discussed. The options included ceasing the purchases, repeating the AUD 100 purchases for another 6 months, scaling back the amount or spreading over a longer period, and moving to an approach where pace of purchases is reviewed more frequently.

Suggested readings on RBA:

- RBA Minutes Reveal Members Discussed Three Options to Extend QE

- RBA Board Minutes for June Provide Useful Insights into July Decisions

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4077; (P) 1.4100; (R1) 1.4130; More…

GBP/USD’s break of 1.4072 support suggests resumption of fall from 1.4248. Such decline could be the third leg of the pattern from 1.4240. Intraday bias is back on the downside for 1.4008 resistance turned support first. Break till target 1.3668/3800 support zone. On the upside, above 1.4127 minor resistance will turn intraday bias neutral first.

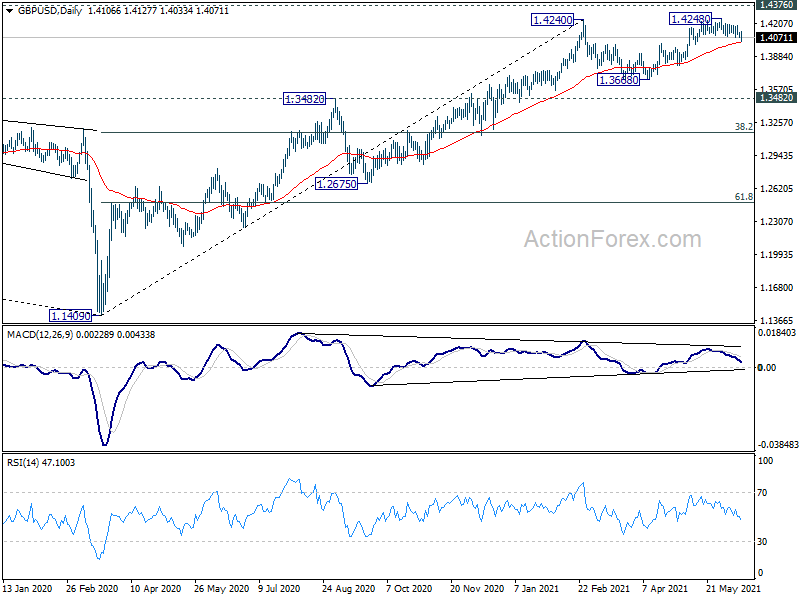

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed and bring deeper fall to 1.2675 support and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | House Price Index Q/Q Q1 | 5.40% | 5.50% | 3.00% | |

| 01:30 | AUD | RBA Minutes | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Apr | -0.70% | -0.40% | 1.10% | |

| 06:00 | GBP | Claimant Count Change May | -92.6K | -15.1K | ||

| 06:00 | GBP | Claimant Count Rate May | 6.20% | 7.20% | 6.40% | |

| 06:00 | GBP | ILO Unemployment Rate (3M) Apr | 4.70% | 4.70% | 4.80% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Apr | 5.60% | 5.30% | 4.60% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Apr | 5.60% | 4.90% | 4.00% | 4.30% |

| 06:00 | EUR | Germany CPI M/M May F | 0.50% | 0.50% | 0.50% | |

| 06:00 | EUR | Germany CPI Y/Y May F | 2.50% | 2.50% | 2.50% | |

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | 9.4B | 15.2B | 13.0B | 18.3B |

| 12:15 | CAD | Housing Starts Y/Y May | 276K | 271K | 269K | 267K |

| 12:30 | USD | Empire State Manufacturing Index Jun | 17.4 | 22.5 | 24.3 | |

| 12:30 | USD | Retail Sales M/M May | -1.30% | -0.40% | 0.00% | 0.90% |

| 12:30 | USD | Retail Sales ex Autos M/M May | -0.70% | 0.50% | -0.80% | 0.00% |

| 12:30 | USD | PPI M/M May | 0.80% | 0.60% | 0.60% | |

| 12:30 | USD | PPI Y/Y May | 6.60% | 6.40% | 6.20% | |

| 12:30 | USD | PPI Core M/M May | 0.70% | 0.50% | 0.70% | |

| 12:30 | USD | PPI Core Y/Y May | 4.80% | 4.80% | 4.10% | |

| 13:15 | USD | Industrial Production M/M May | 0.70% | 0.70% | ||

| 13:15 | USD | Capacity Utilization May | 75.10% | 74.90% | ||

| 14:00 | USD | Business Inventories Apr | -0.10% | 0.30% | ||

| 14:00 | USD | NAHB Housing Market Index Jun | 83 | 83 |