{kind=link}

Dollar’s selloff resumed overnight after FOMC risk was cleared. Basically, Fed just reaffirmed it’s stance that it’s far from considering stimulus exits. Though, for the week so far, Yen is even weaker with strong rebound in global treasury yields. Euro is no far, follow Dollar as third weakest so far. On the other hand, Canadian Dollar is the top performing, leading other commodity currencies higher.

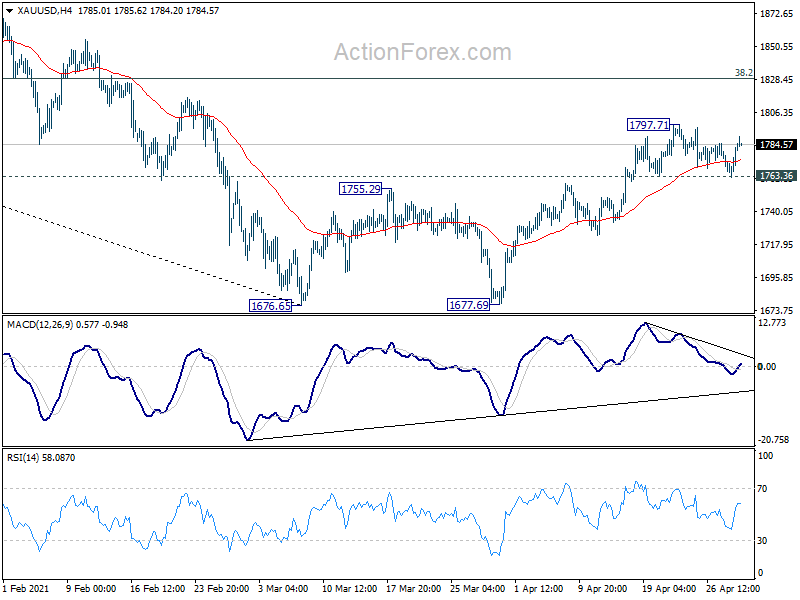

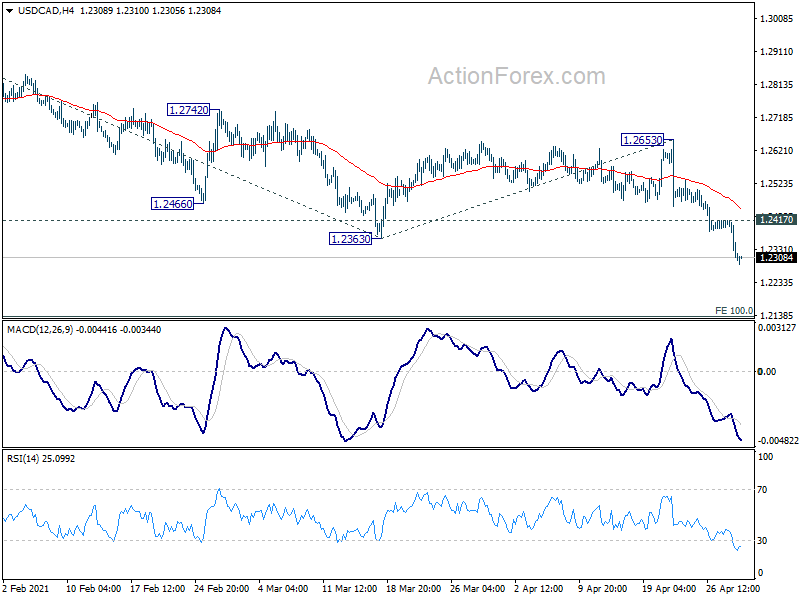

Technically, for Dollar, USD/CHF’s break of 0.9121 temporary suggests resumption of fall from 0.9471. USD/CAD also broke 1.2363 support to resume larger down trend from 1.4667. Focus is back on 108.19 minor support in USD/JPY. Additionally, Gold rebounded comfortably after drawing support from 1763.36. Break of 1797.71 will resume the rise from 1677.69, as another sign of Dollar weakness.

In Asia, at the time of writing, Nikkei is up 0.21%. Hong Kong HSI is up 0.37%. China Shanghai SSE is up 0.20%. Singapore Strait Times is up 0.10%. Japan 10-year JGB yield is up 0.0098 at 0.095. Overnight, DOW dropped -0.48%. S&P 500 dropped -0.08%. NASDAQ dropped -0.28%. 10-year yield dropped -0.002 to 1.620.

Dollar index falls after Fed, on track to retest 89.20 low

Dollar weakened overnight as Fed Chair Jerome Powell indicated in the post meeting press conference that “it is not time yet” to start discussing any change in the monetary policy stance. He added that recovery is “uneven and far from complete.” Fed is still “a long way from our goals” and it’s “going to take some time” to have substantial further progresses.

Powell also talk down the “one-time increases in prices”, as they are “likely to only have transitory effects on inflation.” “We think of bottlenecks as things that in their nature will be resolved as workers and businesses adapt, and we think of them as not calling for a change in monetary policy since they’re temporary and expected to resolve itself,” Powell said. “We know the base effects will disappear in a few months.”

Suggested readings on FOMC:

- Fed Refrained from Giving Any Hint about QE Tapering

- Fed Monitor Review: ‘It Is Not The Time To Start Talking About Tapering’

- April FOMC: A Subtle Change In Tune

- FOMC: Steady As She Goes

Dollar index dropped further to close at 90.60 overnight. Near term outlook stays bearish with 55 day EMA (now at 91.54) intact. Retest of 89.20 should be seen next. Break there will resume larger fall from 102.99.

New Zealand goods exports dropped -2.3% yoy, imports rose 11.0% yoy in March

New Zealand goods exports dropped -2.3% yoy to NZD 5.7B in March. Imports rose 11.0% yoy to NZD 5.6B. Trade surplus narrowed to NZD 33m, down from NZD 201m, matched expectations.

Exports to China was up NZD 423m to NZD 1.8B. But exports to all other top trading partners were down, with USA down NZD -52m, EU down NZD -49m, AU down NZD -105m, Japan down NZD -25m.

Imports from China was up NZD 624m to NZD 1.3B, from EU was up NZD 132m, from AU was up NZD 65m, from Japan was up NZD 19m. But imports from USA was down NZD -74m.

New Zealand ANZ business confidence rose to -2 in Apr, a pretty inflationary soup cooking

New Zealand ANZ Business Confidence rose to -2.0 in April, up from March’s -4.1, much better than preliminary reading of -8.4. Own Activity Outlook rose to 22.2, up from 16.6, versus prelim 16.4. Exports intentions rose to 9.1, up from 4.5. Investment intentions rose to 17.1, up from 11.9. Cost expectations rose to 76.1, up from 73.3. Employment intentions rose to 16.4, up from 14.4. Pricing intentions rose to 55.8, up form 47.3.

ANZ said: “Given supply-side constraints are biting so hard, the confidence and robust employment intentions of firms may represent greater upside to wages and prices than to actual growth. It’s looking like a pretty inflationary soup. The RBNZ will be keen to look through cost-push inflation as far as possible, because it’s temporary…. But there’s clearly plenty of demand and risk-taking out there. The notion that the RBNZ might be overcooking things may well gain some traction in the months ahead, especially with headline inflation expected to rise above 2% in mid-2021.”

Looking ahead

Germany unemployment and CPI flash, Eurozone M3 and economic sentiment indicator will be released in European session. Later in the day, US Q1 GDP will be the main focus, while jobless claims and pending home sales will be featured too.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2278; (P) 1.2348; (R1) 1.2385; More…

USD/CAD drops to as low as 1.2286 so far today. The break of 1.2363 support confirms resumption of whole down trend form 1.4668. Intraday bias stays on the downside for 100% projection of 1.2880 to 1.2363 from 1.2653 at 1.2136. On the upside, above 1.2417 minor resistance will turn intraday bias neutral first. But recovery should be limited below 1.2653 resistance to bring fall resumption.

In the bigger picture, fall from 1.4667 is seen as the third leg of the corrective pattern from 1.4689 (2016 high). Further decline should be seen back to 1.2061 (2017 low). In any case, sustained break of 1.2653 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | 33M | 33M | 181M | 201M |

| 0:00 | NZD | ANZ Business Confidence Apr F | -2.0 | -8.4 | ||

| 1:30 | AUD | Import Price Index Q/Q Q1 | 0.20% | -1.10% | -1.00% | |

| 7:55 | EUR | Germany Unemployment Change Apr | -10K | -8K | ||

| 7:55 | EUR | Germany Unemployment Rate Apr | 6% | 6% | ||

| 8:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 10.20% | 12.30% | ||

| 9:00 | EUR | Eurozone Economic Sentiment Indicator Apr | 103 | 101 | ||

| 9:00 | EUR | Eurozone Consumer Confidence Apr F | -8.1 | -8.1 | ||

| 9:00 | EUR | Eurozone Services Sentiment Apr | -8 | -9.3 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Apr | 4.3 | 2 | ||

| 9:00 | EUR | Eurozone Business Climate Apr | 0.3 | |||

| 12:00 | EUR | Germany CPI M/M Apr P | 0.50% | 0.50% | ||

| 12:00 | EUR | Germany CPI Y/Y Apr P | 1.80% | 1.70% | ||

| 12:30 | USD | Continuing Jobless Claims (Apr 16) | 3.674M | |||

| 12:30 | USD | Initial Jobless Claims (Apr 23) | 560K | 547K | ||

| 12:30 | USD | GDP Annualized Q1 P | 6.50% | 4.30% | ||

| 12:30 | USD | GDP Price Index Q1 P | 1.90% | |||

| 14:00 | USD | Pending Home Sales M/M Mar | 3.50% | -10.60% | ||

| 14:30 | USD | Natural Gas Storage | 38B |