{kind=link}

Sterling and commodity currencies are back in driving seat on positive market sentiments. Nikkei rises sharply in Asian session, following another record close in DOW overnight. Treasury yields also appear to have settled in range after this week’s central bank rhetorics. For now, Yen is the worst performing for the week, followed by Dollar. Aussie is the strongest, followed by the Pound.

Technically, USD/CAD’s break of 1.2574 minor support now puts 1.2466 low in focus. Break will resume larger down trend. Attention will turn to 1.4016 minor resistance in GBP/USD and 0.7837 minor resistance in AUD/USD. Break of these levels will put 1.4240 and 0.8008 resistance in focus respectively. Break there will further solidify the comeback of risk-on theme.

In Asia, currently, Nikkei is up 1.57%. Hong Kong HSI is down -0.65%. China Shanghai SSE is up 0.14%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is up 0.0134 at 0.119. Overnight, DOW rose 0.58%. S&P 500 rose 1.04%. NASDAQ rose 2.52%. 10-year yield rose 0.007 to 1.527.

Japan business conditions deteriorated sharply in Q1, no material improvement expected in Q2

According to the Ministry of Finance’s latest survey, business conditions in Japan deteriorated drastically in Q1. The Large manufacturing business survey index (BSI) tumbled from 21.6 to 1.6. Large non-manufacturing BSI turned negative from 6.7 to -7.4. Large all industries BSI also turned negative from 11.6 to -4.5.

Outlook is for Q2 is not expected to improve much, with large manufacturing, large non-manufacturing and large all industries at 2.5. Some improvements could be seen in Q3, with large manufacturing outlook at 9.3, but still way off Q4’s number. Large non-manufacturing Q3 outlook rose to 6.0. Large all industries Q3 outlook rose to 7.1.

New Zealand BNZ manufacturing dropped to 53.4, employment and new orders plunged

New Zealand BusinessNZ Performance of Manufacturing dropped sharply to 53.4 in February, down -4.6 pts from 58.0. Looking at some details, production dropped from 59.3 to 57.3. Employment dropped from 56.1 to 49.8. New orders tumbled from 62.8 to 56.2.

“Despite the PMI remaining in expansion, the proportion of those outlining negative comments stood at 54%, compared with 46% in January. Given the second recent partial lockdown, it remains to be seen what impact this will have on the sector over the next few months,” said BusinessNZ’s executive director for manufacturing Catherine Beard.

BNZ Senior Economist, Craig Ebert said that “supply issues were to the fore from respondents’ comments to February’s PMI survey. Of those citing negative factors, supply rather than demand problems dominated, with frequent references to supply chains, shipping, freight, costs, and difficulties in finding suitable staff.”

Looking ahead

Germany UK GDP and production will be the major focus in European session, while trade balance will also be featured. Germany CPI final and Eurozone industrial will be released too.

Later in the day, Canada employment will take center stage with wholesale sales and capacity utilization. US will release PPI and U of Michigan consumer sentiment.

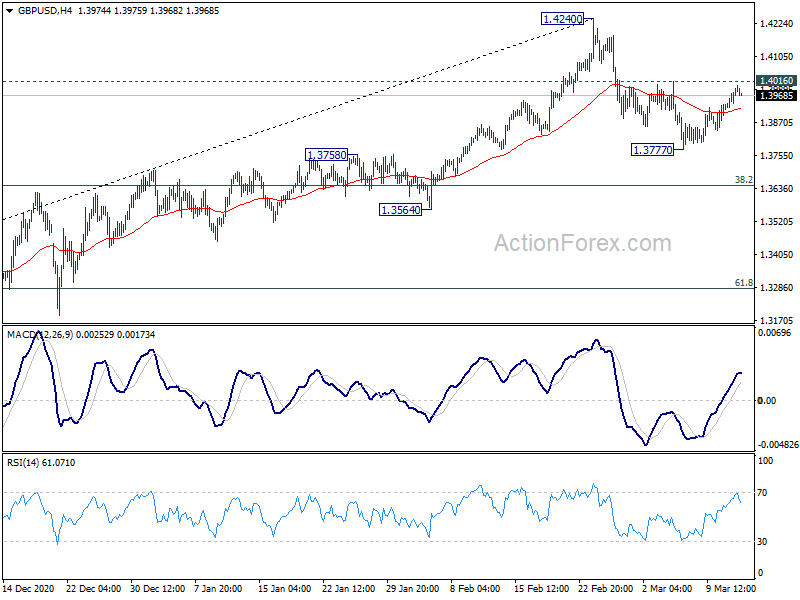

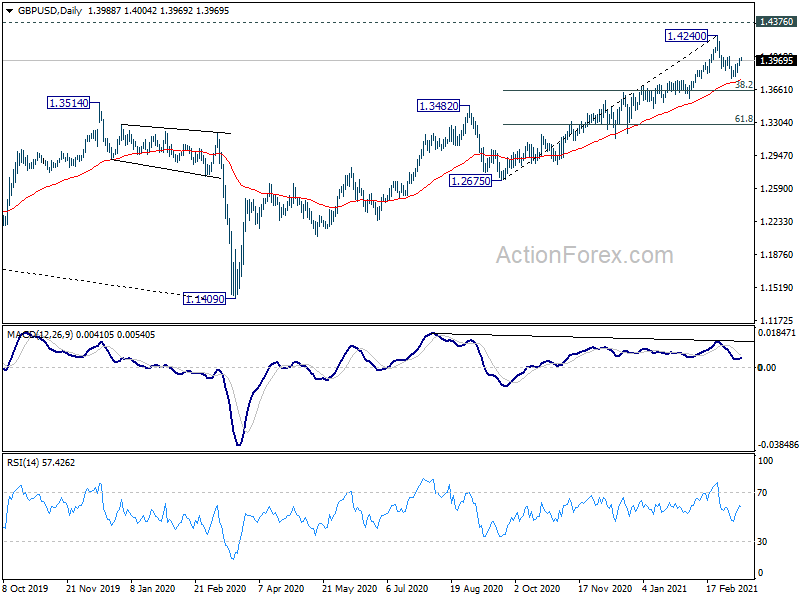

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3944; (P) 1.3969; (R1) 1.4020 More….

GBP/USD’s rebound from 1.3777 extends higher today and focus is now on 1.4016 minor resistance Break there will argue that the correction from 1.4240 has completed. Further rise should be seen to retest 1.4240 first. On the other hand, rejection by 1.4016 could extend the correction with another leg through 1.3777. But in that case, downside should be contained by 38.2% retracement of 1.2675 to 1.4240 at 1.3642 to bring rebound.

In the bigger picture, rise from 1.1409 medium term bottom is in progress. Further rally would be seen to 1.4376 resistance and above. Decisive break there will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. On the downside, break of 1.3482 resistance turned support is needed to be first indication of completion of the rise. Otherwise, outlook will stay cautiously bullish even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Feb | 53.4 | 57.5 | 58 | |

| 23:50 | JPY | BSI Large Manufacturing Index Q1 | 1.6 | 21.6 | ||

| 07:00 | EUR | Germany CPI M/M Feb F | 0.70% | 0.70% | ||

| 07:00 | EUR | Germany CPI Y/Y Feb F | 1.30% | 1.30% | ||

| 07:00 | GBP | GDP M/M Jan | -4.90% | 1.20% | ||

| 07:00 | GBP | Industrial Production M/M Jan | -0.50% | 0.20% | ||

| 07:00 | GBP | Industrial Production Y/Y Jan | -4.00% | -3.30% | ||

| 07:00 | GBP | Manufacturing Production M/M Jan | -0.60% | 0.30% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Jan | -3.60% | -2.50% | ||

| 07:00 | GBP | Index of Services 3M/3M Jan | -3.10% | 0.60% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | -13.2B | -14.3B | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | 0.20% | -1.60% | ||

| 13:00 | GBP | NIESR GDP Estimate Feb | -2.50% | |||

| 13:30 | CAD | Capacity Utilization Q4 | 77.90% | 76.50% | ||

| 13:30 | CAD | Wholesale Sales M/M Jan | 5.10% | -1.30% | ||

| 13:30 | CAD | Net Change in Employment Feb | 98.5K | -212.8K | ||

| 13:30 | CAD | Unemployment Rate Feb | 9.20% | 9.40% | ||

| 13:30 | USD | PPI M/M Feb | 0.30% | 1.30% | ||

| 13:30 | USD | PPI Y/Y Feb | 2.70% | 1.70% | ||

| 13:30 | USD | PPI Core M/M Feb | 0.20% | 1.20% | ||

| 13:30 | USD | PPI Core Y/Y Feb | 2.60% | 2.00% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Mar P | 78.5 | 76.8 |