{kind=link}

Sterling pares back some of its losses as traders refused to add to bet on no-deal Brexit for now. Though, the Pound remains generally weak in Asian session today. Markets are relatively quiet elsewhere with stocks trading in mixed mode. Treasury yields also gave back some of last week’s gains. Improvement in Australia business confidence and Japan’s fresh fiscal stimulus are unable to ignite any moves. Focus will turn to German ZEW economic sentiment first, with eyes on Brexit development and ECB later in the week.

Technically, Gold took out 1850 resistance overnight and further affirms the case of near term bullish reversal. But corresponding selloff was not seen in the greenback. EUR/USD is holding in consolidation below 1.2177 temporary top. AUD/USD and USD/CAD are both continuing to lose momentum. Focuses would be on 0.7351 minor support in AUD/USD and 1.2868 minor resistance in USD/CAD to gauge the chance of a near term recovery in Dollar.

In Asia, currently, Nikkei is down -0.34%. Hong Kong HSI is down -0.55%. China Shanghai SSE is down -0.13%. Singapore Strait Times is down -0.06%. Japan 10-year JGB yield is down -0.0020 at 0.024. Overnight, DOW dropped -0.49%. S&P 500 dropped -0.19%. NASDAQ rose 0.45%. 10-year yield dropped -0.041 to 0.928.

UK Johnson to travel to Brussels as significant differences remain on three critical Brexit issues

UK Prime Minister Boris Johnson will travel to Brussels for an in-person meeting with the European commission President Ursula von der Leyen, for last ditch effort in making the Brexit trade agreement. The meeting should be held in the coming days, possible on Wednesday or Thursday. A joint announcement confirmed after both leaders talked on phone yesterday.

Nevertheless, the statement maintained that “the conditions for finalizing an agreement are not there due to the remaining significant differences on three critical issues: level playing field, governance and fisheries”.

UK BRC like-for-like sales rose 7.7% yoy, largest gain since June

According to BRC, UK’s year-on-year total retail sales growth slowed to 0.9% in November, down from October’s 4.9% yoy. That’s the weakest spending growth since the -5.9% fall in May. Like-for-like sales rose by 7.7% yoy, largest gain since June.

“Some retailers were able offset a proportion of lost sales through greater online and click-and-collect sales, ensuring they could still serve their customers,” Helen Dickinson, chief executive of the BRC, said.

Japan PM Suga announced JPY 73.5T fresh stimulus

Japanese Prime Minister Yoshihide Suga announced today a fresh economic stimulus package worth JPY 73.6T. Suga said, “we will maintain employment, keep businesses going, revive the economy and open a path to growth including through green and digital technology.”

A batch of economic data is released from Japan today. Q3 GDP growth was finalized at 5.3% qoq, revised up from 5.0% qoq. In annualized term, GDP grew 22.9%, revised up from 21.4%. In October, labor cash earnings dropped -0.8% yoy versus expectation of -0.7% yoy. Household spending rose 1.9% yoy versus expectation of 2.5% yoy. Current account surplus widened to JPY 1.98%. In November, bank lending rose 6.3% yoy.

Australia NAB business confidence rose to 12, but no improvement in employment

Australia NAB Business Confidence rose to 12 in November, up from 3. Business Conditions rose to 9, up from 2. Trading conditions improved to 17, from 7. Profitability conditions rose to 15, up from 5. Employment conditions, however, was unchanged at -5. NAB noted, “Overall both confidence and conditions are now above average, and stronger than the period right before the pandemic – albeit this partly reflects some ‘snapback’ following the containment of the virus.”

However, “the employment index did not see a further improvement and remains in negative territory. So, while activity is picking up as the economy reopens, businesses are yet to move back into hiring mode. This is not completely surprising with the labour market often lagging developments in activity – so we will keep closely watching this measure,” said Alan Oster, NAB Group Chief Economist

Also released, house price index rose 0.8% qoq in Q3, much better than expectation of -0.4% qoq.

Looking ahead

France will release employment and trade balance. Swiss will release unemployment rate. Eurozone will release GDP revision. Germany will release ZEW economic sentiment. Later in the day, US will release non-farm productivity.

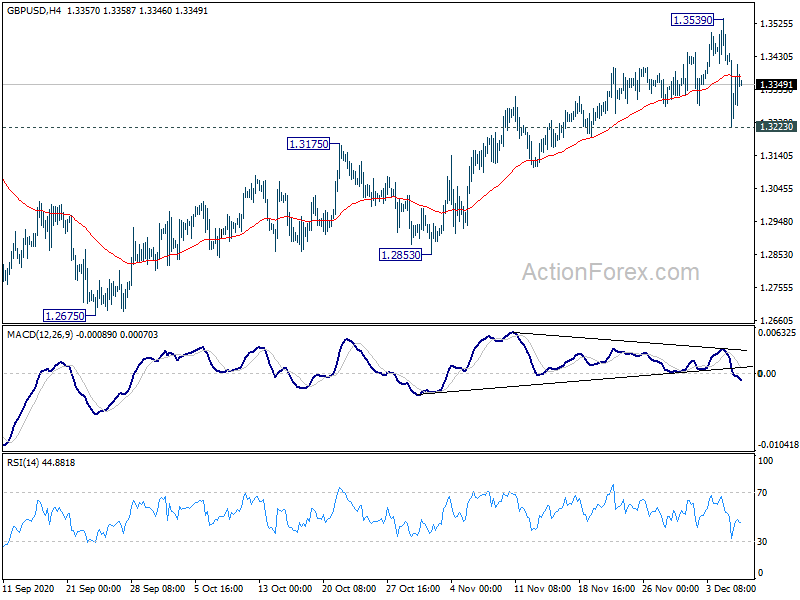

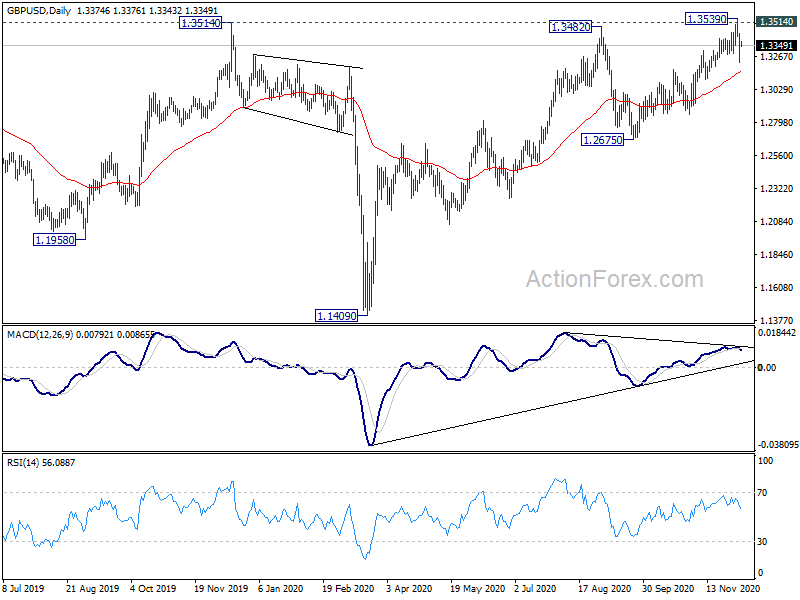

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3256; (P) 1.3347; (R1) 1.3468; More…

GBP/USD recovers notably after hitting 1.3223 and intraday bias is turned neutral first. We’re holding on to the view that a short term top was formed at 1.3539, and deeper fall is in favor. Break of 1.3223 will target 55 day EMA (now at 1.3162) first. Sustained break there will confirm another rejection by 1.3514 key resistance. Deeper fall should be seen back to 1.2675 support next. For now, risk will stay on the downside as long as 1.3539 resistance holds, in case of recovery.

In the bigger picture, focus stays on 1.3514 key resistance. Decisive break there should also come with sustained trading above 55 month EMA (now at 1.3308). That should confirm medium term bottoming at 1.1409. Outlook will be turned bullish for 1.4376 resistance and above. Nevertheless, rejection by 1.3514 will maintain medium term bearishness for another lower below 1.1409 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q F | 5.30% | 5.00% | 5.00% | |

| 23:50 | JPY | GDP Deflator Y/Y F | 1.20% | 1.10% | 1.10% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | -0.80% | -0.70% | -0.90% | -1.30% |

| 23:30 | JPY | Overall Household Spending Y/Y Oct | 1.90% | 2.50% | -10.20% | |

| 23:50 | JPY | Bank Lending Y/Y Nov | 6.30% | 6.30% | 6.20% | 6.10% |

| 23:50 | JPY | Current Account (JPY) Oct | 1.98T | 1.83T | 1.35T | |

| 00:01 | GBP | BRC Retail Sales Monitor Y/Y Nov | 7.70% | 5.20% | ||

| 00:30 | AUD | House Price Index Q/Q Q3 | 0.80% | -0.40% | -1.80% | |

| 00:30 | AUD | NAB Business Confidence Nov | 12 | 5 | ||

| 05:00 | JPY | Eco Watchers Survey: Current Nov | 52.6 | 54.5 | ||

| 06:30 | EUR | France Nonfarm Payrolls Q/Q Q3 F | 1.80% | |||

| 06:45 | CHF | Unemployment Rate Nov | 3.40% | 3.30% | ||

| 07:45 | EUR | France Trade Balance (EUR) Oct | -5.5B | -5.7B | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 | 12.60% | 12.60% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 F | 0.90% | 0.90% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | 45.2 | 39 | ||

| 10:00 | EUR | Germany ZEW Current Situation Dec | -69 | -64.3 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 37.5 | 32.8 | ||

| 11:00 | USD | NFIB Business Optimism Index Nov | 102.6 | 104 | ||

| 13:30 | USD | Nonfarm Productivity Q3 | 4.90% | 4.90% | ||

| 13:30 | USD | Unit Labor Costs Q3 | -8.90% | -8.90% |