{kind=link}

Euro rises mildly after ECB President Christine Lagarde sounded cautiously upbeat in the post-meeting press conference. Yet, there is no clear follow through buying for an upside breakout yet. Dollar is also not much supported by better than expected jobless claims data. The more notable movement today is the selloff in Sterling, as well as Aussie and Kiwi. But respective pairs are still range bound. Overall, trading is rather directionless.

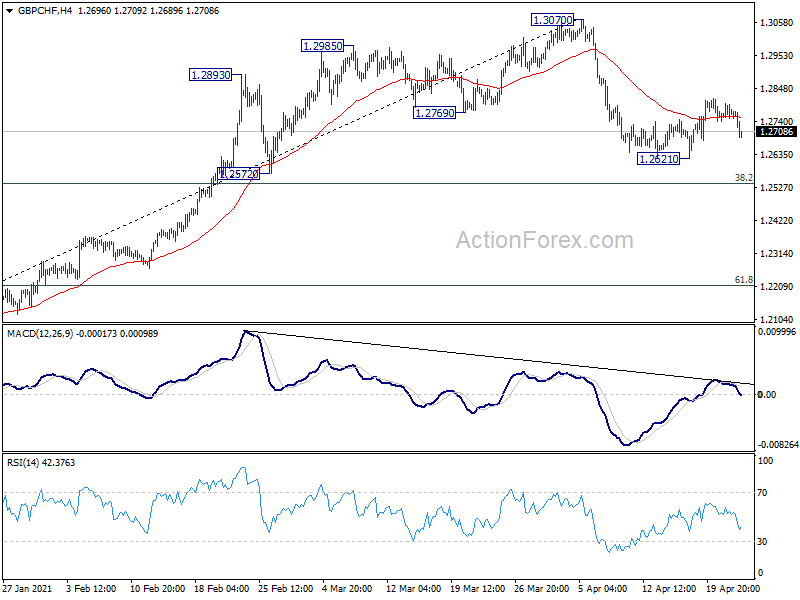

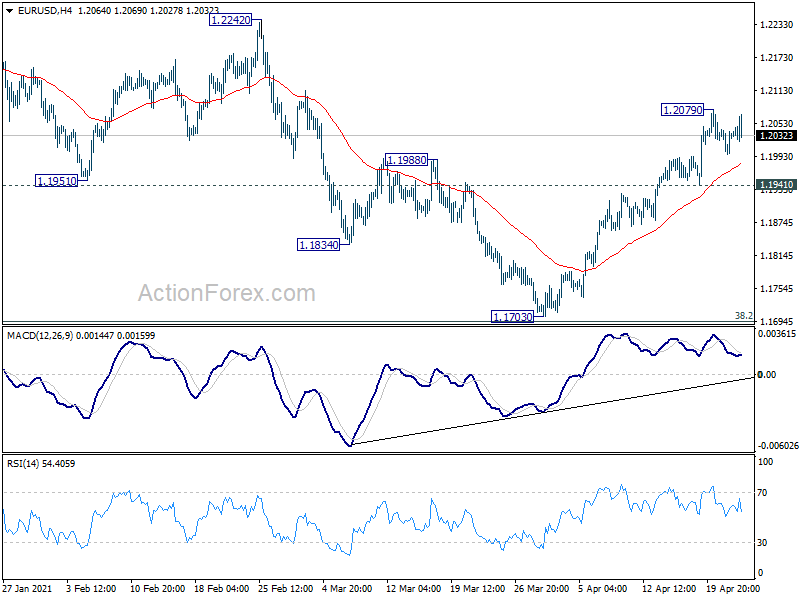

Technically, we’ll now see if EUR/USD can break through 1.2079 temporary top to resume the rebound from 1.1703. Similarly, eyes will be on 130.95 temporary top in EUR/JPY, as well as 0.8718 resistance in EUR/GBP. If Euro does rise further, we’ll also have a look on whether Swiss is taken higher too. Levels to watch include 0.9127 temporary low in USD/CHF and 1.2621 in GBP/CHF.

In Europe, at the time of writing, FTSE is up 0.24%. DAX is up 0.50%. CAC is up 0.59%. German 10-year yield is up 0.003 at -0.256. Earlier in Asia, Nikkei rose 2.38%. Hong Kong HSI rose 0.47%. China Shanghai SSE dropped -0.23%. Singapore Strait Times rose 1.04%. Japan 10-year JGB yield dropped -0.006 to 0.069.

US initial claims dropped to 547k, lowest since March 2020

US initial jobless claims dropped -39k to 547k in the week ending April 17, better than expectation of a rise to 642k. That’s also the lowest level since March 14, 2020. Four-week moving average of initial claims dropped 28k to 651k, lowest since March 14, 2020 too.

Continuing claims dropped -34k to 3674k in the week ending April 10, lowest since March 21, 2020. Four-week moving average of continuing claims dropped -42k to 3713k, lowest since March 28, 2020.

ECB stands pat, reconfirm its very accommodative stance

ECB left monetary policy unchanged and “reconfirm its very accommodative monetary policy stance”. Main refinancing rate, marginal lending facility rate, and deposit rate are held at 0.00%, 0.25%, and -0.50% respectively.

The pandemic emergency purchase programme (PEPP) will continue with an envelop of EUR 1850B, “until at least the end of March 2022”. It also expects PEPP to be carried out at a “significantly higher pace” during the current quarter. ECB also stands ready to “recalibrated” the envelop if required. The asset purchase programme (APP) will continue at a monthly pace of EUR 20B. It will also continue to provide “ample liquidity” through the refinancing operations.

Finally, ECB “stands ready to adjust all of its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner, in line with its commitment to symmetry.”

ECB Lagarde: Progress with vaccinations should pave the way for firm rebound

In the post meeting press conference, ECB President Christine Lagarde said that while Eurozone real GDP could have contracted again in Q1, data pointed to a “resumption of growth” in Q2. Progress with vaccinations, should “pave the way for a firm rebound in economic activity in the course of 2021”.

Near-term risks on growth continue to be “on the downside, but medium-term risks remain “more balanced”. Headline inflation is “likely to increase further in the coming months”, reflecting “changing dynamics of idiosyncratic and temporary factors”. These factors can be expected to “fade out” early next year.

Australia NAB business confidence rose to 17 in Q1, economic recovery built further momentum

Australia NAB quarterly business confidence rose to 17 in Q1, up from 15. Business conditions rose from 11 to 17. Business condition for next 3 months rose form 19 to 26. Business conditions for next 12 months rose form 24 to 31. Next 12-month capex plans rose from 31 to 34, highest level since mid 1990s.

Alan Oster, NAB Group Chief Economist: “The survey suggests that the economic recovery built further momentum in Q1. What is particularly welcome is that the improvement is broad-based with conditions and confidence improving in most industries and are at an above-average level in all. Moreover, the lift in trading conditions and profitability over the last two quarters is now being translated into the Survey’s employment indicator”.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2008; (P) 1.2026; (R1) 1.2053; More….

EUR/USD is staying in range below 1.2079 temporary top and intraday bias stays neutral first. Further rally is expected with 1.1941 minor support intact. As noted before, correction from 1.2348 should have completed with three waves down to 1.1703. Break of 1.2079 will target 1.2442/2348 resistance zone. However, break of 1.1941 will argue that the rebound from 1.1703 has completed, and turn bias back to the downside for this support.

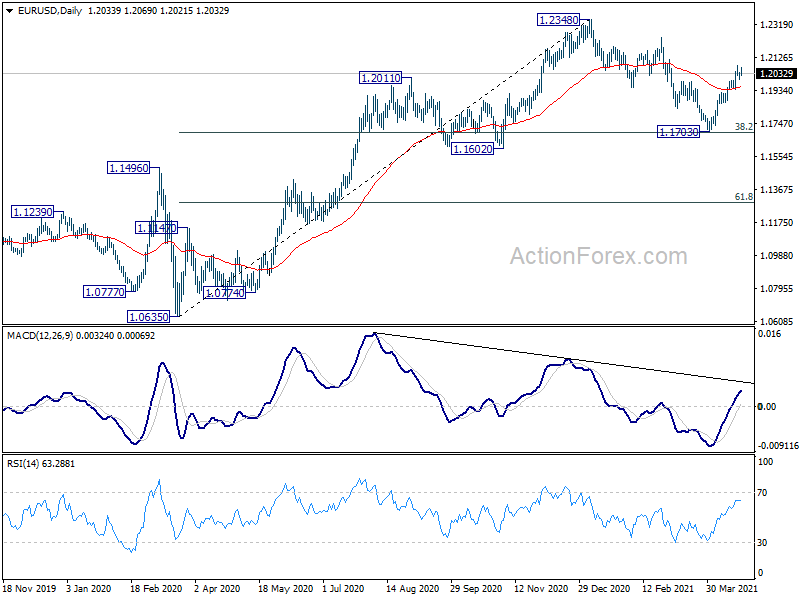

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. However, sustained break of 1.1602 will argue that whole rise from 1.10635 has completed. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q1 | 17 | 14 | 15 | |

| 06:00 | CHF | Trade Balance (CHF) Mar | 5.82B | 4.12B | 3.70B | |

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | CAD | New Housing Price Index M/M Mar | 1.10% | 1.80% | 1.90% | |

| 12:30 | USD | Initial Jobless Claims (Apr 16) | 547K | 642K | 576K | 586 K |

| 14:00 | USD | Existing Home Sales Mar | 6.20M | 6.22M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Apr P | -11 | -11 | ||

| 14:30 | USD | Natural Gas Storage | 47B | 61B |