{kind=link}

Sterling surges broadly today after BoE Governor criticized that negative interest rates have a lot of issues. Commodity currencies are currently the next strongest, reversing some of this week’s pull back. On the other hand, Dollar is now the weakest one for the day, as the near term recovery lost momentum. Yen and Euro are the next weakest for the moment.

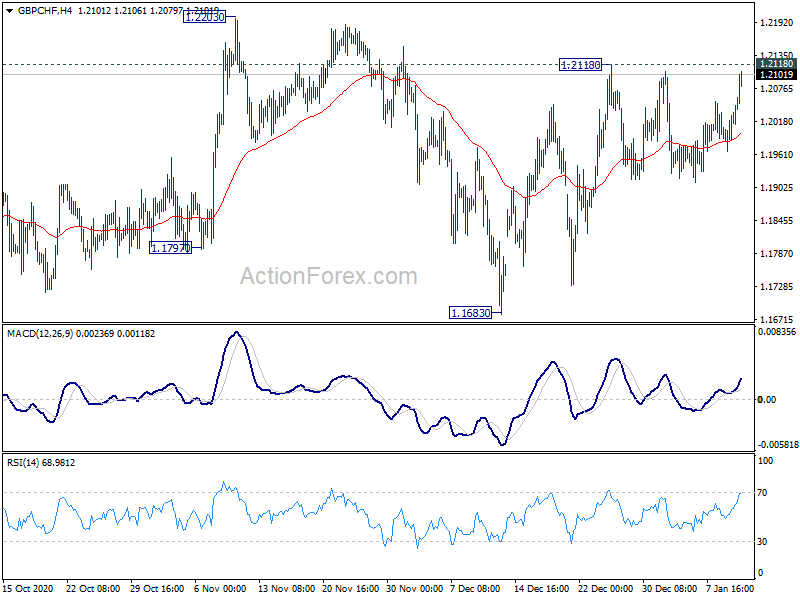

Technically, focus remain on whether USD/CHF would break through 0.8918 resistance, and whether USD/JPY would break through near term channel. Or, the two pairs would be rejected to end near term recovery. Another focus is whether the Pound would solidify today’s rally. GBP/JPY has already broken 141.34 temporary top. 1.2118 resistance in GBP/CHF will be watched.

In Europe, currently, FTSE is down -0.74%. DAX is down -0.10%. CAC is down -0.19%. Germany 10-year yield is up 0.021 at -0.473. Earlier in Asia, Nikkei rose 0.09%. Hong Kong HSI rose 1.32%. China Shanghai SSE rose 2.18%. Singapore Strait Times dropped -0.23%. Japan 10-year JGB yield dropped -0.0022 to 0.037.

BoE Bailey: There are a lot of issues with negative interest rates

BoE Governor Andrew Bailey said today that negative rates are a “controversial issue” and there are “a lot of issues” with it. He added that negative rates would complicate banks’ efforts to earn a rate of return, and potentially hurt their lending.

Bailey added that “we’re in a world of low rates for a long period of time”. Outlook for interest rates “hinges on productivity growth”. At this point, it’s “too soon to reach any conclusion about the need for future stimulus.

On the economy, he said, We’re”in a very difficult period at the moment and there’s no question that it’s going to delay, probably, the trajectory.”

ECB Schnabel: Predominant problem is weak demand, not capacity bottlenecks

ECB Executive Board member Isabel Schnabel said in an interview that “inflation is not dead. Compared to the long course of economic history, there are only a relatively few years in which inflation was as low as it is now”. In particular, the decline in energy prices was a ” major reason why inflation fell sharply in 2020″. Temporary sales tax reductions also has a “dampening effect”, especially in Germany.

For now, there are no signs that one should worry about inflation being too high”. She added. “We are experiencing a pronounced weakness in demand. It is to be feared that the crisis will have longer-term effects on the labor market.

“Overall, the predominant problem is that economic demand is too weak, not that there are capacity bottlenecks, which is why prices are likely to rise too slowly,” she said.

Germany BDI expects Joe Biden and China to boost industrial sector export this year

Germany’s BDI industry association expects the country’s GDP to grow 4.4% this year. The export-oriental industrial sector would drive recovery with 6% growth.

BDI President Siegfried Russwurm said, “the election of Joe Biden as U.S. President facilitates the path for multilateral solutions and joint initiatives for fair competition on the world markets.”

“Our companies will benefit from both China, the driver of global growth, and the agreement on an investment pact, even if it is not perfect,” he added.

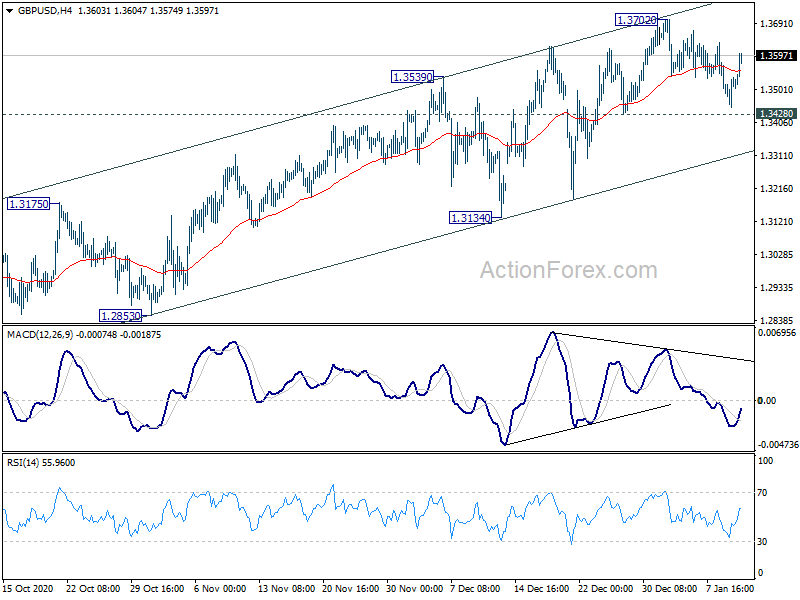

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3452; (P) 1.3513; (R1) 1.3574; More…

GBP/USD rebounds notably today but stays below 1.3702 resistance. Intraday bias remains neutral first and another rise is in favor. On the upside, break of 1.3702 will resume whole rise from 1.1409 to 61.8% projection of 1.1409 to 1.3482 from 1.2675 at 1.3956. On the downside, break of 1.3428 will indicate short term topping, and turn bias to the downside for deeper pull back, to 1.3134 support next.

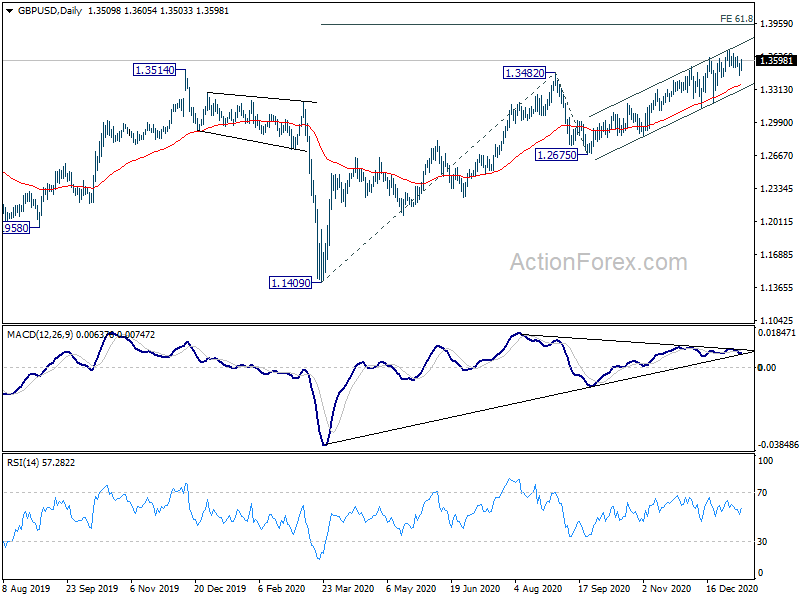

In the bigger picture, the break of 1.3514 structural resistance and sustained trading above 55 month EMA (now at 1.3328) should confirm medium term bottoming at 1.1409. Rise from there should now extend to 1.4376 resistance and above. This will remain the favored case as long as 1.2675 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Dec | 6.20% | 6.50% | 6.30% | 6.20% |

| 23:50 | JPY | Current Account (JPY) Nov | 2.34T | 2.00T | 1.98T | |

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Dec | 4.80% | 5.90% | 7.70% | |

| 05:00 | JPY | Eco Watchers Survey: Current Dec | 35.5 | 36.2 | 45.6 | |

| 11:00 | USD | NFIB Business Optimism Index Dec | 95.9 | 100.7 | 101.4 |