{kind=link}

Dollar rises further in early US session after much stronger than expected non-farm payroll report. 10-year yield also surges and it’s now back above 1.6 handle. The greenback in currently the second strongest for the week, only overwhelmed by the oil supported Canadian Dollar. While Swiss Franc and Yen are trying to recover against others, in particular commodity currencies, both are still the worst performing for the week.

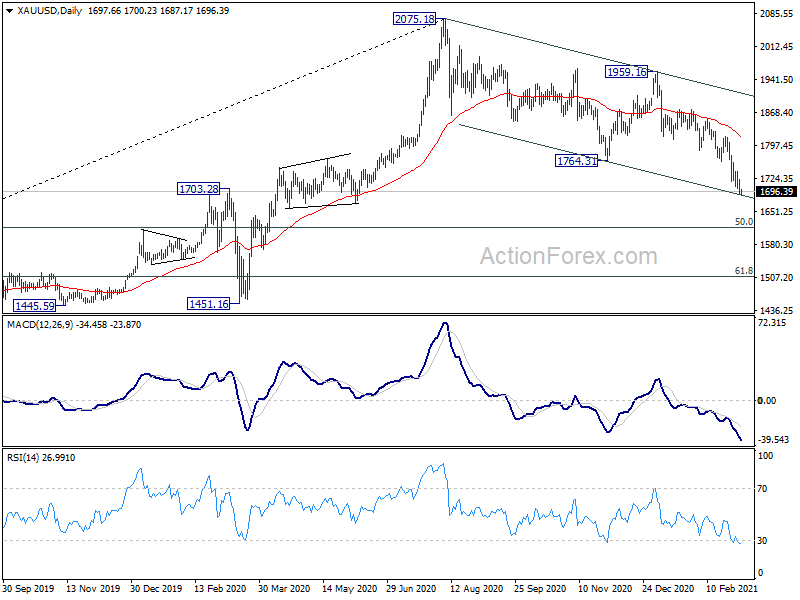

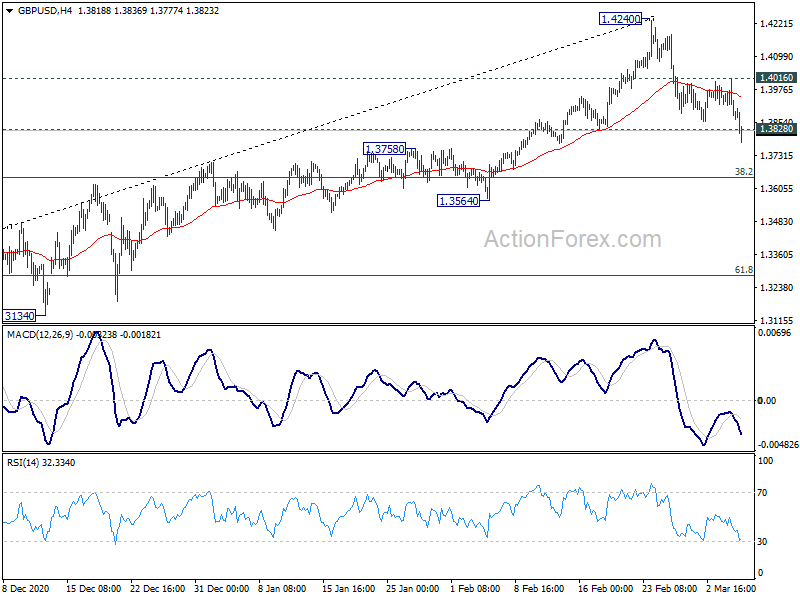

Technically, Dollar’s strength is now being more convincing with break of 1.3828 support in GBP/USD and 0.7591 temporary low in AUD/USD. A focus is on whether gold would break through medium term channel support, to accompany further rally in Dollar. Or, gold would stabilize from here and recover first. We’d probably only find out early next week.

In Europe, currently, FTSE is down -0.06%. DAX is down -0.70%. CAC is down -0.58%. Germany 10-year yield is up 0.020 at -0.288. Earlier in Asia, Nikkei dropped -0.23%. Hong Kong HSI dropped -0.47%. China Shanghai SSE dropped -0.04%. Singapore Strait Times dropped -0.03%. Japan 10-year JGB yield dropped -0.0434 to 0.097, back below 0.1 handle.

US non-farm payrolls grew 379k in Feb, unemployment rate dropped to 6.2%

US non-farm payrolls employment grew 379k in February, well above expectation of 148k. Prior month’s figure was also revised sharply up from 49k to 166k. Overall, total non-farm payroll employment was still down by -9.5m or -6.2% from pre pandemic level in February 2020.

Unemployment rate dropped to 6.2%, down from 6.3%, better than expectation of 6.4%. average hourly earnings rose 0.2% mom, matched expectations. Labor force participation rate remained at 61.4%.

US trade deficit widened to USD -68.2B in January versus expectation of USD -67.5B. Canada trade surplus came in at CAD 1.4B, versus expectation of CAD -1.4B.

Released in European session, Italy retail sales dropped -3.0% mom in January, below expectation of -0.6% mom. France trade deficit widened to EUR -3.9B in January. versus expectation of -3.4B. Germany factory orders rose 1.4% mom in January, versus expectation of -1.0% mom. Swiss foreign currency reserves rose to CHF 914B in February.

BoJ Kuroda: Important to keep yield curve stably low

BoJ Governor Haruhiko Kuroda told the parliament today that “it’s important to keep the yield curve stably low for the time being.” The central bank allows 10-year JGB yield to move inside a band around 0% to “enhance bond market functions”. But given recent surge in yields, “much more debate” was needed before deciding to widen the band.

“It’s a difficult decision,” Kuroda said, “the economy remains under pressure from the COVID-19 pandemic.”

“We have been and must continue to buy ETFs flexibly,” he said. “We’ll discuss at the March review how specifically we could make our purchases more nimble”.

Australia AiG services rose to 55.8, but employment fell

Australia AiG Performance of Services rose 1.5 pts to 55.8 in February, highest since June 2018, as “recovery following the COVID-19 recession of 2020 gaining in strength”. Looking at some details, sales rose 5.5 pts to 65.7. New orders rose 3.6 pts to 58.4. However, employment dropped -13.2 to 42.7. Input prices rose slightly by 1.8 to 64.4. But selling prices jumped 11.2 to 56.2.

Ai Group Chief Executive, Innes Willox, said: ” While the continued improvement in conditions is heartening, employment fell in February following a strong recovery in the preceding months. Employers and employees will be hoping that the further growth in new orders recorded in February signals the continued recovery of sales and employment over the next few months.”

Gold breaks 1700, pressing channel support

Gold’s correction extends lower today and breaks 1700 handle. It’s now pressing medium term channel support and there is prospect of a quick rebound. Yet, break of 1740.32 resistance is needed to indicate short term bottoming first. Otherwise, further decline is still in favor.

Meanwhile, sustained trading below the channel support will indicates downside acceleration. Gold should then dive further to 50% retracement of 1160.17 to 2075.18 at 1617.67 or even 61.8% retracement at 1509.70, before forming a bottom.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3844; (P) 1.3930; (R1) 1.3981 More….

GBP/USD’s break of 1.3828 support now suggests that deeper correction is underway. Intraday bias is back on the downside for 38.2% retracement of 1.2675 to 1.4240 at 1.3642 first. Break there will target 61.8% retracement at 1.3273 next. On the upside, break of 1.4016 resistance is needed to indicate completion of the pull back. Otherwise, risk will stay mildly on the downside.

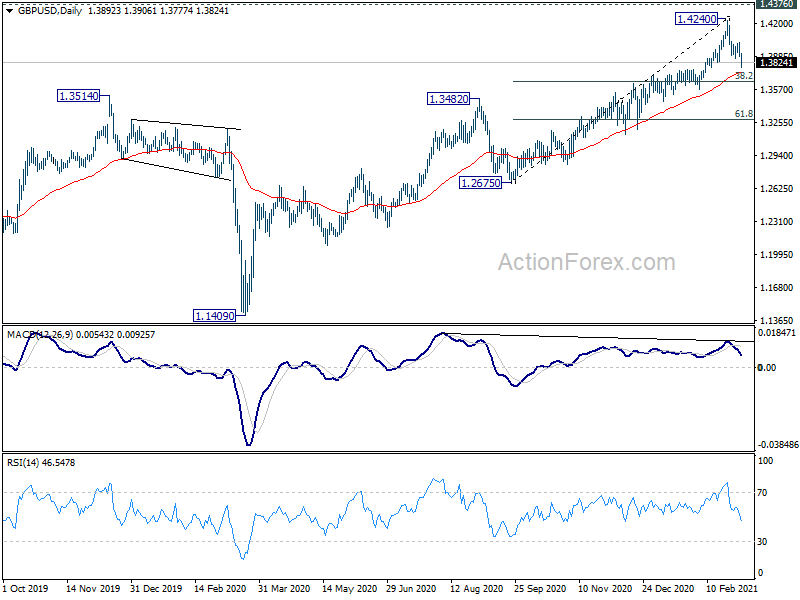

In the bigger picture, rise from 1.1409 medium term bottom is in progress. Further rally would be seen to 1.4376 resistance and above. Decisive break there will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. On the downside, break of 1.3482 resistance turned support is needed to be first indication of completion of the rise. Otherwise, outlook will stay cautiously bullish even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Feb | 55.8 | 54.3 | ||

| 07:00 | EUR | Germany Factory Orders M/M Jan | 1.40% | -1.00% | -1.90% | -2.20% |

| 07:45 | EUR | France Trade Balance (EUR) Jan | -3.9B | -3.4B | -3.4B | -3.6B |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Feb | 914B | 896B | ||

| 09:00 | EUR | Italy Retail Sales M/M Jan | -3.00% | -0.60% | 2.50% | 2.40% |

| 13:30 | USD | Nonfarm Payrolls Feb | 379K | 148K | 49K | 166 K |

| 13:30 | USD | Unemployment Rate Feb | 6.20% | 6.40% | 6.30% | |

| 13:30 | USD | Average Hourly Earnings M/M Feb | 0.20% | 0.20% | 0.20% | 0.10% |

| 13:30 | USD | Trade Balance (USD) Jan | -68.2B | -67.5B | -66.6B | -67 B |

| 13:30 | CAD | Trade Balance (CAD) Jan | 1.4B | -1.4B | -1.7B | -1.98 B |

| 15:00 | CAD | Ivey PMI Feb | 49.2 | 48.4 |