{kind=link}

Trading continue to be relatively subdued as US and UK are both on holiday. Sterling is mildly softer, followed by Dollar, and Swiss Franc. On the other hand, Australian Dollar is strengthening mildly, ahead of RBA rate decision in the upcoming Asian session. It’s highly unlikely for the central bank to alter the forward guidance that, the conditions of a rate hike is unlikely to be met until 2024 at the earliest. But it’s still possible for the Aussie to get some hawkish surprise.

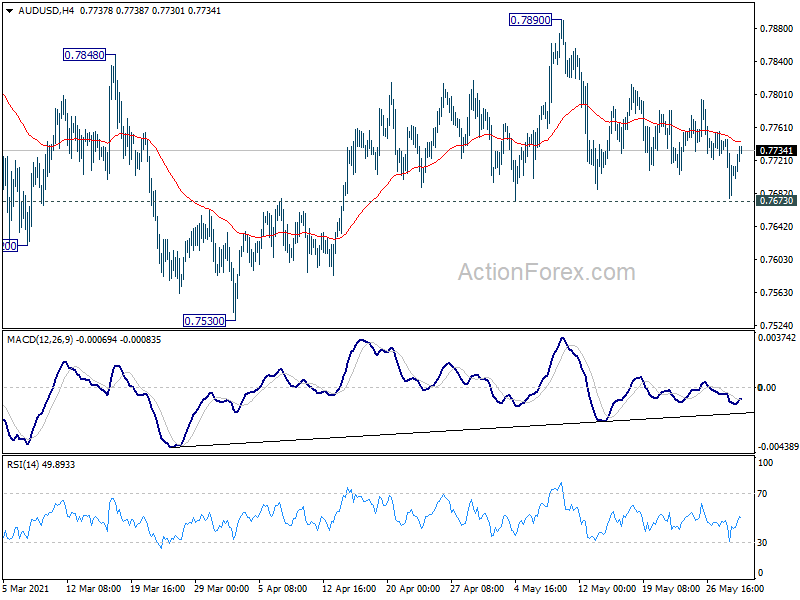

Technically, 0.7673 support in AUD/USD would be the major focus in the upcoming house. As long as this support holds, we’d still expect rise from 0.7530 to resume sooner or later. Break of 0.7890 resistance should confirm underlying buying momentum for a test on 0.8004 high. Such development, if happens, should ideally be accompanied by break of 1.5723 minor support in EUR/AUD to bring deeper fall to 1.5418 support.

Some suggested previews on RBA:

- RBA Preview: RBA to Assess Economic Data and Prepare for Policy Tweak in July

- RBA Could Take A Little More Time As Global Taper Talks Intensify

- Aussie Starts Week Higher, RBA Decision Next

In Europe, at the time of writing, DAX is down -0.28%. CAC is down -0.06%. Germany 10-year yield is up 0.0164 at -0.163. Earlier in Asia, Nikkei dropped -0.99%. Hong Kong HSI rose 0.09%. China Shanghai SSE rose 0.41%. Singapore Strait Times dropped -0.45%. Japan 10-year JGB yield dropped -0.0054 to 0.080.

OECD raises global growth forecast to 5.8% this year, but this is no ordinary recovery

In the new economic outlook report, OECD raised global economic growth forecast to 5.8% this year, a “sharp upwards revision” from December’s projection of 4.2%. It said that “vaccines rollout in many of the advanced economies has been driving the improvement, as has the massive fiscal stimulus by the United States”. Growth is projected to slow to 4.4% next year.

The organization warned that this is “no ordinary recovery” and is likely to “remain uneven and dependent on the effectiveness of vaccination programmes and public health policies.” Some countries like Korea and US are ” reaching pre-pandemic per capita income levels after about 18 months”. But, “much of Europe is expected to take nearly 3 years to recover”. Mexico and South Africa would take between 3 and 5 years.

ECB Visco: Large and persistent rises in interest rates are not justified

ECB Governing council member Ignazio Visco said that “uncertainty over the timing and the strength of the recovery require that financial conditions remain supportive for a long time.”

“Large and persistent rises in interest rates are not justified by the current economic prospects and will be countered,” he emphasized. ECB was ready to make “full use of its already defined bond-buying programme.”

Also release, Eurozone M3 money supply rose 9.2% yoy in April, below expectation of 9.5% yoy.

Japan industrial production rose 2.5% mom, retail sales rose 12% yoy

Japan industrial production grew 2.5% mom in April, below expectation of 4.1% mom. Manufacturers surveyed by the Ministry of Economy, Trade and Industry (METI) expected output to contract -1.7% in May, followed by a 5.0% rebound in June. Retail sales rose 12.0% yoy, below expectation of 15.4% yoy. Over the month, sales dropped -4.5% mom on a seasonally adjusted basis. Housing starts rose 7.1% yoy in April, above expectation of 5.2% yoy. Consumer confidence dropped slightly to 34.1 in May, below expectation of 35.3.

China PMI manufacturing edged lower to 51.0, PMI non-manufacturing rose to 55.2

China official PMI manufacturing dropped slightly to 51.0 in May, down from 51.1, below expectation of 51.1. Looking at some details, production rose 0.5 to 52.7. New orders dropped to 51.3, while raw material inventory dropped to 47.7. New export orders also dropped to 48.2. PMI non-manufacturing rose to 55.2, up from 54.9, above expectation of 52.7.

New Zealand ANZ business confidence rose to 1.8, economy struggling to keep up with demand

New Zealand ANZ business confidence rose to 1.8 in May, up from April’s -2.0, but well below preliminary reading of 7.0. Own activity outlook rose to 27.1, up from April’s 22.2, but below preliminary reading of 32.3.

Looking at some more details, export intentions rose from 9.1 to 12.2. Investment intentions rose from 17.1 to 18.9. Cost expectations rose from 76.1 to 81.3. Employment intentions rose from 16.4 to 20.5. Pricing intentions rose from 55.8 to 57.4.

ANZ said: “The New Zealand economy is struggling to keep up with demand, and cost and inflation pressures continue to build. Firms are having trouble sourcing inputs to production. We wouldn’t read too much into the drop in activity indicators in the second half of the month just yet, as it may have been influenced by Budget uncertainty. We won’t have to wait long to get a fresh read, with the preliminary June data due to be released on 9 June.”

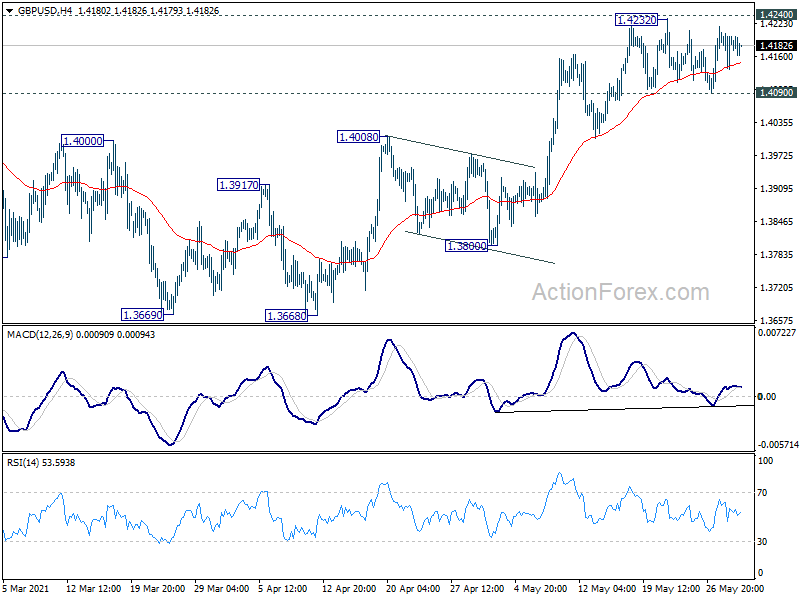

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4146; (P) 1.4178; (R1) 1.4221; More…

GBP/USD is still bounded in consolidation from 1.4232 and intraday bias remains neutral for the moment. Further rise is still in favor with 1.4090 support intact. On the upside, decisive break of 1.4240 resistance will resume larger up trend from 1.1409, for 1.4376 key resistance next. On the downside, though, break of 1.4090 support will extend the consolidation from 1.4240 with another falling leg. Intraday bias will be turned back to the downside for 1.4008 resistance turned support first.

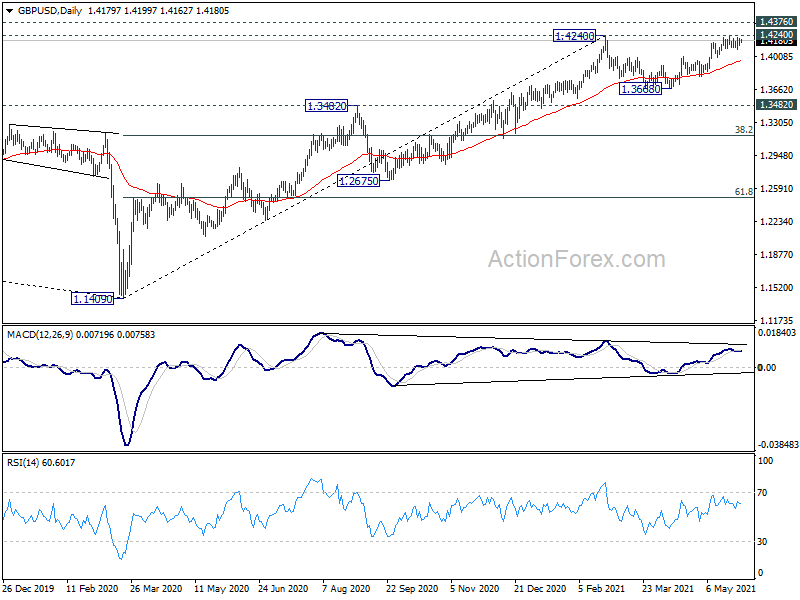

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed and bring deeper fall to 1.2675 support and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Apr P | 2.50% | 4.10% | 1.70% | |

| 23:50 | JPY | Retail Trade Y/Y Apr | 12.00% | 15.40% | 5.20% | |

| 01:00 | CNY | Manufacturing PMI May | 51 | 51.1 | 51.1 | |

| 01:00 | CNY | Non-Manufacturing PMI May | 55.2 | 52.7 | 54.9 | |

| 01:00 | NZD | ANZ Business Confidence May | 1.8 | 7 | ||

| 01:30 | AUD | Private Sector Credit M/M Apr | 0.20% | 0.40% | 0.40% | |

| 05:00 | JPY | Housing Starts Y/Y Apr | 7.10% | 5.20% | 1.50% | |

| 05:00 | JPY | Consumer Confidence May | 34.1 | 35.3 | 34.7 | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | 9.20% | 9.50% | 10.10% | 10.00% |

| 12:00 | EUR | Germany CPI M/M May P | 0.50% | 0.30% | 0.70% | |

| 12:00 | EUR | Germany CPI Y/Y May P | 2.50% | 2.40% | 2.00% | |

| 12:30 | CAD | Industrial Product Price M/M Apr | 1.60% | 0.80% | 1.60% | |

| 12:30 | CAD | Raw Material Price Index Apr | 1.00% | 1.70% | 2.30% | |

| 12:30 | CAD | Current Account (CAD) Q1 | 1.2B | 2.4B | -7.3B |