{kind=link}

Dollar is striking back today with some help from surging US yields. At the time of writing, 10-year yield is trading above 1.25 handle. Additionally, much stronger than expected manufacturing is support the greenback too. While European stocks are treading water, US futures point to higher open. Yen is now the worst performing one, followed by Aussie and Canadian. Overall, it remains to be seen if Dollar could sustain the rebound.

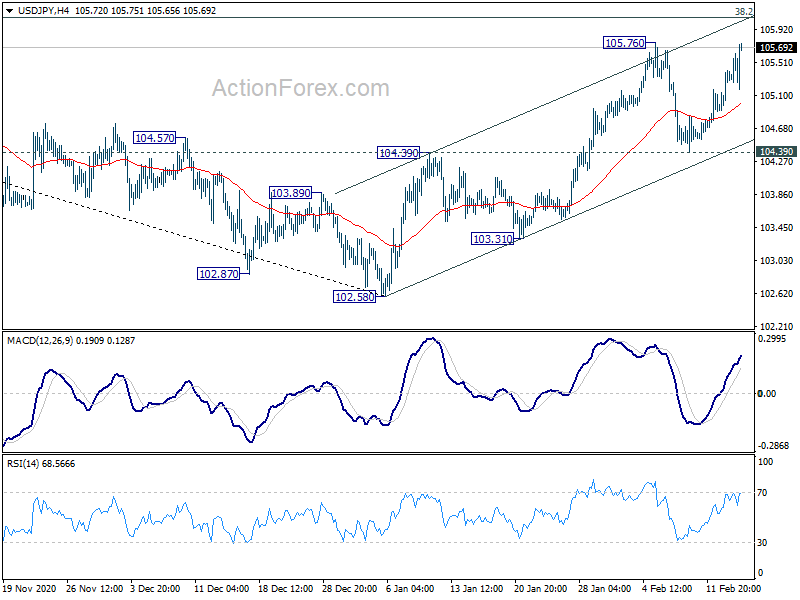

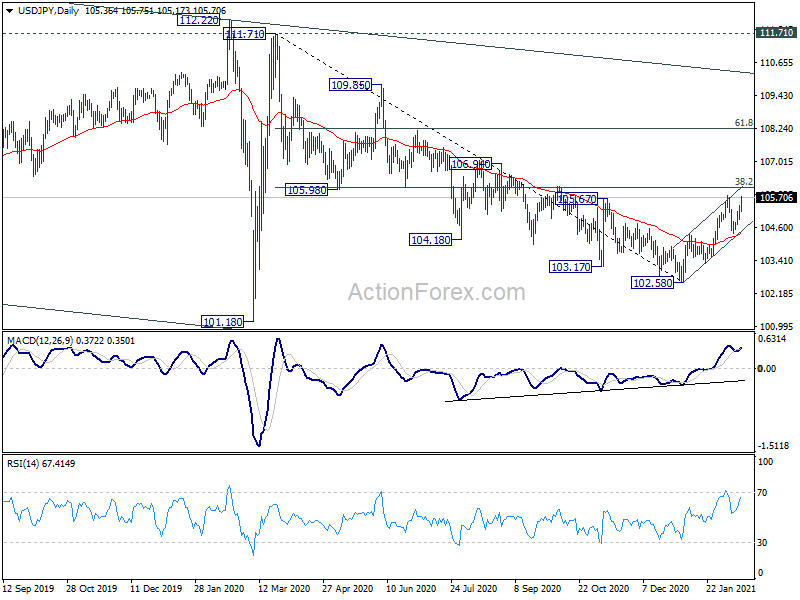

Technically, Gold’s decline is consistent with a Dollar rebound. Break of 1784.67 support would resume the fall from 1959.16, and affirm Dollar’s strength. 105.76 resistance in USD/JPY is the first hurdle for the greenback and break could at least give a floor. Other levels to watch include 1.2080 minor support in EUR/USD, 1.3865 minor support in GBP/USD and 0.7717 minor support in AUD/USD. Break of these levels would also solidify the case for a near term rebound in Dollar.

In other markets, currently, DOW future is up 0.44%. US 10-year yield is up 0.047 at 1.257. FTSE is up 0.06%. DAC is down -0.01%. CAC is down -0.03%. Germany 10-yaer yield is up 0.0141 at 0.367. Earlier in Asia, Nikkei rose 1.28%. Hong Kong HSI rose 1.90%. Singapore Strait Times rose 0.13%. Japan 10-year yield rose 0.0002 to 0.080.

US Empire State manufacturing rose to 12.1 in Feb, highest since Jul 2020

US Empire State Manufacturing business conditions rose to 12.1 in February, up from 3.5, well above expectation of 5.5. That’s also the highest level since July 2020. 32% of respondents reported that conditions had improved, while 20% said conditions had worsened.

New orders rose 4.2 pts to 10.8. Shipments dropped -3.3 to 4.0. Prices paid jumped 12.3 pts to 57.8. Prices received also rose 8.2 to 15.2. Number of employees edged up by 0.9 to 12.1 Average employee workweek also rose slightly by 2.7 to 9.0.

German ZEW rose to 71.2, optimistic about the future

German ZEW Economic Sentiment rose to 71.2 in February, up from 61.8, well above expectation of 60.0. Current Situation Index dropped to -67.2, down from -66.4, missed expectation of -67.0. Eurozone ZEW Economist Sentiment rose to 69.9, up from 58.3, well above expectation of 59.2. Current Situation Index rose 4.3 pts to 74.6.

The financial market experts are optimistic about the future. They are confident that the German economy will be back on the growth track within the next six months. Consumption and retail trade in particular are expected to recover significantly, accompanied by higher inflation expectations,” comments ZEW President Achim Wambach.

Eurozone GDP contracted -0.6% qoq in Q4, EU down -0.4% qoq

Eurozone GDP contracted -0.6% qoq in Q4, following the strong rebound of 12.4% qoq in Q3. EU GDP contracted -0.4% in Q4, following 11.5% qoq growth in Q3. For 2020, annual contraction in Eurozone GDP was at -6.8%, and -6.4% for EU. Eurozone employment rose 0.3% qoq while EU employment also rose 0.3% qoq.

RBA Minutes: Some years before inflation and unemployment goals achieved

Minutes of RBA’s February 2 meeting noted that a number of major central banks had already announced extensions of their QE program. There was also a widespread expectation for RBA to extend its own. Hence, “if the Bank were to cease bond purchases in April, it was likely that there would be unwelcome significant upward pressure on the exchange rate.”

Outlook for the economy also indicated that it would be “some years before the goal of inflation and unemployment were achieved”. Hence, RBA decided to purchase an additional AUD 100B of Australian Government and states and territories after the current program completes in April.

On interest rate, the minutes reiterated that a negative policy rate is “extraordinarily unlikely”. Cash rate would be maintained at 10 basis points for “as long as necessary”. The conditions for a rate hike are not expected to be met “until 2024 at the earliest”.

BoJ Kuroda: Optimism over global outlook and vaccine rollouts behind surge in stock prices

BoJ Governor Haruhiko Kuroda told the parliament that “optimism over the global economic outlook and steady vaccine rollouts may be behind the recent surge in stock prices”. Nevertheless, he also warned that “global outlook remains highly uncertain and risks to Japan’s economy remained tilted to the downside. His comment came when Nikkei closed above 30k level for the first time in three decades.

Kuroda also noted that it’s premature to consider exiting the massive monetary stimulus measures, including ETF purchase. “It’s likely to take significant time to achieve our price target. As such, now is not the time to think about an exit including from our ETF buying,” he said.

Finance Minister Taro Aso also said, it’s not time to withdraw fiscal support. “The biggest issue now is when to shift from crisis-mode policy to fiscal restoration. In doing so, it’s important for such action to be coordinated,” he added.

Also from Japan, tertiary industry index dropped -0.4% mom in December, versus expectation of -0.6% mom.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.05; (P) 105.24; (R1) 105.55; More..

Focus is now on 105.76 resistance in USD/JPY. Decisive break there will confirm resumption of rise from 102.58 and turn bias to the upside. Such rebound is at least correcting the down trend from 111.71 to 102.58. Next target is 38.2% retracement of 111.71 to 102.58 at 106.06. Break will target 61.8% retracement at 108.22. However, firm break of 104.39 will indicate that rebound from 102.58 has completed at 105.76. Intraday bias will be turned to the downside for 103.31 support first.

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016), and there is no clear indication of trend reversal yet. Though, sustained trading above 55 week EMA (now at 105.90) will be the first sign of reversal and turn focus to channel resistance (now at 110.23).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | RBA Minutes | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Dec | -0.40% | -0.60% | -0.70% | -0.60% |

| 09:00 | EUR | Italy Trade Balance (EUR) Jan | 6.84B | 6.77B | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Feb | 71.2 | 60 | 61.8 | |

| 10:00 | EUR | Germany ZEW Current Situation Feb | -67.2 | -67 | -66.4 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Feb | 69.9 | 59.2 | 58.3 | |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | -0.60% | -0.70% | -0.70% | |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 P | 0.30% | 1.00% | ||

| 13:30 | CAD | Foreign Portfolio Investment (CAD) Dec | 5.08B | 7.72B | 11.78B | |

| 13:30 | USD | Empire State Manufacturing Index Feb | 12.1 | 5.5 | 3.5 |