{kind=link}

Yen bounces broadly in Asian session session today, after Japan reported solid trade data. Sterling is currently following as second strongest, then Aussie. On the other hand, Euro weakens in general, dragging down the Swiss Franc too. The developments came as Sterling is reversing recent decline against other European majors. Dollar and Canadian are both mixed at the time of writing.

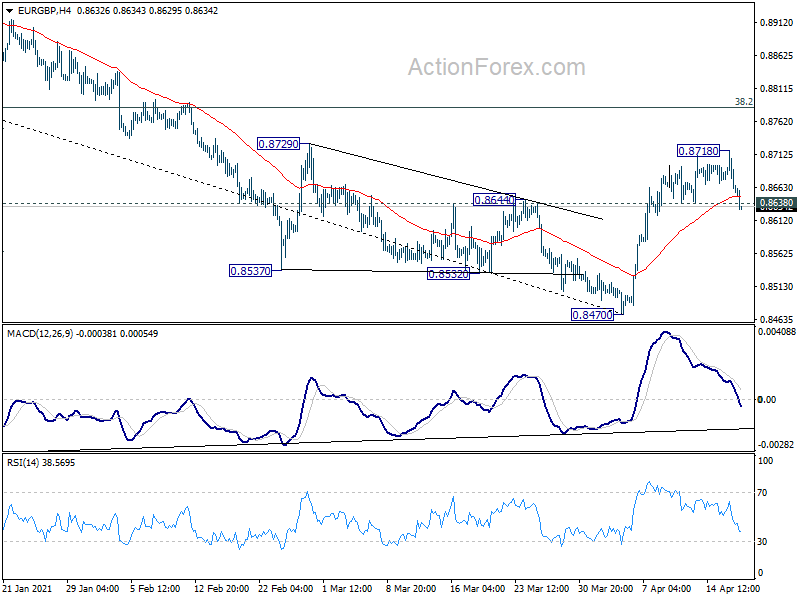

Technically, EUR/GBP’s break of 0.8638 minor support argues that the rebound from 0.8470 has completed much earlier than expected. Deeper fall could be seen back to retest 0.8470. EUR/JPY could now be eyeing 129.56 support. Break will extend the consolidation pattern from 130.65 with another fall towards 128.28 support. Selloff in Euro crosses could in turn keep EUR/USD capped by 1.2 handle.

In Asia, at the time of writing, Nikkei is up 0.15%. Hong Kong HSI is up 0.84%. China Shanghai SSE is up -1.33%. Singapore Strait Times is up 0.23%. Japan 10-year JGB yield is down -0.0032 at 0.087.

Japan exports surged 16.1% yoy in March, imports rose 5.7% yoy

Japan’s exports rose 16.1% yoy in March to JPY 7378B, as led by exports of autos, plastics and non-ferrous metals. That’s the first double-digit annual growth in more than three years. Though, the growth rate was skewed by the low base effect due to the pandemic. Exports to China was up 37.2% yoy, to US up 4.9% yoy, to EU up 12.8% yoy. Imports rose 5.7% yoy to 6714B. Trade surplus came in at JPY 663.7B.

In seasonally adjusted term, exports rose 4.3% mom to JPY 6524B. Imports dropped -0.7% mom to 6226B. Trade balance turned to JPY 298B surplus.

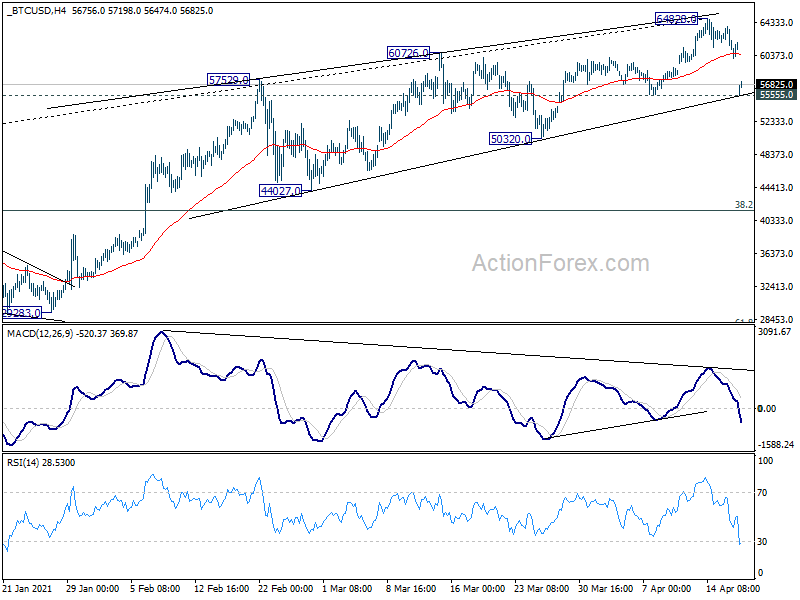

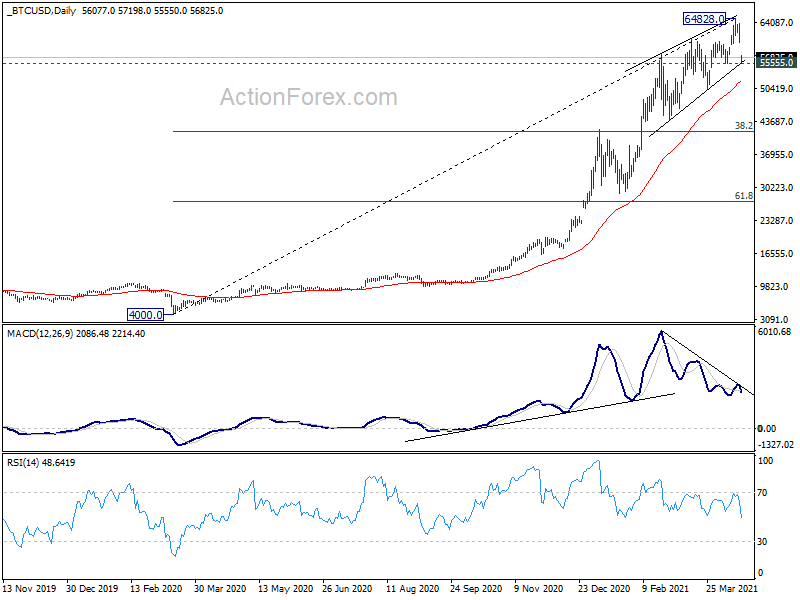

Bitcoin completing terminal triangle, setting up for medium term correction

Bitcoin was in heavy selloff during the weekend, together with other crypto currencies. There’s unconfirmed news that the US Treasury is going to tighten up regulations to crackdown money laundering with digital assets. The selloff was also seen as hangover of Coinbase listing on NASDAQ last week. Some believed it’s related to the blackout in China’s Xinjiang region, which caused almost half of Bitcoin network to go offline in 48 hours.

Technically, the decline wasn’t much a surprise to us. We have been seen price actions from 20283 as developing in to a five-wave terminal triangle. The break through 60726 to 64828 was a bit stronger than expected. But that’s kept by upper trend line of the triangle nonetheless.

Immediate focus is now on 55555 support, which is close to lower trend line of the triangle. Firm break there should confirm the start of a larger correction, to the whole up trend from 4000 (Mar 2020). The eventual depth of the correction would depend on the strength of the interim rebound. But we’d tentatively put 38.2% retracement of 4000 to 64828 at 41591 as target. That’s also close enough to top of prior range of 20283/41964.

BoC to start tapering, ECB likely a non-event

BoC is generally expected to be the first major central to taper asset purchases this week, from the currently CAD 5B per week to CAD 3B per week. As for interest rate, however, it will likely reiterate that overnight rate will remain at the effective lower bound until into 2023. Additionally, new economic forecasts in the MPR will be closely watched.

ECB will also meet this week, but it’s unlikely to provide any new information, given that it has just started to increase the pace of asset purchases significantly this month. Though, the overall tone of President Christine Lagarde could be slightly more upbeat, as Eurozone seems to be weathering the third wave of pandemic rather well. Also to be featured, RBA minutes will likely be a non-event.

On the data front, it’s a big week for the UK, with employment, CPI and PPI, retail sales, and PMIs featured. Japan, Canada and New Zealand will also release CPI. Eurozone will release PMIs too. The calendar will get busier towards the end of the week. Here are some highlights:

- Monday: Japan trade balance; Eurozone current account.

- Tuesday: RBA minutes; Japan tertiary industry activity index; Germany PPI; UK employment.

- Wednesday: New Zealand CPI; Australia retail sales; UK CPI, PPI; Canada CPI, BoC rate decision.

- Thursday: Australia NAB business confidence; Swiss trade balance; ECB rate decision; Canada new housing price index; US jobless claims, existing home sales, leading index.

- Friday: Japan CPI core, PMI manufacturing; UK Gfk consumer confidence, retail sales, public sector net borrowing, PMIs; Eurozone PMIs; US PMIs, new home sales.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8636; (P) 0.8677; (R1) 0.8699; More…

EUR/GBP’s break of 0.8638 minor support suggests that rebound from 0.8470 has completed at 0.8718 already. The failure to sustain above 55 day EMA also keeps near term outlook bearish. Intraday bias is back on the downside for retesting 0.8470 low first. on the upside, above 0.8718 will resume the rebound to 38.2% retracement of 0.9291 to 0.8470 at 0.8784.

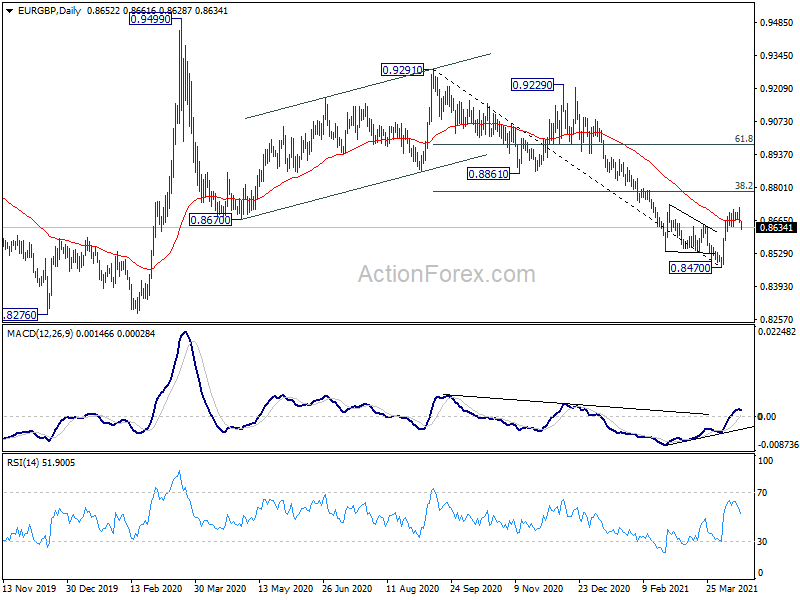

In the bigger picture, we’re seeing the price actions from 0.9499 as developing into a corrective pattern. That is, up trend from 0.6935 (2015 low) would resume at a later stage. This will remain the favored case as long as 0.8276 support holds. However, firm break of 0.8276 support will suggest that rise from 0.6935 has completed and turn medium term outlook bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Price Index M/M Apr | 2.10% | 0.80% | ||

| 23:50 | JPY | Trade Balance (JPY) Mar | 0.30T | 0.20T | -0.04T | -0.01T |

| 4:30 | JPY | Industrial Production M/M Feb F | -1.30% | -2.10% | -2.10% | |

| 8:00 | EUR | Eurozone Current Account (EUR) Feb | 31.2B | 30.5B |