{kind=link}

Dollar rebounds broadly again today as markets are unsettled by renewed strength in treasury yield. At the time of writing, US 10-year yield is back pressing 1.6 handle. DOW future is trading mildly higher, but NASDAQ futures is down -1.3%. Though, Canadian Dollar is even stronger as lifted by much stronger than expected employment data. Sterling, Kiwi and Swiss Franc are the weaker ones today.

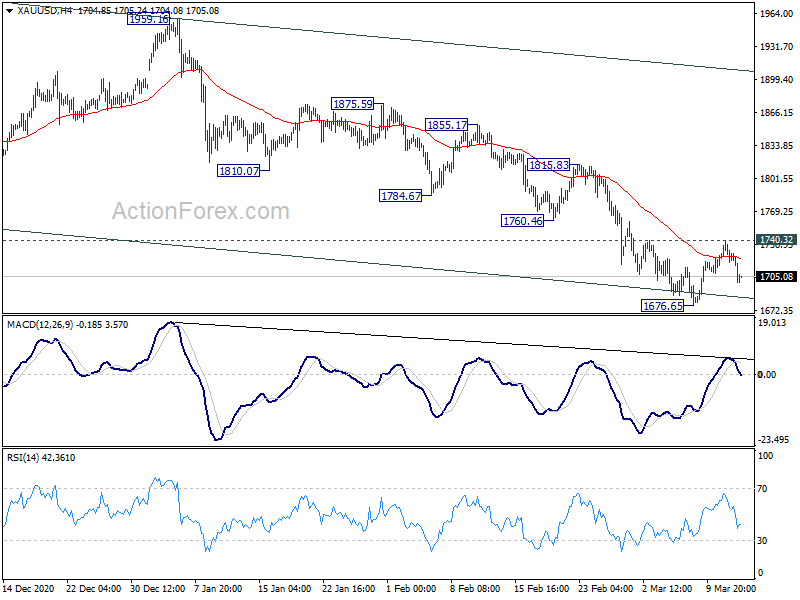

Technically, one focus is on 109.22 temporary top in USD/JPY. Break there will confirm resumption of recent up trend for trend line resistance at around 110.00 handle. Gold’s focus is back to 1676.65 support after rejection by 1740.32 resistance. Break there will affirm underlying strength in Dollar and resume larger correction from 2075.18.

In Europe, currently, FTSE is up 0.02%. DAX is down -0.64%. CAC is down -0.08%. Germany 10-year yield is up 0.035 at -0.298. Earlier in Asia, Nikkei rose 1.73%. Hong Kong HSI dropped -2.20%. China Shanghai SSE rose 0.47%. Singapore Strait Times dropped -0.35%. Japan 10-year JGB yield rose 0.0084 to 0.114.

Canada employment rose 259k in Feb, unemployment rate dropped to 8.2%

Canada employment grew 259k or 1.5% in February, well above expectation of 98k. Part-time jobs increased 171k while full-time jobs rose 88k. Unemployment rate dropped -1.2% to 8.2%, well below expectation of 9.2%. That’s also the lowest level since March 2020. Labor force participation ware was unchanged at 64.7%.

Also from Canada, capacity utilization rose to 79.2% in Q4, above expectation of 77.9%. Wholesale sales rose 4.0% mom in January, below expectation of 5.1% mom.

US PPI jumped to 2.8% yoy, highest since 2018

US PPI rose 0.5% mom in February, above expectation of 0.3% mom. Annually, PPI jumped to 2.8% yoy, up from 1.7% yoy, above expectation of 2.7% yoy. It’s also the largest increase since October 2018.

PPI ex foods, energy and trade services rose 0.2% mom, matched expectations. Annually, PPI ex foods, energy and trade services rose 2.2%, highest since May 2019.

Eurozone industrial production rose 0.8% mom in Jan, EU up 0.7% mom

Eurozone industrial production rose 0.8% mom in January, well above expectation of 0.2% mom. Production of durable consumer goods rose by 0.8% mom, non-durable consumer goods by 0.6% mom, energy and capital goods by 0.4% mom and intermediate goods by 0.3% mom.

EU industrial production rose 0.7% mom. Among Member States for which data are available, the highest increases were registered in Luxembourg (+3.8% mom), Greece and France (both +3.4% mom) and Belgium (+3.1% mom). The largest decreases were observed in Estonia and Latvia (both -1.5% mom), Portugal (-1.3%) and Spain (-0.7% mom).

UK GDP contracted -2.9% mom in Jan, as dragged by services

UK GDP contracted -2.90% mom in January, better than expectation of -4.9% mom. Services was the main drag, due to restrictions, and dropped -3.5% mom. Production sector dropped -1.5% mom, following eight consecutive month of growth. Construction saw 0.9% mom growth.

Overall GDP was -9% below the pre-pandemic level seen in February 2020. Services was down -10.2% from that level, production down -5.0%, manufacturing down -4.7%, construction down -2.6%.

Japan business conditions deteriorated sharply in Q1, no material improvement expected in Q2

According to the Ministry of Finance’s latest survey, business conditions in Japan deteriorated drastically in Q1. The Large manufacturing business survey index (BSI) tumbled from 21.6 to 1.6. Large non-manufacturing BSI turned negative from 6.7 to -7.4. Large all industries BSI also turned negative from 11.6 to -4.5.

Outlook is for Q2 is not expected to improve much, with large manufacturing, large non-manufacturing and large all industries at 2.5. Some improvements could be seen in Q3, with large manufacturing outlook at 9.3, but still way off Q4’s number. Large non-manufacturing Q3 outlook rose to 6.0. Large all industries Q3 outlook rose to 7.1.

New Zealand BNZ manufacturing dropped to 53.4, employment and new orders plunged

New Zealand BusinessNZ Performance of Manufacturing dropped sharply to 53.4 in February, down -4.6 pts from 58.0. Looking at some details, production dropped from 59.3 to 57.3. Employment dropped from 56.1 to 49.8. New orders tumbled from 62.8 to 56.2.

“Despite the PMI remaining in expansion, the proportion of those outlining negative comments stood at 54%, compared with 46% in January. Given the second recent partial lockdown, it remains to be seen what impact this will have on the sector over the next few months,” said BusinessNZ’s executive director for manufacturing Catherine Beard.

BNZ Senior Economist, Craig Ebert said that “supply issues were to the fore from respondents’ comments to February’s PMI survey. Of those citing negative factors, supply rather than demand problems dominated, with frequent references to supply chains, shipping, freight, costs, and difficulties in finding suitable staff.”

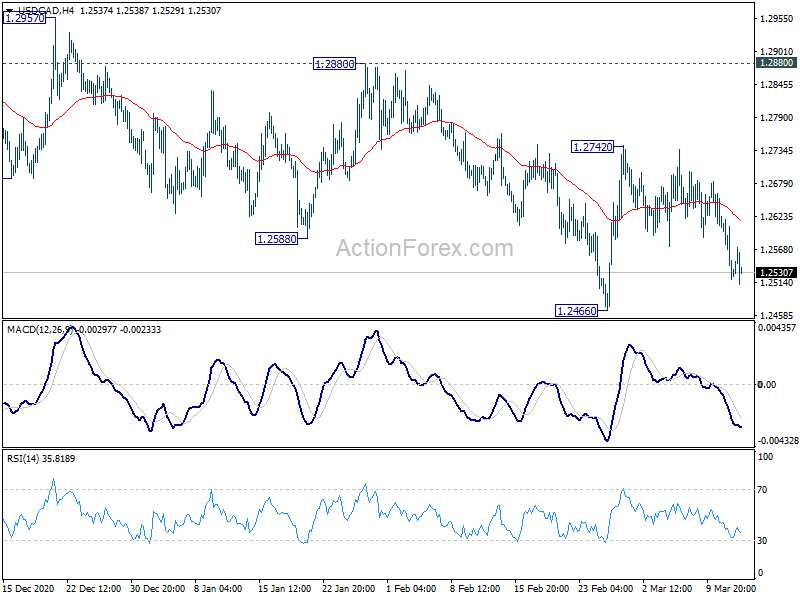

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2497; (P) 1.2561; (R1) 1.2602; More….

Outlook in unchanged in USD/CAD as rebound from 1.2466 should be completed at 1.2742. Intraday bias stays on the downside for retesting 1.2466. Firm break there will resume larger down trend from 1.4667. For now, another rebound cannot be ruled out as corrective pattern from 1.2466 could still extend. But outlook will stay bearish as long as 1.2880 resistance holds.

In the bigger picture, fall from 1.4667 is seen as the third leg of the corrective pattern from 1.4689 (2016 high). Further decline should be seen back to 1.2061 (2017 low). In any case, break of 1.2994 support turned resistance resistance is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Feb | 53.4 | 57.5 | 58 | |

| 23:50 | JPY | BSI Large Manufacturing Index Q1 | 1.6 | 21.6 | ||

| 07:00 | EUR | Germany CPI M/M Feb F | 0.70% | 0.70% | 0.70% | |

| 07:00 | EUR | Germany CPI Y/Y Feb F | 1.30% | 1.30% | 1.30% | |

| 07:00 | GBP | GDP M/M Jan | -2.90% | -4.90% | 1.20% | |

| 07:00 | GBP | Industrial Production M/M Jan | -1.50% | -0.50% | 0.20% | |

| 07:00 | GBP | Industrial Production Y/Y Jan | -4.90% | -4.00% | -3.30% | |

| 07:00 | GBP | Manufacturing Production M/M Jan | -2.30% | -0.60% | 0.30% | |

| 07:00 | GBP | Manufacturing Production Y/Y Jan | -5.20% | -3.60% | -2.50% | |

| 07:00 | GBP | Index of Services 3M/3M Jan | -2.40% | -3.10% | 0.60% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | -9.8B | -13.2B | -14.3B | |

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | 0.80% | 0.20% | -1.60% | -0.10% |

| 13:00 | GBP | NIESR GDP Estimate Feb | -2.00% | -2.50% | ||

| 13:30 | CAD | Capacity Utilization Q4 | 79.20% | 77.90% | 76.50% | 77.40% |

| 13:30 | CAD | Wholesale Sales M/M Jan | 4.00% | 5.10% | -1.30% | -1.10% |

| 13:30 | CAD | Net Change in Employment Feb | 259.2K | 98.5K | -212.8K | |

| 13:30 | CAD | Unemployment Rate Feb | 8.20% | 9.20% | 9.40% | |

| 13:30 | USD | PPI M/M Feb | 0.50% | 0.30% | 1.30% | |

| 13:30 | USD | PPI Y/Y Feb | 2.80% | 2.70% | 1.70% | |

| 13:30 | USD | PPI Core M/M Feb | 0.20% | 0.20% | 1.20% | |

| 13:30 | USD | PPI Core Y/Y Feb | 2.50% | 2.60% | 2.00% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Mar P | 78.5 | 76.8 |