{kind=link}

Dollar turns softer entering into US session, as traders await the results of auctions of both 3- and 10-year bonds, worth USD 96B in total. Additionally, there will be auction of USD 24B of 30-year bonds tomorrow, and a total of USD 151B in bills this week. It should be noted that this year’s strong rally in treasury yield started after a poor 7-year note auction back in February. Reactions to these results could set the tone for yields in Q2.

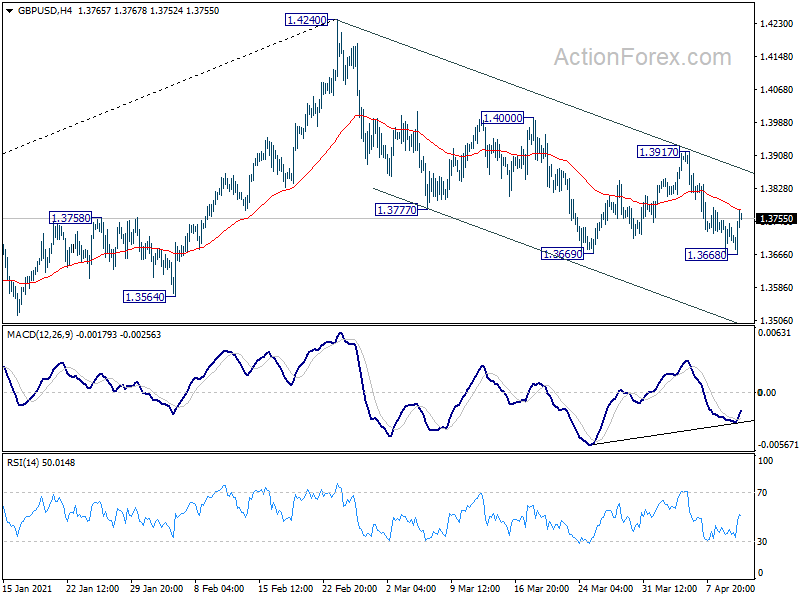

On the other hand, Sterling is currently the strongest one so far, with the held from strong recovery in GBP/USD after breaching 1.3669 support very briefly. Eyes will now be on 0.8620 minor support in EUR/GBP, to gauge whether Sterling is rebounding broadly. Or, attention will also be on 1.1926 temporary top in EUR/USD, to gauge is Dollar’s selloff is resuming.

In Europe, currently, FTSE is down -0.30%. DAX is up 0.12%. CAC is up 0.12%. Germany 10-year yield is up 0.002 at 0.298. Earlier in Asia, Nikkei dropped -0.77%. Hong Kong HSI dropped -0.86%. China Shanghai SSE dropped -1.09%. Singapore Strait Times dropped -0.33%. Japan 10-year JGB yield rose 0.0052 to 0.111.

Eurozone retail sales rose 3.0% mom in Feb, EU rose 2.9% mom

Eurozone retail sales rose 3.0% mom in February, well above expectation of 1.4% mom. Volume of retail trade increased by 6.8% mom for non-food products and by 3.7% mom for automotive fuels, while it decreased by -1.1% mom for food, drinks and tobacco.

EU retail sales rose 2.9% mom. Among Member States for which data are available, the highest increases in total retail trade were registered in Austria (+28.2%), Slovenia (+16.4%) and Italy (+8.4%). The largest decreases were observed in Malta (-1.5%), France and Hungary (both -1.2%).

Released earlier, Japan machine tool orders rose 65.0% mom yoy in March. PPI rose 1.0% yoy in March, versus expectation of 0.5% yoy. Bank lending rose 6.3% yoy in March.

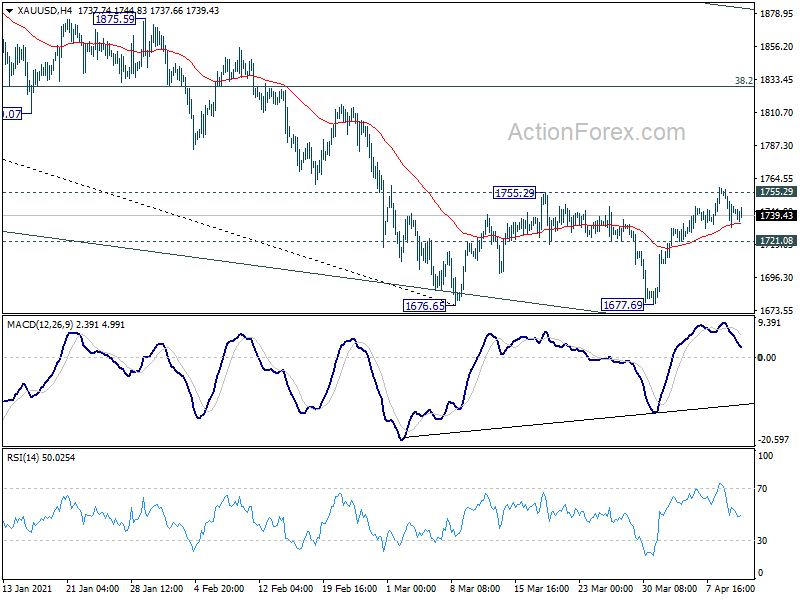

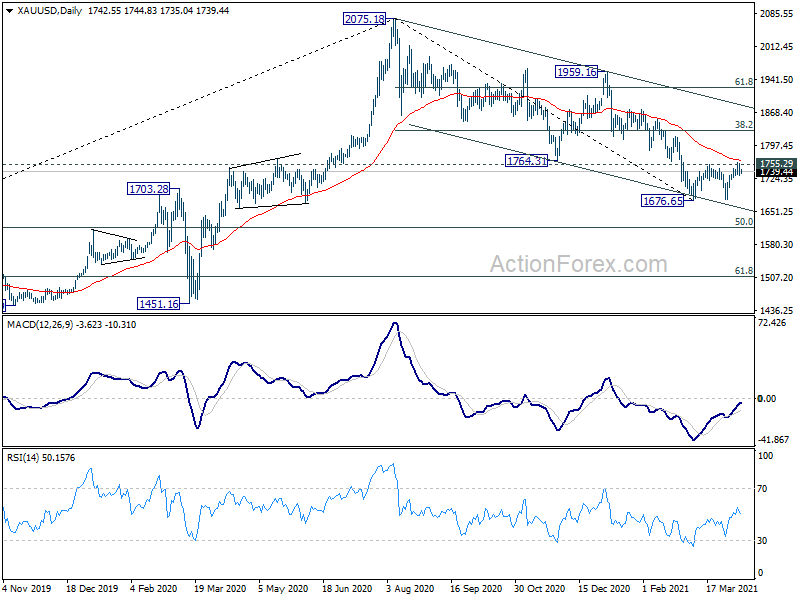

Gold could still retest 1755 resistance after brief retreat

Gold failed to sustain above 1755.29 resistance last week, but subsequent retreat is so far shallow. Further rally remains in favor with 1721.08 minor support holds. At this point, firm break of 1755.29 and 55 day EMA (now at 1763.39) would still consider to have completed a double pattern reversal pattern (1676.65, 1677.69). Stronger rebound should at least be seen to 38.2% retracement of 2075.18 to 1676.65 at 1828.88.

However, break of 1721.08 will indicate that price actions from 1676.65 is just a three wave sideway consolidation pattern. Fall from 2075.18 is then ready to resume for another low.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3665; (P) 1.3708; (R1) 1.3746; More…

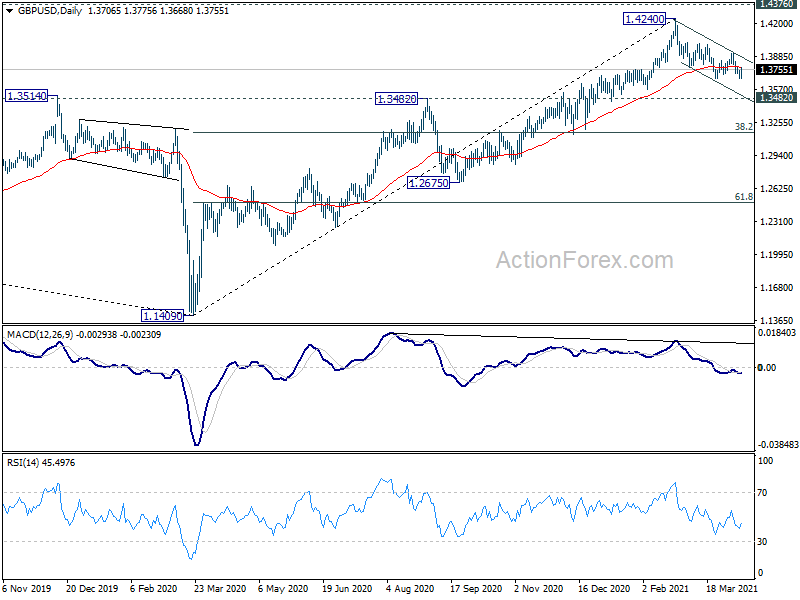

Intraday bias in GBP/USD is turned neutral as it drew support from 1.3669 and recovered. Some consolidations could be seen but risk stays on the downside as long as 1.3917 resistance holds. Break of 1.3668/9 will resume the correction from 1.4240 to 1.3482 key resistance turned support. However, firm break of 1.3917 will suggest that the correction has completed, and bring stronger rise to 1.4000 resistance first.

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed and bring deeper fall to 1.2675 support and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Mar | 6.30% | 6.30% | 6.20% | |

| 23:50 | JPY | PPI Y/Y Mar | 1.00% | 0.50% | -0.70% | -0.60% |

| 6:00 | JPY | Machine Tool Orders Y/Y Mar | 65.00% | 36.70% | ||

| 9:00 | EUR | Eurozone Retail Sales M/M Feb | 3.00% | 1.40% | -5.90% | -5.20% |

| 14:30 | CAD | BoC Business Outlook Survey |