{kind=link}

Yen rebounds notably overnight, following the pull back in stocks. Market sentiment was weighed down by renewed concerns over coronavirus infections, which also dragged down oil prices. Dollar also followed and recovered. On the other hand, commodity currencies reversed their earlier gains. Overall, Yen is currently the strongest for the week so far, followed by Sterling. Canadian Dollar is the worst, as BoC tapering is awaited, followed by Aussie and Dollar.

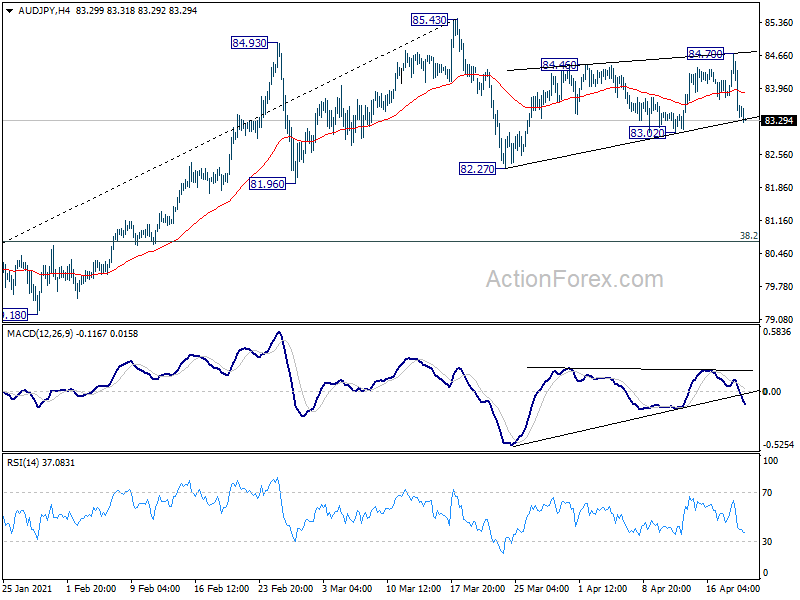

Technically, the developments in Yen crosses are a bit of a drama. AUD/JPY’s sharp reversal yesterday suggests that it’s still it could indeed be starting the third leg of the correction from 85.43. Break of 83.02 support will bring deeper fall to 82.27 support and below. To double confirm selloff in Yen crosses, 129.56 minor support in EUR/JPY, 149.36 support in GBP/JPY, and 76.64 support in NZD/JPY will be watched.

In Asia, Nikkei is down -2.04%. Hong Kong HSI is down -1.63%. China Shanghai SSE is up 0.15%. Singapore Strait Times is down -1.26%. Japan 10-year JGB yield is down -0.0152 at 0.069. Overnight, DOW dropped -0.75%. S&P 500 dropped -0.68%. NASDAQ dropped -0.92%. 10-year yield dropped -0.039 to 1.562.

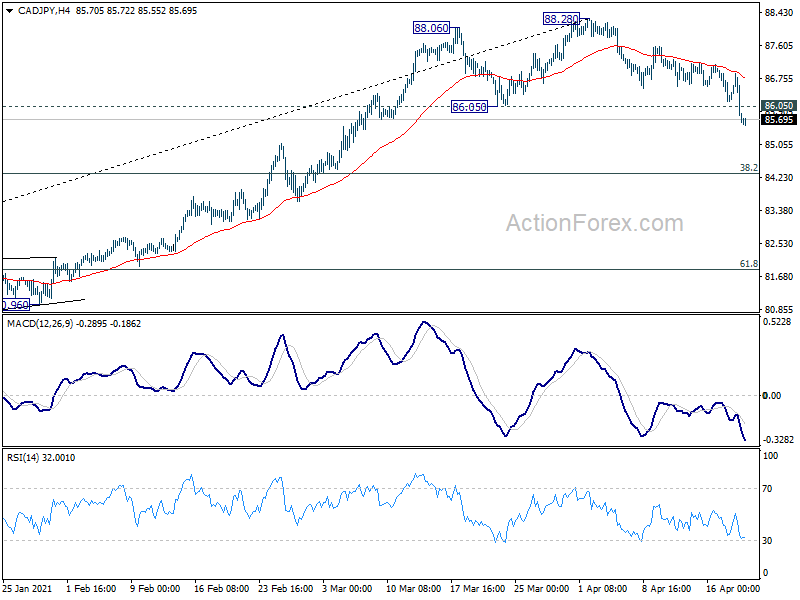

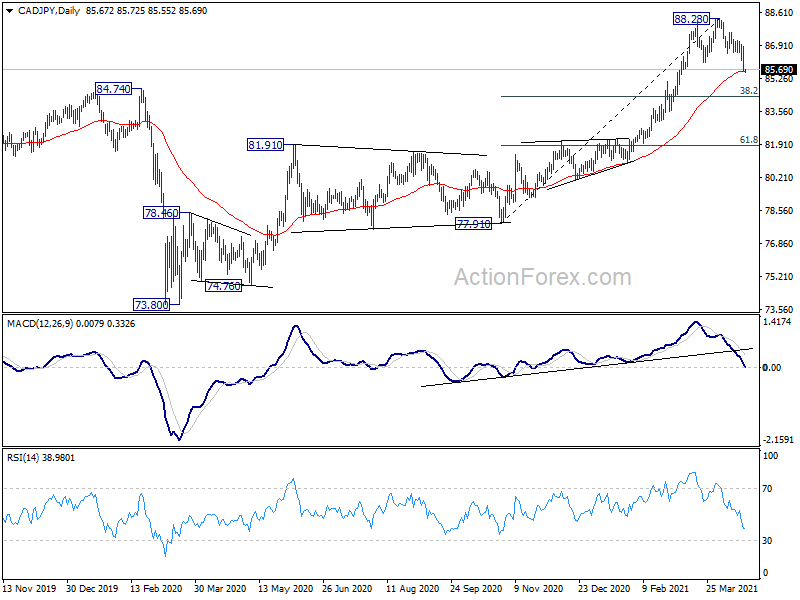

CAD/JPY extends correction as BoC tapering awaited

BoC is widely expected to become the first major central bank to scale back monetary stimulus today. It would announce to its asset purchases to CAD3B/week, from CAD4B/week previously. Overnight rate will be held at effective lower bound of 0.25%. The central will also likely revise up its economic projections.

The main question is whether the more optimistic outlook would prompt a change in the forward guidance. BoC had indicated that the policy rate will stay unchanged “until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved”, and this would unlikely happen until 2023. A better economic outlook might lead the members to see slack be absorbed earlier than 2023.

Here are some previews:

- BOC Preview – Expects Upgrades on Economic Forecasts and More Optimistic Forward Guidance

- Bank of Canada Policy Meeting: A Bond Tapering Story

- Will a Bank of Canada Taper Lift CAD?

Canadian Dollar is currently the weakest one for the week, even worse than the greenback. Tapering of asset purchase was well priced in already. If there is no significant upgrade in the outlook, we’d expect CAD’s correction to continue. CAD/JPY’s break of 86.05 support overnight suggests that deeper correction in underway. Near term bearishness is also affirmed by rejection by 4 hour 55 EMA. We’d now expect deeper fall to 38.2% retracement of 77.91 to 88.28 at 84.31.

Australia retail sales rose 1.4% mom in Mar, led by Victoria and Western Australia

Australia retail sales rose 1.4% mom, or AUD 423.9m, in March. Over the year, sales was up 2.3% yoy. The rises were led by Victoria (4%) and Western Australia (5.5%), with both states rebounding from COVID-19 lockdown restrictions during February. Queensland, which saw COVID-19 restrictions impact March 2021, saw a minor fall.

New Zealand CPI rose 0.8% qoq, 1.5% yoy in Q1

New Zealand CPI rose 0.8% qoq in Q1, matched expectations. Annually, CPI accelerated to 1.5% yoy, up from 1.4% yoy. Looking at some details, the rises in prices were led by transport, which rose 3.9% qoq, biggest quarterly rise in over a decade. Rent prices rose 1.0% qoq, biggest quarterly rise in a year.

Elsewhere

UK CPI and PPI will be released in European session. Canada will release CPI too, in addition to BoC rate decision.

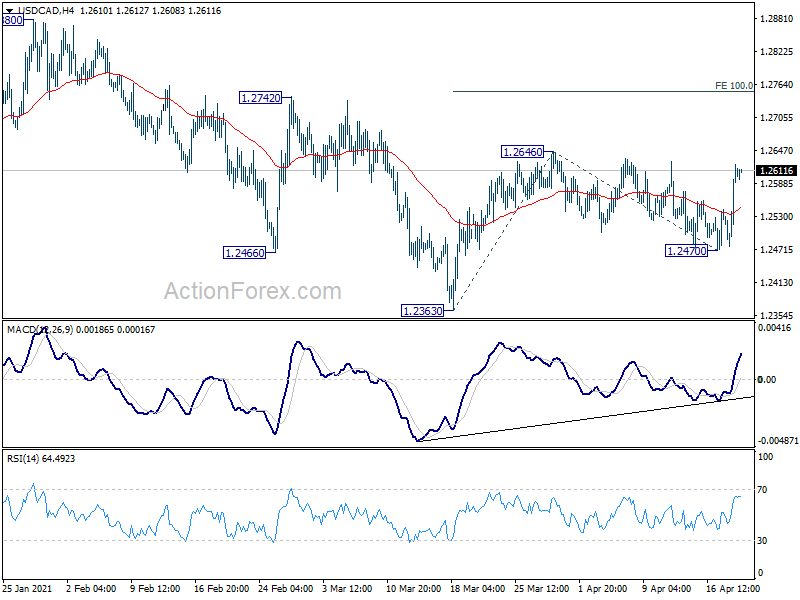

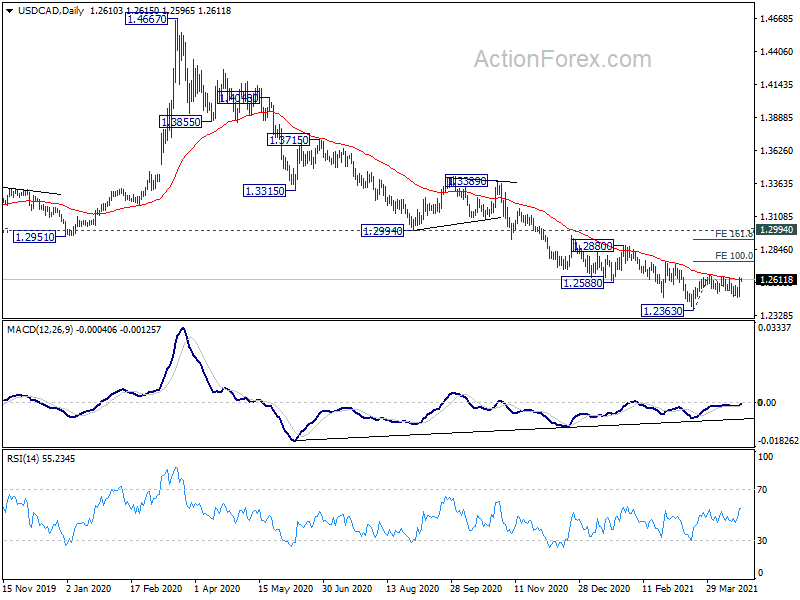

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2522; (P) 1.2572; (R1) 1.2666; More…

Intraday bias in USD/CAD is turned neutral with the current rebound, and focus is back on 1.2646 resistance. Sustained break there would also have 55 day EMA firmly taken out. That would indicate that USD/CAD is in a larger scale rebound. Intraday bias will be back on the upside for 100% projection of 1.2363 to 1.2646 from 1.2470 at 1.2753, and then 161.8% projection at 1.2928. Meanwhile, break of 1.2470 support will bring retest of 1.2363 low instead.

In the bigger picture, fall from 1.4667 is seen as the third leg of the corrective pattern from 1.4689 (2016 high). Further decline should be seen back to 1.2061 (2017 low). In any case, break of 1.2994 support turned resistance resistance is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 0.80% | 0.80% | 0.50% | |

| 22:45 | NZD | CPI Y/Y Q1 | 1.50% | 1.00% | 1.40% | |

| 0:30 | AUD | Westpac Leading Index M/M Mar | 0.38% | 0.02% | ||

| 1:30 | AUD | Retail Sales M/M Mar P | 1.40% | 0.80% | -0.80% | |

| 6:00 | GBP | CPI M/M Mar | 0.30% | 0.10% | ||

| 6:00 | GBP | CPI Y/Y Mar | 0.70% | 0.40% | ||

| 6:00 | GBP | Core CPI Y/Y Mar | 1.00% | 0.90% | ||

| 6:00 | GBP | RPI M/M Mar | 0.30% | 0.50% | ||

| 6:00 | GBP | RPI Y/Y Mar | 1.50% | 1.40% | ||

| 6:00 | GBP | PPI Input M/M Mar | 0.60% | |||

| 6:00 | GBP | PPI Input Y/Y Mar | 2.60% | 2.60% | ||

| 6:00 | GBP | PPI Output M/M Mar | 0.30% | 0.60% | ||

| 6:00 | GBP | PPI Output Y/Y Mar | 1.70% | 0.90% | ||

| 6:00 | GBP | PPI Core Output M/M Mar | 0.10% | |||

| 6:00 | GBP | PPI Core Output Y/Y Mar | 1.40% | |||

| 12:30 | CAD | CPI M/M Mar | 0.60% | 0.50% | ||

| 12:30 | CAD | CPI Y/Y Mar | 2.30% | 1.10% | ||

| 12:30 | CAD | CPI Common Y/Y Mar | 1.30% | |||

| 12:30 | CAD | CPI Median Y/Y Mar | 2.00% | |||

| 12:30 | CAD | CPI Trimmed Y/Y Mar | 1.90% | |||

| 14:00 | CAD | BoC Rate Decision | 0.25% | 0.25% | ||

| 14:30 | USD | Crude Oil Inventories | -5.9M | |||

| 15:00 | CAD | BoC Press Conference | ||||

| 17:00 | USD | 20-Year Bond Auction | 2.29% |