{kind=link}

Trading continued to be rather subdued in Asian session. Major pairs and crosses are staying inside yesterday’s range, as well as last week’s range. Sterling is currently the weakest one, after failing to follow through the rally attempt earlier this week. Dollar is the next weakest for now. On the other hand, Aussie and Swiss Franc are the stronger ones. In other markets, Gold is back below 1900 handle as rally falters. WTI oil is also losing upside momentum after breaching a near term resistance.

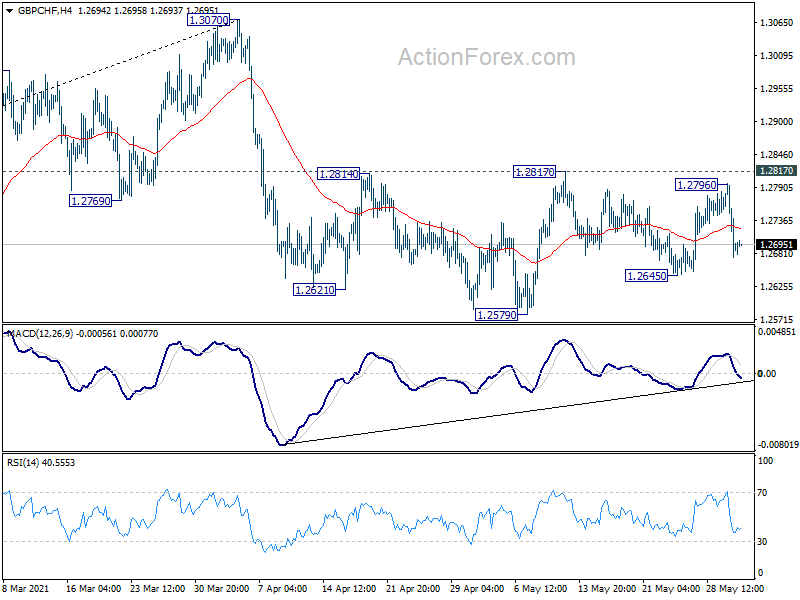

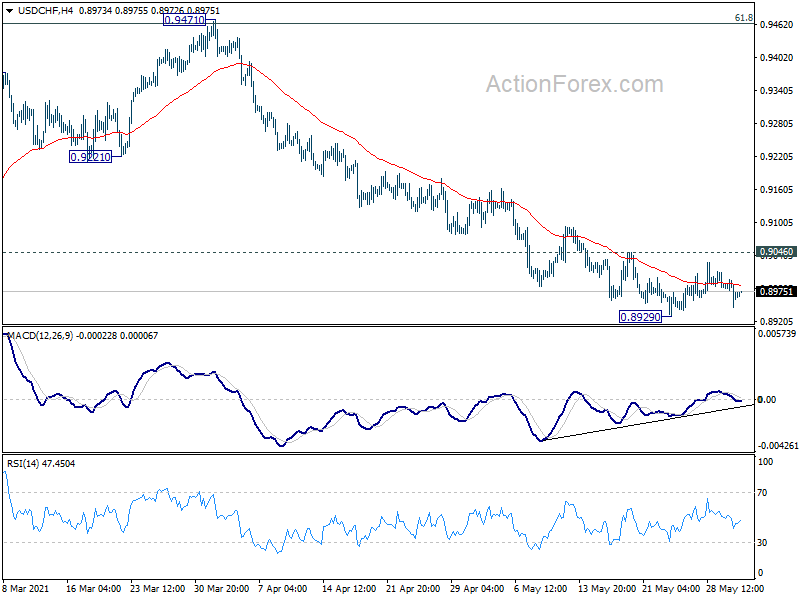

Technically, Swiss Franc will be a focus today, as USD/CHF is heading back to 0.8929 support. Break there will resume the decline from 0.9471 and target 0.8756 low. GBP/CHF is also heading back to 1.2645 minor support, break there will raise the chance that decline from 1.3070 is resuming through 1.2579 low.

In Asia, at the time of writing, Nikkei is up 0.39%. Hong Kong HSI is down -0.50%. China Shanghai SSE is down -0.65%. Singapore Strait Times is down -0.85%. Japan 10-year JGB yield is down -0.0006 at 0.079. Overnight, DOW rose 0.13%. S&P 500 dropped -0.05%. NASDAQ dropped -0.09%. 10-year yield rose 0.034 to 1.615.

BoJ Adachi: Post-pandemic era may give a prime opportunity to achieve inflation target

BoJ board member Seiji Adachi said in a speech, “the post-COVID-19 phase may be an opportunity for the services industry to raise the prices of their services while improving their quality.”

“As Japan’s past deflationary phase is characterized by the fact that there were almost no price rises in the domestic demand-oriented services industry, the post-COVID-19 era may afford a prime opportunity to achieve the 2 percent price stability target,” he added.

Australia GDP grew 1.8% qoq in Q1, recovered to above pre-pandemic levels

Australia GDP grew 1.8% qoq in Q1, above expectation of 1.1% qoq. Through the year, GDP rose 1.1%. Head of National Accounts at the ABS, Michael Smedes said: “With 1.8% growth in the March quarter 2021, Australian economic activity has recovered to be above pre-pandemic levels and has grown 1.1% through the year.”

RBNZ Rayner: Unconventional tools to remain mainstream with low interest rates

RBNZ Head of Financial Markets Vanessa Rayner said in speech, “unconventional” monetary policy tools will “likely remain mainstream for as long as global central bank policy rates remain at, or near record lows”. With the OCR at current low level, RBNZ has “less space” to cut interest rates further. Also, there’s a “limit to how negative rates can go before causing adverse side effects”.

“This means that other tools that utilize the balance sheet have become an important part of the ‘package’ of monetary policy instruments that global central banks have turned to,” she added. The tools can work together in different ways, to “better calibrate an ‘optimal package’ of monetary policy tools in response to future shocks”.

Released from New Zealand, terms of trade index rose 0.1% in Q1, versus expectation of -0.4%.

Fed Brainard: I’m attentive to risks on both sides

Fed Governor Lael Brainard said she’s “attentive to the risks on both sides” regarding the economy now. “I will carefully monitor inflation and indicators of inflation expectations for any signs that longer-term inflation expectations are evolving in unwelcome ways,” she added.

But she added, “while the level of inflation in my near-term outlook has moved somewhat higher, my expectation for the contour of inflation moving back towards its underlying trend in the period beyond the reopening remains broadly unchanged.”

“Relative to the entrenched inflation dynamics that existed before the pandemic, the sharp temporary increases in some categories of goods and services seem unlikely to leave an imprint on longer-run inflation behavior,” she said.

“Today employment remains far from our goal,” she added. “Jobs are down by over 8 million relative to their pre-pandemic level, and the shortfall is over 10 million jobs if we take into account the secular job growth that would have occurred over the past year.”

Looking ahead

Germany retail sales, Eurozone PPI and UK mortgage approvals will be released in European session. Canada will release building permits later in the day. Fed will release Beige Book economic report.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8948; (P) 0.8974; (R1) 0.9000; More….

USD/CHF is staying in range above 0.8929 and intraday bias remains neutral at this point. Outlook stays bearish with 0.9046 resistance intact. On the downside, break of 0.8929 will resume the fall from 0.9471, to retest 0.8756 low. However, on the upside, break of 0.9045 will indicate short term bottoming. Intraday bias will be turned back to the upside for stronger rebound.

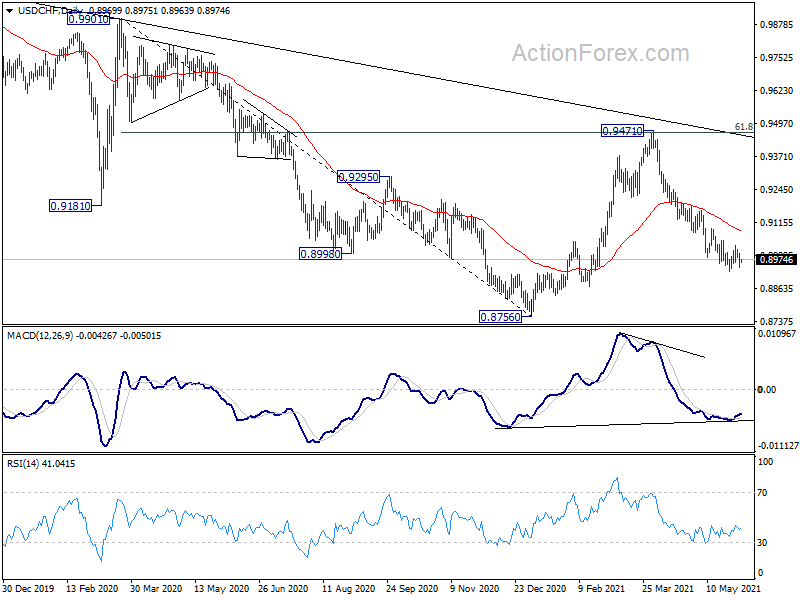

In the bigger picture, prior rejection by 61.8% retracement of 0.9901 to 0.8756 at 0.9464 argues that rebound from 0.8756 was probably just a corrective move. That is, larger down trend from 1.0237 might be still in progress. Medium term bearish is also affirmed as the pair is now far below falling 55 week EMA. Firm break of 0.8756 low will target 61.8% projection of 1.0237 to 0.8756 from 0.9471 at 0.8556 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q1 | 0.10% | -0.40% | 1.30% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Apr | -0.60% | -1.30% | ||

| 23:50 | JPY | Monetary Base Y/Y May | 22.40% | 25.20% | 24.30% | |

| 1:30 | AUD | GDP Q/Q Q1 | 1.80% | 1.10% | 3.10% | |

| 6:00 | EUR | Germany Retail Sales M/M Apr | -2.00% | 7.70% | ||

| 8:30 | GBP | Mortgage Approvals Apr | 85.0K | 82.7K | ||

| 8:30 | GBP | M4 Money Supply M/M Apr | 0.70% | 0.60% | ||

| 9:00 | EUR | Eurozone PPI M/M Apr | 0.90% | 1.10% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Apr | 7.30% | 4.30% | ||

| 12:30 | CAD | Building Permits M/M Apr | 5.70% | |||

| 18:00 | USD | Fed’s Beige Book |