{kind=link}

Australian Dollar weakest broadly today after China intensified the trade tensions with banning Australia’s coal imports. Markets are relatively mixed elsewhere, with some softness in both Yen and Swiss Franc. The Pound’s rebound is fading as for now, there is no confirmation on whether there would be a Brexit trade deal or not. Though, it’s currently the slightly stronger one, together with Euro.

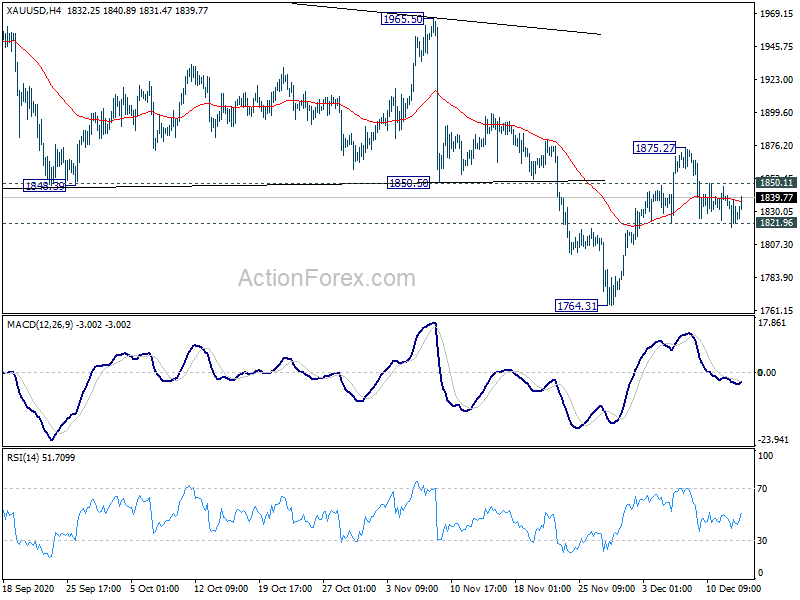

Technically, Dollar’s downside breakout failed yesterday. But focus will remain on 1.2177 resistance in EUR/USD, 0.8851 in USD/CHF and 1.2706 support in USD/CAD to indicate resumption of Dollar’s selloff. Gold also rebounded notably after breaching 1821.96 minor support. That retains near term bullishness and focus is back on 1850.11 minor resistance, to further affirm it.

In Asia, Nikkei closed down -0.17%. Hong Kong HSI is down -0.55%. China Shanghai SSE is down -0.02%. Singapore Strait Times is down -0.23%. Japan 10-year JGB yield is down -0.0050 at 0.009. Overnight, DOW dropped -0.62%. S&P 500 dropped -0.44%. NASDAQ rose 0.50%. 10-year yield dropped -0.001 to 0.892.

Australia Birmingham: China is a significant coal market, but not our largest

In response to news that China has blocked Australian coal imports, Trade Minister Simon Birmingham said he has not ruled out taking China to the WTO. Though, he emphasized, “we do have to make sure that we have the facts behind us when it comes to undertaking WTO challenges.”

“In terms of coal exports, it is important to recognise that although China is a significant market, it is not our largest market,” he added. “We do have significant markets in Japan … with India, strong growth recently in relation to Vietnam.” “We continue to work in a range of other markets where our government has secured trade agreements to develop trade ties to make sure that all of those exporters can have as many choices available to them as possible.”

Trade tensions between the two countries escalated in the past few months as China has recently increased tariffs on Australian wine and barley and blocked imports on lamb, beef, lobsters and other goods.

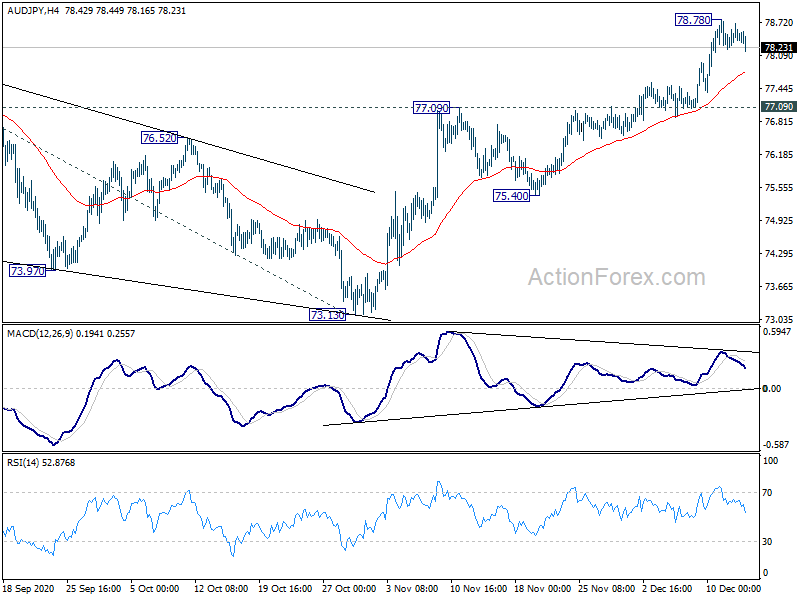

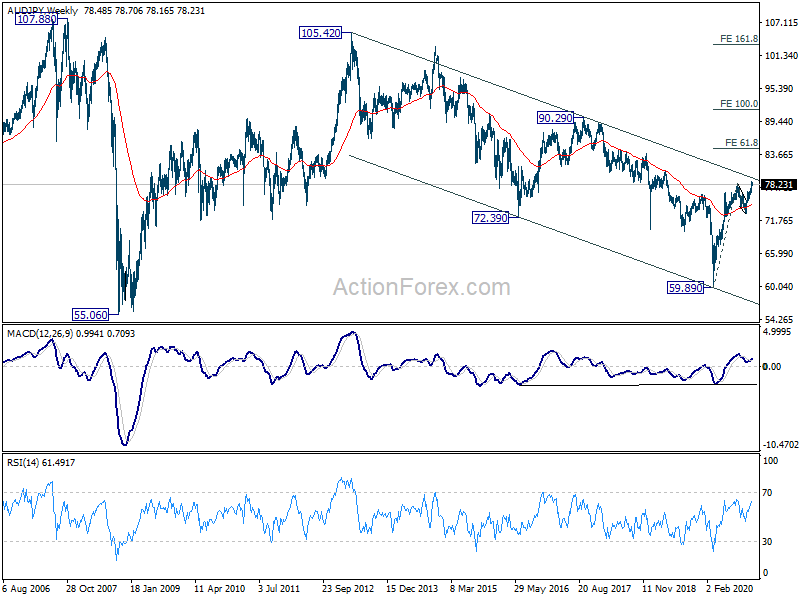

AUD/JPY retreats mildly but further rise expected with 77.09 support intact

AUD/JPY dips mildly today as Australia Dollar pulls back broadly. This is in response to China’s new hostile trade action in banning Australian coals. Though, the retreat in AUD/JPY is shallow so far and doesn’t warrant a reversal yet. Further rise will remain in favor as long as 77.09 resistance turned support holds.

Still, we’d emphasize that the real test lies in long term channel resistance (started back at 105.42 in 2013). Sustained break there will be a strong signal of an emerging bullish trend and pave the way to 61.8% projection of 59.89 to 78.46 from 73.13 at 84.60 in the medium term. However, rejection by the channel resistance, followed by break of 77.09 support, will retain long term bearishness and turn focus back to 73.13 support.

RBA Minutes: Recovery is underway but uneven and protracted

In the minutes of December 1 monetary policy meeting, RBA said economic recovery in Australia was “under way” and and recent data had “generally been better than expected”. Employment rate was “likely to peak lower than the 8 per cent rate expected”. Though, recovery was still expected to be “uneven and protracted”, dependent on “significant policy support and favorable health outcomes”. High unemployment rate and excess capacity were expected to result in “subdued wages growth in inflation over coming years”.

RBA reiterated, “the Bank remained prepared to purchase bonds in whatever quantity required to achieve the 3-year yield target”. The size of bond purchases is kept “under review” and it’s “prepared to do more if necessary. Also, RBA ” remains committed to not increasing the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range”. No increase in cash rate is expected for “at least 3 years”. Also, ” it would be appropriate to remove the yield target before the cash rate itself were increased.”

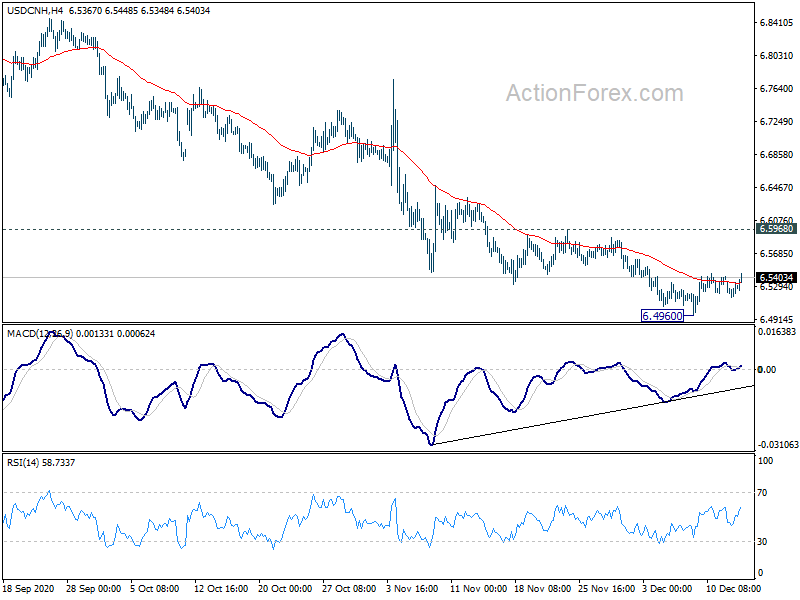

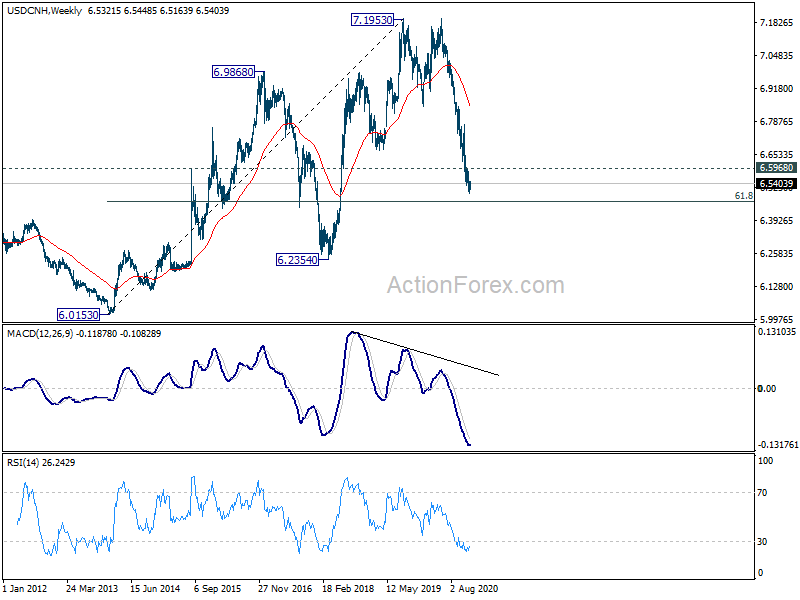

USD/CNH staying in consolidation after strong China data, down trend in force

China’s industrial production rose 7.0% yoy in November, up from October’s 6.9% yoy, matched expectations. Retail sales rose 5.0% yoy, up from October’s 4.3% yoy, but missed expectation of 5.1% yoy. Auto sales rose 11.8% yoy while household appliances sales rose 5.1% yoy. Communications equipment sales even jumped 43.6% yoy. Fixed asset investment rose 2.6% ytd yoy, up from October’s 1.8% ytd yoy, beat expectation of 2.6%. Private sector fixed-asset investment rose 0.2% ytd yoy, turned positive from October -0.7%.

USD/CNH recovers mildly today as consolidation form 6.4960 extends. Downside momentum has been diminishing as seen in 4 hour MACD. But outlook stays bearish as long as 6.5968 resistance holds. The down trend from 7.1953 medium term top should still extend to 61.8% retracement of 6.0153 to 7.1953 at 6.4661. There we’d expect strong support to bring a sustainable corrective rebound.

Looking ahead

UK employment data will be the main focus in European session. Swiss will release PPI while Italy will release trade balance. later in the day, US will release import price index and industrial production. Canada will release housing starts and manufacturing sales.

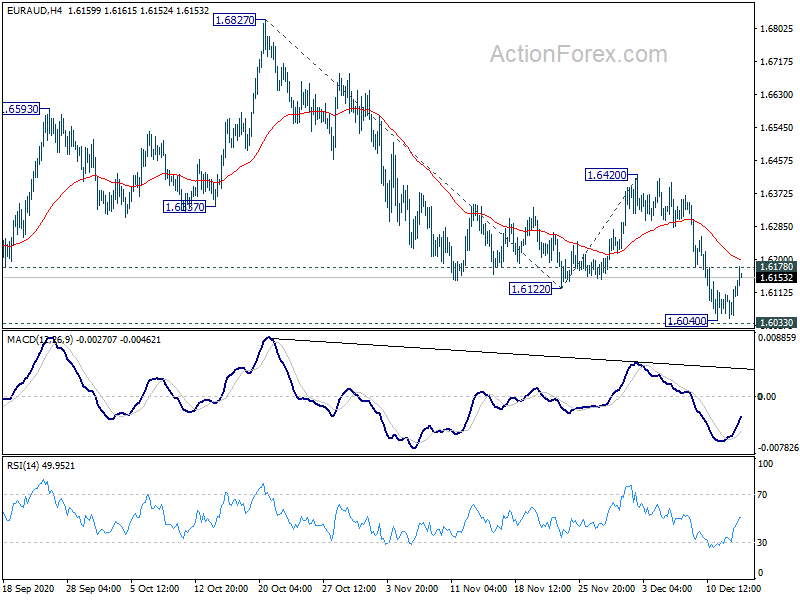

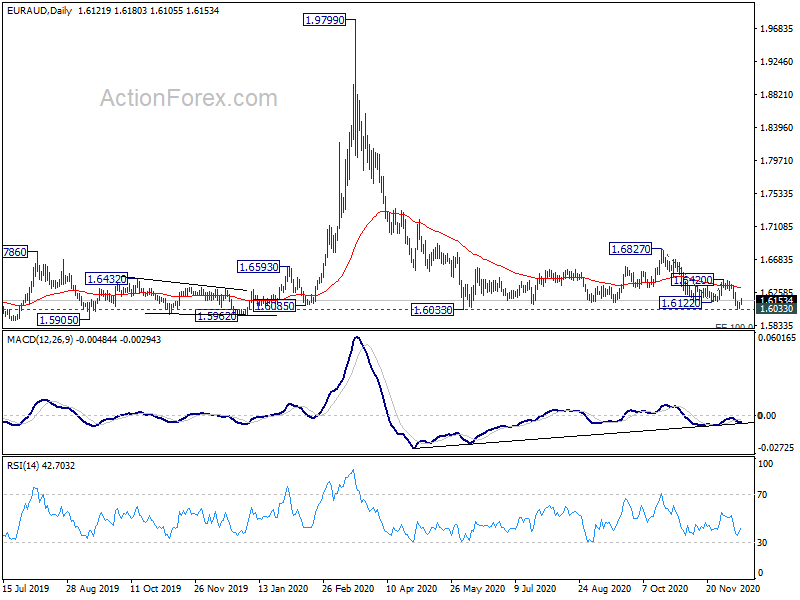

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6070; (P) 1.6100; (R1) 1.6153; More…

Intraday bias in EUR/AUD is turned neutral with today’s recovery. On the upside, firm break of 1.6178 minor resistance will suggest short term bottoming, after drawing support from 1.6033 low. Intraday bias will be turned back to the upside for 1.6420 resistance first. Decisive break there would confirm that consolidation pattern from 1.6033 has started another rise leg, back towards 1.6827 resistance. On the downside, however, decisive break of 1.6033 will resume larger down trend from 1.9799. Next near term target is 100% projection of 1.6872 to 1.6122 from 1.6420 at 1.5984.

In the bigger picture, price action from 1.9799 are seen as developing into a corrective pattern. The question is whether it’s a sideway pattern or a deep correction. On the downside, sustained break of 1.6033 will suggest it’s the latter case and target 61.8% retracement of 1.1602 (2012 low) to 1.9799 at 1.4733. On the upside, break of 1.6827 resistance will favor the former case and bring stronger rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | Westpac Consumer Survey Q4 | 106 | 95.1 | ||

| 0:30 | AUD | RBA Meeting Minutes | ||||

| 2:00 | CNY | Retail Sales Y/Y Nov | 5.00% | 5.10% | 4.30% | |

| 2:00 | CNY | Industrial Production Y/Y Nov | 7.00% | 7.00% | 6.90% | |

| 2:00 | CNY | Fixed Asset Investment YTD Y/Y Nov | 2.60% | 2.60% | 1.80% | |

| 6:45 | CHF | SECO Economic Forecasts | ||||

| 7:00 | GBP | Claimant Count Change Nov | 10.5K | -29.8K | ||

| 7:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | 2.30% | 1.30% | ||

| 7:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | 2.60% | 1.90% | ||

| 7:00 | GBP | ILO Unemployment Rate (3M) Oct | 5.10% | 4.80% | ||

| 7:30 | CHF | Producer and Import Prices M/M Nov | 0.00% | |||

| 7:30 | CHF | Producer and Import Prices Y/Y Nov | -2.90% | |||

| 9:00 | EUR | Italy Trade Balance (EUR) Oct | 5.40B | 5.85B | ||

| 13:15 | CAD | Housing Starts Nov | 215K | |||

| 13:30 | CAD | Manufacturing Sales M/M Oct | 1.50% | |||

| 13:30 | USD | Import Price Index M/M Nov | 0.30% | -0.10% | ||

| 14:15 | USD | Industrial Production M/M Nov | 0.30% | 1.10% | ||

| 14:15 | USD | Capacity Utilization Nov | 73.00% | 72.80% |