{kind=link}

Sterling strength continues today, in the otherwise mixed markets. UK Prime Minister Boris Johnson told the parliament that restrictions measures are already “starting to have an effect in many parts of the country”. Canadian Dollar is following as second strongest for today, lifted slightly by upside acceleration in oil prices. Dollar, as the third strongest, is paring back some of yesterday’s losses. On the other hand, selling focus is turning back to the Euro, with Aussie and Kiwi also turning soft slightly.

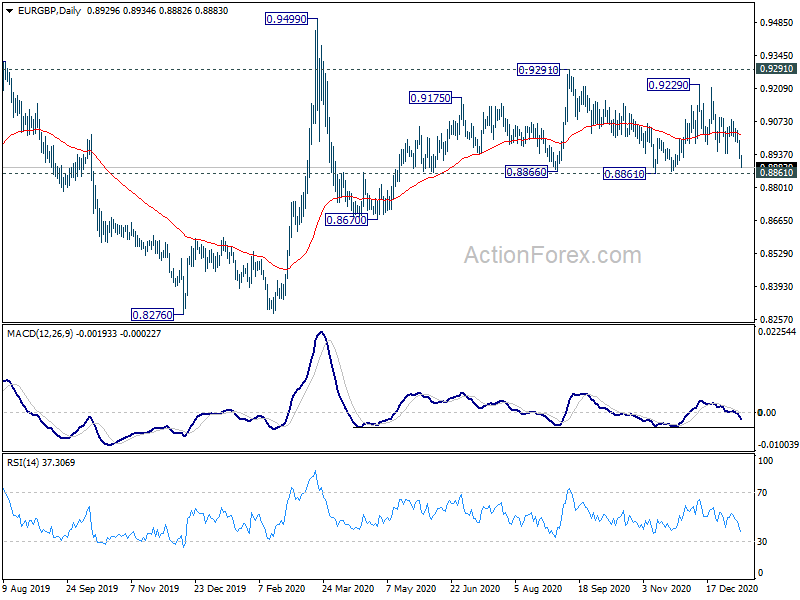

Technically, Sterling pairs would be a focus for the rest of the week. GBP/CHF’s break of 1.2118 resistance is a sign that near term buying is back. GBP/USD is pressing 1.3702 resistance, without backing off. Firm break there will resume larger rise from 1.1409 to 1.3956 projection level. More importantly, EUR/GBP could have a take on 0.8861 key near term support. Decisive break there would resume the pattern from 0.9499, with another falling leg through 0.8670 support.

In Europe, currently, FTSE is down -0.10%. DAX is down -0.03%. CAC is up 0.17%. Germany 10-year yield is down -0.039 at -0.503. Earlier in Asia, Nikkei rose 1.04%. Hong Kong HSI dropped -0.15%. China Shanghai SSE dropped -0.27%. Singapore Strait Times rose 0.01%. 10-year JGB yield dropped -0.0052 to 0.032.

US CPI ticked up to 1.4% yoy in Dec, core CPI unchanged at 1.6% yoy

US CPI rose 0.4% mom in December while core CPI rose 0.1% mom. Both matched expectations. On annual basis, CPI accelerated to 1.4% yoy, up from 1.2% yoy, above expectation of 1.3% yoy. Core CPI was unchanged at 1.6% yoy, matched expectations.

Eurozone industrial production rose 2.5% mom in Nov, EU up 2.3% mom

Eurozone industrial production rose 2.5% mom in November, well above expectation of 0.3% mom. Production of capital goods rose by 7.0% mom and intermediate goods by 1.5% mom, while production of durable consumer goods fell by -1.2% mom, non-durable consumer goods by -1.7% mom and energy by -3.9% mom.

EU industrial production rose 2.3% mom. Among Member States, for which data are available, the highest increases were registered in Ireland (+52.8% mom), Greece (+6.3% mom) and Denmark (+5.3% mom). The largest decreases were observed in Portugal (-5.1% mom), Belgium (-3.5% mom) and Croatia (-2.6% mom).

Also released, Italy industrial output dropped -1.4% mom in November, versus expectation of 0.0% mom. Germany WPI rose 0.6% mom in December, versus expectation of 0.1% mom.

ECB Lagarde: Some restrictions in Q1 considered in last economic projections

ECB President Christine Lagarde said the forecasts of 3.9% GDP growth this year in Eurozone is “still very plausible”, despite resurgent in coronavirus infections. She explained that’s because “our forecast is predicated on lockdown measures until the end of the first quarter.

“What would be a concern would be that after the end of March those member states still need to have lockdown measures and if, for instance, vaccination programmes were slowed down,” she added.

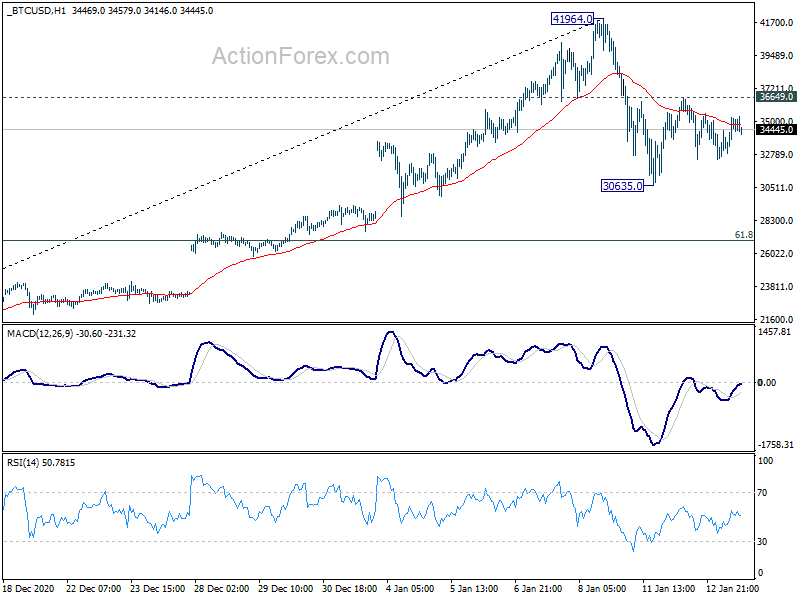

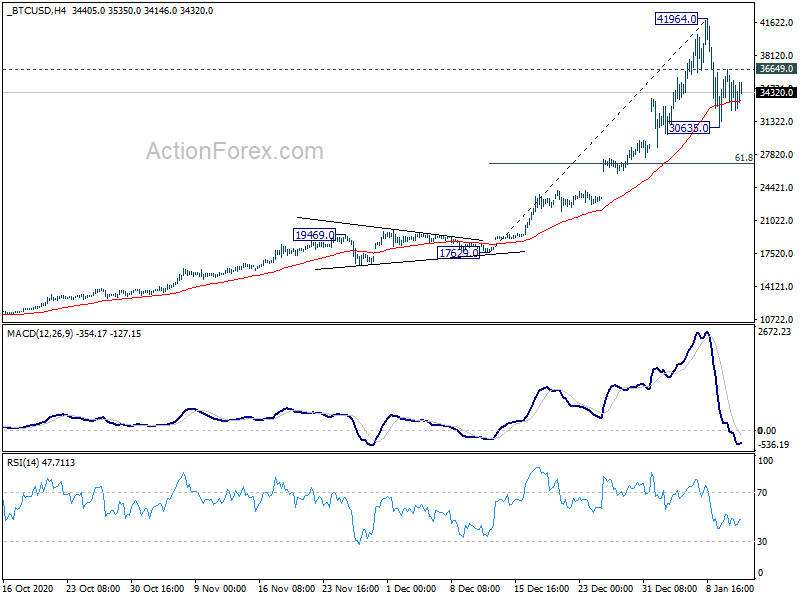

Bitcoin settles in range above 30k, await next move

Lagarde also said in the Reuters Next conference that Bitcoin is a “highly speculative asset, which has conducted some funny business and some interesting and totally reprehensible money laundering activity”. As for crytocurrencies in general, she said, “there has to be regulation. This has to be applied and agreed upon … at a global level because if there is an escape that escape will be used.”

Bitcoin’s pull back from 41964.0 was a bit deeper than expected. But is quickly recovered back above 4 hour 55 EMA and settles in range. Though, as recovery attempt was so far held by 55 H EMA, another fall would be mildly in favor, but 30k handle should provide enough support for now. Meanwhile, a break above 36649.0 resistance will suggest that the correction has completed, and bring retest on the high.

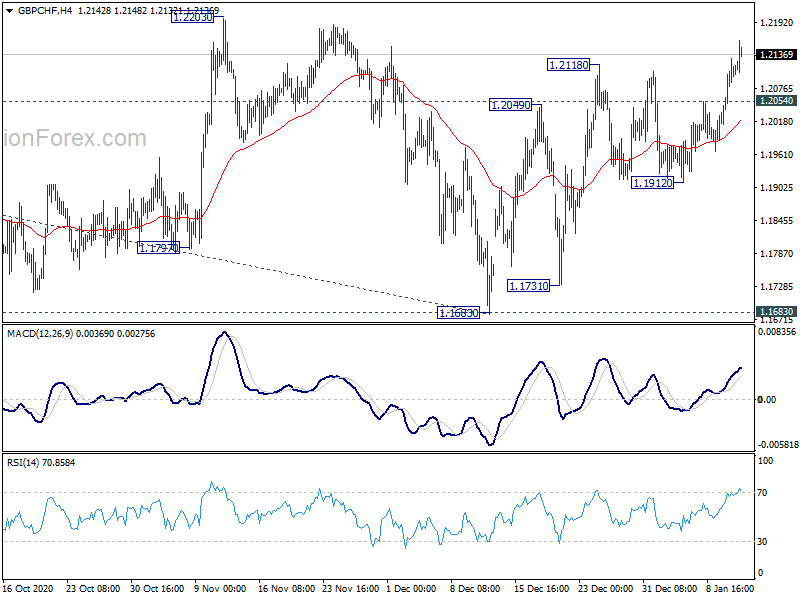

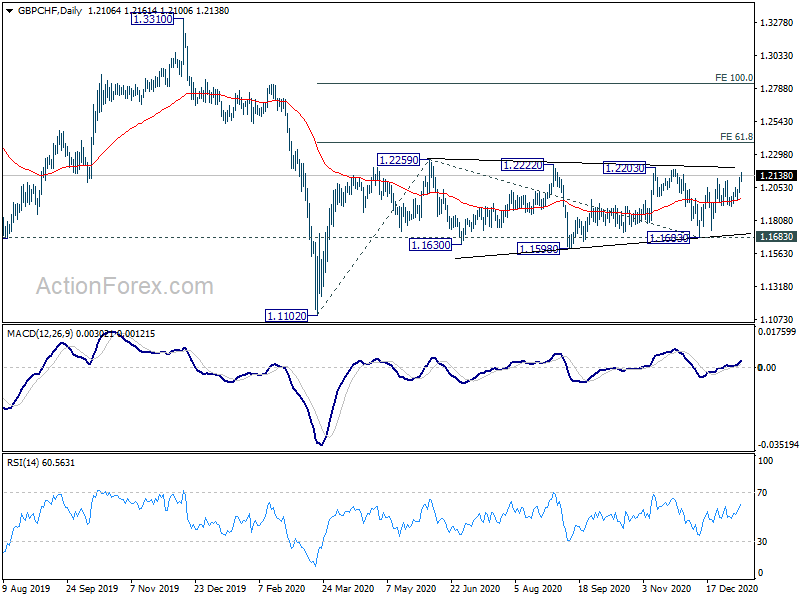

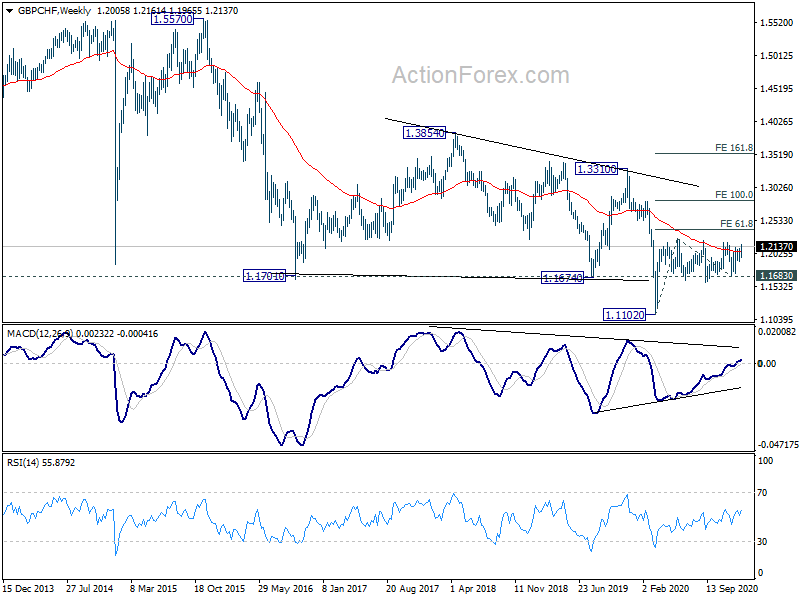

GBP/CHF breaks through 1.2118, ready to resume rise from 1.1102

GBP/CHF rides on broad based rally in Sterling this week and breaks through 1.2118 resistance. The development suggests resumption of the rise from 1.1683. Further rally is expected as long as 1.2054 support holds, for 1.2203/59 resistance zone. Decisive break there will resume whole rebound from 1.1102 to 61.8, projection of 1.1102 to 1.2259 from 1.1683 at 1.2398.

If happens, that would be a bullish medium term development too, as GBP/CHF could then sustain above 55 week EMA.

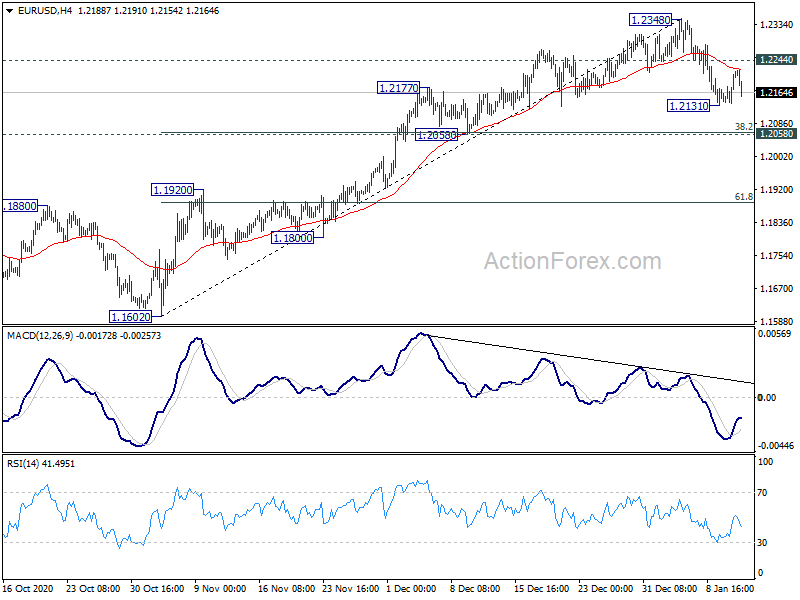

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2160; (P) 1.2185; (R1) 1.2233; More…

Intraday bias in EUR/USD remains neutral first. With 1.2244 minor resistance intact, another fall could still be seen as consolidation from 1.2348 extends. But downside should be contained by 1.2058 cluster support (38.2% retracement of 1.1602 to 1.2348 at 1.2063) to bring rebound. Meanwhile, on the upside, break of 1.2244 minor resistance will bring retest of 1.2348.

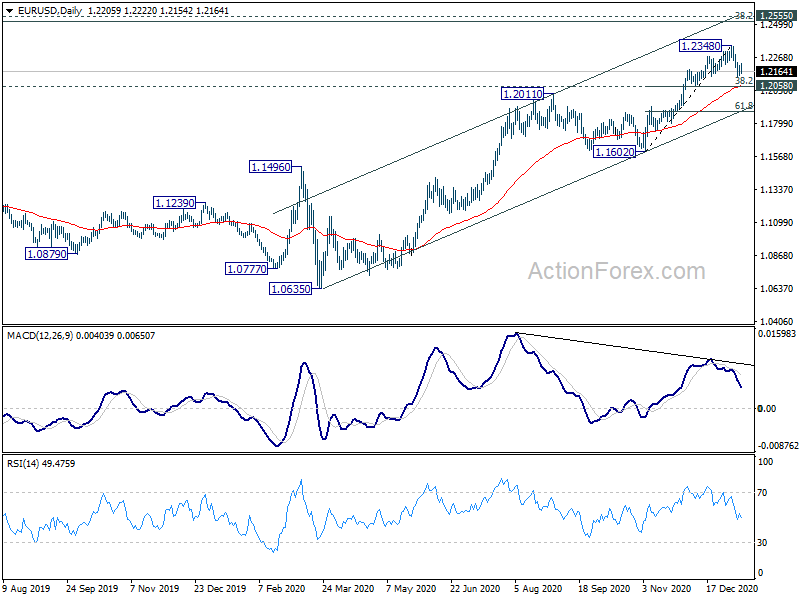

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. We’d be alerted to topping sign around 1.2516/55. But sustained break there will carry long term bullish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Dec | 9.20% | 9.20% | 9.10% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Dec P | 8.70% | 8.00% | 8.60% | |

| 07:00 | EUR | Germany WPI M/M Dec | 0.60% | 0.10% | 0.10% | |

| 09:00 | EUR | Italy Industrial Output M/M Nov | -1.40% | 0.00% | 1.30% | 1.40% |

| 10:00 | EUR | Eurozone Industrial Production M/M Nov | 2.50% | 0.30% | 2.10% | 2.30% |

| 13:30 | USD | CPI M/M Dec | 0.40% | 0.40% | 0.20% | |

| 13:30 | USD | CPI Y/Y Dec | 1.40% | 1.30% | 1.20% | |

| 13:30 | USD | CPI Core M/M Dec | 0.10% | 0.10% | 0.20% | |

| 13:30 | USD | CPI Core Y/Y Dec | 1.60% | 1.60% | 1.60% | |

| 15:30 | USD | Crude Oil Inventories | -3.2M | -8.0M |