{kind=link}

Euro softens mildly after ECB announced to speed up PEPP purchases in the next quarter. But loss is relatively limited as the overall envelop was kept unchanged. Dollar and Yen are currently the worst performing one for today, on the back of risk-on sentiments. Commodity currencies are currently the stronger ones, as led by Aussie. Focus will now be back on US 30-year auctions, and development in yields and stocks.

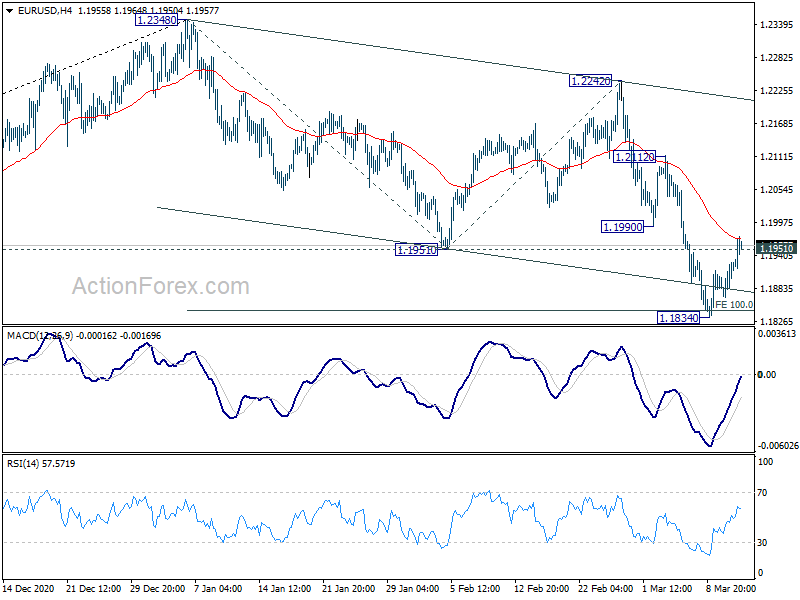

Technically, EUR/USD’s break of 1.1951 resistance suggests short term bottoming at 1.1834. Stronger rebound is now in favor. As for Euro, a focus will be on 129.96 resistance in EUR/JPY. Break there will resume EUR/JPY’s recent up trade and could help solidify EUR/USD’s rebound. As for Dollar, break of 1740.32 resistance in Gold will indicate short term bottoming, and add some pressure to the greenback.

In Europe, currently, FTSE is up 0.03%. DAX is up 0.09%. CAC is up 0.24%. Germany 10-year yield is down -0.0301 at -0.343. Earlier in Asia, Nikkei rose 0.60%. Hong Kong HSI rose 1.65%. China Shanghai SSE rose 2.36%. Singapore Strait Times rose 0.85%. Japan 10-year JGB yield dropped -0.0205 to 0.105.

ECB: PEPP to be conducted at significantly higher pace over the next quarter

ECB said it expected the purchases under the pandemic emergency purchase programme (PEPP) to be conducted at a “significantly higher pace” over the next quarter. Though, the total envelop will be left unchanged at EUR 1850B, and the program will continue until at least end of March 2022.

The Governing Council will purchase flexibly according to market conditions and with a view to “preventing a tightening of financing conditions”. The total envelop can be “recalibrated if required”, to maintain favourable financing conditions to help counter the negative pandemic shock to the path of inflation.

Main refinancing rate is kept at 0.00%. Marginal lending rate and deposit rate are held at 0.25% and -0.50% respectively. Interest are expected to “remain at their present or lower levels” until inflation outlook robustly converges to target within its horizon.

ECB Lagarde: Increase in market rates poses a risk to wider financing conditions

In the post meeting press conference, ECB President Christine Lagarde acknowledged that “market interest rates have increased since the start of the year, which poses a risk to wider financing conditions.”

“Banks use risk-free interest rates and sovereign bond yields as key references for determining credit conditions,” she explained. “If sizeable and persistent, increases in these market interest rates, when left unchecked, could translate into a premature tightening of financing conditions for all sectors of the economy”.

“This is undesirable at a time when preserving favourable financing conditions still remains necessary to reduce uncertainty and bolster confidence, thereby underpinning economic activity and safeguarding medium-term price stability.”

In the baseline scenario of the new economic projections, Eurozone GDP growth is expected to be at 4.0% in 2021, 4.1% in 2022, and 2.1% in 2023. Outlook is “broadly unchanged” comparing to December projections. Risks over medium term “have become more balanced” even though downside risks remains in the near term.

Annual inflation is projected to be at 1.5% in 2021, 1.2% in 2022, and 1.4% in 2023. The outlook for 2021 and 2022 was revised up, “largely due to temporary factors and higher energy price inflation.

Swiss government expects 3.0% GDP growth this year, 3.3% next

Swiss Federal Government’s Expert Group said the country’s GDP is set to decrease in Q1. But following the easing of coronavirus measures, the economy should have a “rapid recovery” subsequently. Nevertheless, “uncertainty remains extremely high”.

The Expert Group kept 2021 GDP growth expectation unchanged at 3.0%, adjusted for sporting events. That would be “above-average rate by historical standards”. Pre-crisis GDP level would be exceeded “by late 2021”. Unemployment rate is expected to fall gradually and reach an annual average of 3.3% for 2021, also unchanged.

For 2022, the Expect Group predicts 3.3% GDP growth (revised up from 3.1%), with unemployment rate averaging 3.0%.

US initial jobless claims dropped to 712k, continuing claims down to 4.14m

US initial jobless claims dropped -42k to 712k in the week ending March 6, better than expectation of 725k. Four-week moving average of initial claims dropped -34k to 759k.

Continuing claims dropped -193k to 4144k in the week ending February 27. Four-week moving average of continuing claims dropped 103.5k to 4355.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1889; (P) 1.1909; (R1) 1.1950; More….

Break of 1.1951 support turned resistance suggests short term bottoming at 1.1834. Intraday bias is back on the upside for 55 day EMA (now at 1.2060). Sustained break there will indicate completion of correction from 1.2348 and bring retest of this high. On the downside, however, break of 1.1834 will extend the correction from 1.2348 to 38.2% retracement of 1.0635 to 1.2348 at 1.1694.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. We’d be alerted to topping sign around 1.2516/55. But sustained break there will carry long term bullish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Feb | -0.70% | -0.70% | -1.60% | -1.50% |

| 00:00 | AUD | Consumer Inflation Expectations Mar | 4.10% | 3.70% | ||

| 00:01 | GBP | RICS Housing Price Balance Feb | 52% | 46% | 50% | 49% |

| 12:45 | EUR | ECB Interest Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | USD | Initial Jobless Claims (Mar 5) | 712K | 725K | 745K | 754K |

| 15:30 | USD | Natural Gas Storage | -76B | -98B |