{kind=link}

The global markets are quickly back in risk-on mode today. DOW future is back above 30k handle, as coronavirus vaccine rollout began. There seems to be some progress in the US Congress for fresh fiscal stimulus too. Dollar is under broad based selling pressure, followed by Canadian and Yen for the moment.

On the other hand, Sterling is firstly lifted as Brexit trade talks extended for an “extra mile”. It’s also reported that EU chief negotiator Michel Barnier told EU ambassadors that a deal could come as soon as this week. It’s said that UK has made concessions on fair competition, in exchange for EU’s softening its stance on fishing rights.

Technically, no key levels are broken in Sterling pairs yet. A closer one is 1.3539 resistance in GBP/USD. Sustained break there will revive near term bullishness, for extending larger rise from 1.1409. EUR/USD is now eyeing equivalent resistance at 1.2177 too. USD/CHF is also pressing 0.8851 temporary low. USD/JPY has already breached 103.17 minor support. We’ll see if Dollar’s broad based selloff could materialize today.

In Europe, currently, FTSE is up 0.29%. DAX is up 1.26%. CAC is up 1.04%. Germany 10-year yield is up 0.0246 at -0.609. Earlier in Asia, Nikkei rose 0.30%. Hong Kong HSI dropped -0.44%. China Shanghai SSE rose 0.66%. Singapore Strait Times rose 1.29%. Japan 10-year JGB yield rose 0.0014 to 0.014.

EU von der Leyen: We want a level playing field with UK

European Commission President Ursula von der Leyen said today, “we are on the very last mile” on Brexit trade negotiations. “We want a level playing field, not only at the start but also over time … this is the architecture that we are building,” she said. “We’re fine about the architecture itself but the details, do they really fit?”

“We’re of course aware that time is short. The more time that goes by the less likely it is that we will have a deal in place on the first of January, that’s just a statement of fact,” Commission spokesman Daniel Ferrie told a news briefing separately, “I cannot say what may or may not happen over these days. But what I can say, though, is that we are fully dedicated to trying to reach a deal with the UK.”

Eurozone industrial production rose 2.1% mom in Oct, EU production up 1.9% mom

Eurozone industrial production rose 2.1% mom in October, slightly above expectation of 2.0% mom. Production of capital goods rose by 2.6% mom, intermediate goods by 2.1% mom, energy by 1.8% mom and durable consumer goods by 1.5% mom, while production of non-durable consumer goods remained unchanged.

EU industrial production rose 1.9% mom. Among Member States, for which data are available, the highest increases were registered in Belgium (+6.9%), Germany (+3.4%) and Slovenia (+3.1%). The largest decreases were observed in Denmark (-5.8%), Greece (-3.0%) and Lithuania (-1.7%).

ECB Panetta: Ready to adjust monetary instruments if downside risks materialize

ECB Executive Board member Fabio Panetta said “we can guarantee our commitment to support the recovery. For monetary policy, this means providing certainty about financing conditions well into the future. The PEPP envelope can be further expanded and extended, if warranted.”

“We stand ready to adjust all our instruments if downside risks to the outlook materialise, including those stemming from exchange rate dynamics,” he added. “An appreciation of the euro could significantly affect euro area inflation. There should be no doubt here: the ECB will not accept inflation settling at levels that are inconsistent with its aim.”

Bank of France revises down 2021 growth forecasts due to new restriction measures

Bank of France said in a report that “the rebound in the economy observed in the summer and early fall 2020 was very clear but it is temporarily interrupted by the resumption of the epidemic and the new health restriction measures put in place since October”. It also warned that at the start of 2021, “economic activity would be penalized by still constrained household consumption, with a gradual lifting of health measures”.

In it’s central forecasts, “the hypothesis is that the epidemic would not stop immediately and that the generalized deployment of vaccines would not be fully effective until the end of 2021. Still, the uncertainty is “high”. It projects French GDP to growth around 5% in 2021 and 2022, then easing to slightly more than 2% in 2023. 2021 growth projection was notably lower than September’s forecast of 7.4%.

Japan tankan large manufacturing rose to -10, non-manufacturing rose to -5

Japan Tankan large manufacturing index rose 17 points from -27 to -10 in Q4, above expectation of -15. Outlook also improvement to -8, up from -17, and beat expectation of -11. Non-manufacturing index rose 7 pts from -12 to -5, slightly above expectation of -6. Non-manufacturing outlook rose from -11 to -6, above expectation of -7. However, all industry capex dropped -1.2%, much worse than expectation of -0.1%.

The set of data would affirm BoJ’s decision to stand pat on interest rate and QE program later in the week. Though, extensions of the emergence lending programs would be extended, as Japan is currently in a “relatively” serious third wave of coronavirus infections.

Also from Japan, tertairy industry index rose 1.0% mom in October versus expectation of 1.3% mom. Industrial production was finalized at 4.0% mom in October.

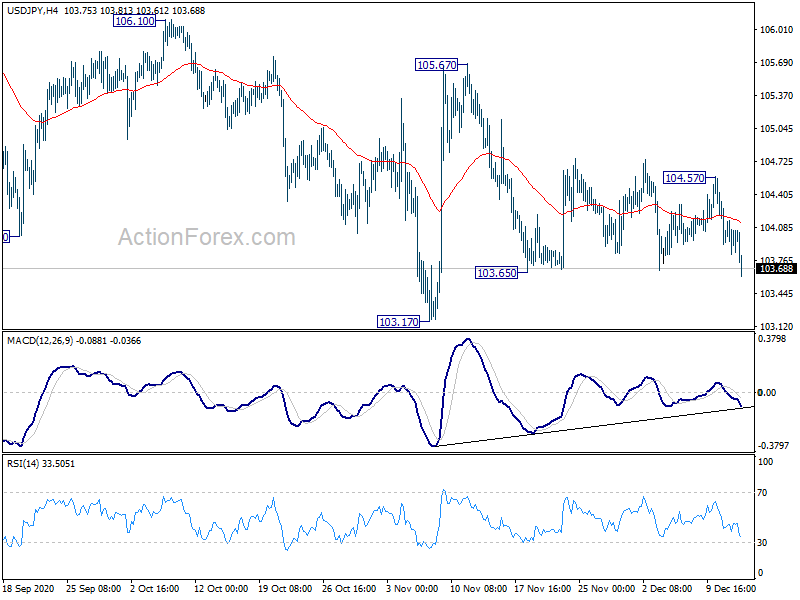

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 103.82; (P) 104.06; (R1) 104.28; More..

USD/JPY’s breach of 103.65 support suggests resumption of fall from 105.67. Intraday bias is back on the downside for 103.17 first. Break there will resume whole decline from 111.71 towards 101.18 low. For now, break of 104.57 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016). Hence, there is no clear indication of trend reversal yet. The down trend could still extend through 101.18 low. On the upside, break of 106.10 resistance is needed to be the first signal of medium term reversal. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | -10 | -15 | -27 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | -8 | -11 | -17 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q4 | -5 | -6 | -12 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q4 | -6 | -7 | -11 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | -1.20% | -0.10% | 1.40% | |

| 0:01 | GBP | Rightmove House Price Index M/M Dec | -0.60% | -0.50% | ||

| 4:30 | JPY | Tertiary Industry Index M/M Oct | 1.00% | 1.30% | 1.80% | 2.30% |

| 4:30 | JPY | Industrial Production M/M Oct F | 4.00% | 3.80% | 3.80% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | 2.10% | 2.00% | -0.40% | 0.10% |