{kind=link}

Dollar’s selloff accelerates today and better than expected jobless claim data provide no support. European majors are generally firm, with Sterling leading the way this time. But the rally in the Pound is unconvincing so far, with uncertainties over Brexit trade talks. Commodity currencies are relatively mixed, with Canadian Dollar being the weakest.

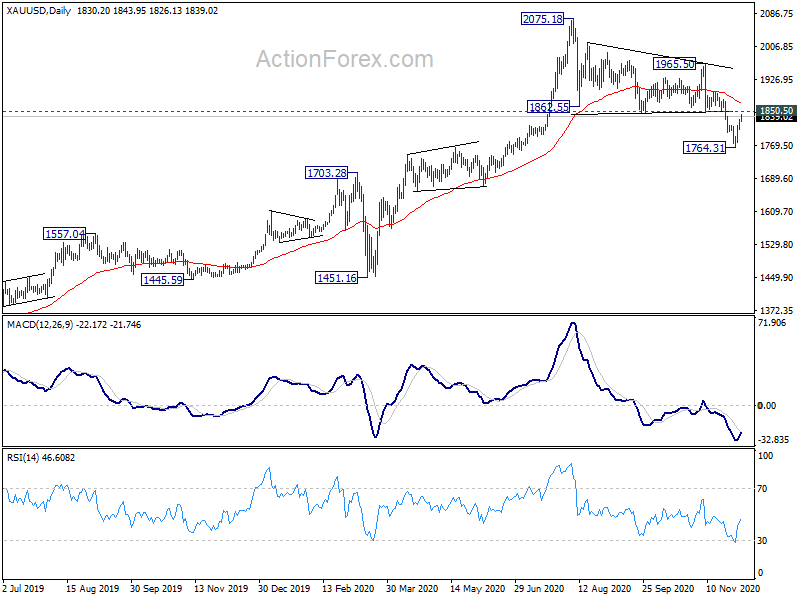

Technically, focus is back on 1850.50 support turned resistance in Gold after the strong rebound in the past few days. Decisive break there will suggest that the correction from 2075.18 has completed, slightly earlier than expected. Sustained break of 55 day EMA will add further credence to the case and target 1965.50 resistance and above. That would give further selling pressing to Dollar.

In Europe, currently, FTSE is up 0.30%. DAX is down -0.49%. CAC is down -0.41%. Germany 10-year yield is down -0.0249 at -0.542. Earlier in Asia, Nikkei rose 0.03%. Hong Kong HSI rose 0.74%. China Shanghai SSE dropped -0.21%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield dropped -0.0002 to 0.026.

US initial jobless claims dropped to 712k, continuing claims down to 6.2m

US initial jobless claims dropped -75k to 712k in the week ending November 28, below expectation of 770k. Four-week moving average of initial claims dropped -11.25k to 739.5k. Continuing claims dropped -569k to 5520k in the week ending November 21. Four-week moving average of continuing claims dropped -426k to 6194k.

Eurozone retail sales rose 1.5% mom in Oct

Eurozone retail sales rose 1.5% mom in October, well above expectation of 0.5% mom. Volume of retail trade increased by 2.0% mom for both non-food products and for food, drinks and tobacco, while automotive fuels fell by 3.7% mom.

EU retail sales also rose 1.5% mom. Among Member States for which data are available, the highest increases in the total retail trade volume were observed in Denmark (+8.3%), Croatia (+6.5%) and France (+2.8%), while decreases were registered in Slovenia (-1.4%), Slovakia (-1.2%), the Netherlands (-0.7%) and Luxembourg (-0.3%).

Eurozone PMI services finalized at 41.7, composite at 45.3

Eurozone PMI Services was finalized at 41.7 in November, down from October’s 46.9. PMI Composite was finalized at 45.3, down from prior month’s 50.0. Looking at some members states, Germany PMI Composite dropped to 51.7, Ireland dropped to 47.7, Italy dropped to 42.7, Spain dropped to 41.7, France dropped to 40.6.

Chris Williamson, Chief Business Economist at IHS Markit said: “The eurozone economy slipped back into a downturn in November as governments stepped up the fight against COVID-19, with business activity hit once again by new restrictions to fight off second waves of virus infections… However, this is a decline of far smaller magnitude than seen in the spring… The fourth quarter will nevertheless likely see the eurozone economy take another major step backwards, with especially steep downturns suffered in France, Spain and Italy.”

UK PMI services finalized at 47.6, composite at 49.0

UK PMI Services was finalized at 47.6 in November, down from October’s 51.4. It’s the first contraction reading in five months. PMI Composite was finalized at 49.0, down from October’s 52.1, first contraction since June amid national lockdowns. Markit also noted the fastest drop in employment for three months. Though, year-ahead business optimism hit nine-month high.

Tim Moore, Economics Director at IHS Markit: “New lockdown measures and tighter pandemic restrictions unsurprisingly tipped UK private sector output back into decline during November…. Hopes that the pandemic will be brought under control from an effective vaccine resulted in a sharp improvement in business optimism during November. Across the UK private sector as a whole, confidence about the year ahead outlook reached its highest since March 2015. That said, survey respondents also cited rising business uncertainty in the short-term, largely due to ongoing restrictions on trade, which contributed to another round of job cuts and efforts to rein in discretionary spending during November.”

China PMI services rose to 57.8, second highest in a decade

China Caixin PMI Services rose to 57.8 in November, up from 56.7, above expectation of 56.5. It’s also the second quickest expansion rate since April 2010. Employment growth was strongest since October 2010 while input costs rose at sharpest pace for over a decade. PMI Composite rose from 55.7 to 57.5, best reading since March 2010.

Wang Zhe, Senior Economist at Caixin Insight Group said: “We expect the economic recovery in the post-epidemic era to continue for several months. At the same time, deciding how to gradually withdraw the easing policies launched during the epidemic will require careful planning as uncertainties still exist inside and outside China.”

Australia exports rose 5% mom in Oct, imports rose 1% mom

In October, Australia’s exports of goods and services rose 5% mom to AUD 35.72B. Imports of goods and services rose 1% mom to AUD 28.26B. Trade surplus came in at AUD 7.46B, above expectation of AUD 5.83B.

AiG Performance of Construction Index rose 2.6 pts to 55.3 in November, a second consecutive month of positive conditions, and the strongest monthly result since April 2018.

From New Zealand, building permits rose 8.8% mom in October. ANZ commodity price rose 0.9% in November.

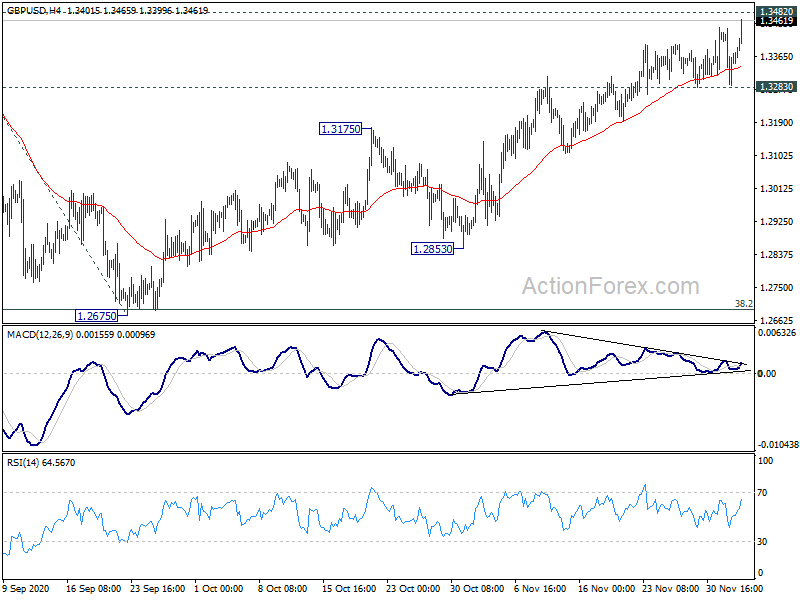

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3289; (P) 1.3365; (R1) 1.3442; More…

Focus is immediately on 1.3482 resistance in GBP/USD with today’s rise. Decisive break of 1.3482 will confirm resumption of whole rise from 1.1409. Next target will be 61.8% projection of 1.1409 to 1.3482 from 1.2675 at 1.3956 next. On the downside, break of 1.3283 support will turn bias back to the downside, to extend the consolidation from 1.3482 with another falling leg.

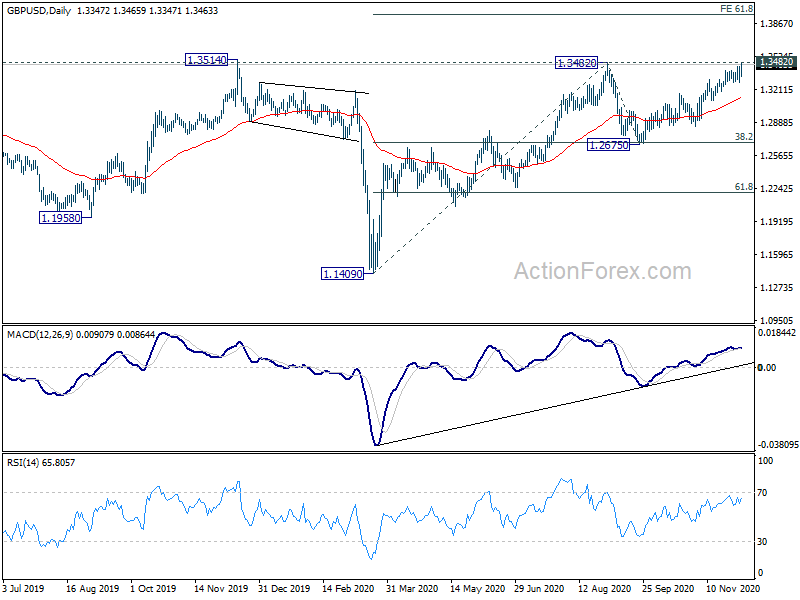

In the bigger picture, focus stays on 1.3514 key resistance. Decisive break there should also come with sustained trading above 55 month EMA (now at 1.3308). That should confirm medium term bottoming at 1.1409. Outlook will be turned bullish for 1.4376 resistance and above. Nevertheless, rejection by 1.3514 will maintain medium term bearishness for another lower below 1.1409 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Nov | 55.3 | 52.7 | ||

| 21:45 | NZD | Building Permits M/M Oct | 8.80% | 3.60% | ||

| 00:00 | NZD | ANZ Commodity Price Nov | 0.90% | 1.90% | 2.00% | |

| 00:30 | AUD | Trade Balance (AUD) Oct | 7.46B | 5.83B | 5.63B | 5.82B |

| 01:45 | CNY | Caixin Services PMI Nov | 57.8 | 56.5 | 56.8 | |

| 08:45 | EUR | Italy Services PMI Nov | 39.4 | 40.4 | 46.7 | |

| 08:50 | EUR | France Services PMI Nov F | 38.8 | 49.1 | 49.1 | |

| 08:55 | EUR | Germany Services PMI Nov F | 46 | 46.2 | 46.2 | |

| 09:00 | EUR | Eurozone Services PMI Nov F | 41.7 | 41.3 | 41.3 | |

| 09:30 | GBP | Services PMI Nov | 47.6 | 45.8 | 45.8 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | 1.50% | 0.50% | -2.00% | -1.70% |

| 12:30 | USD | Challenger Job Cuts Y/Y Nov | 45.40% | 60.40% | ||

| 13:30 | USD | Initial Jobless Claims (Nov 27) | 712 K | 770K | 778K | 787 K |

| 15:00 | USD | ISM Services PMI Nov | 56 | 56.6 | ||

| 15:30 | USD | Natural Gas Storage | -17B | -18B |