{kind=link}

Asian markets are generally mixed despite some solid data from Japan, China and New Zealand. Yen is lifted mildly by the relatively optimistic economic outlook. Sterling is also slightly firmer after UK Foreign Minister Dominic Raab indicated Brexit negotiations are “down to really two basic issues” only. Dollar, Canadian and Euro are the weaker ones. Nevertheless, major movement is found in Gold, which finally dives through 1800 handle.

Technically, focus will remain on whether Dollar would finally drop through key near term support levels, including 1.2011 resistance in EUR/USD, 0.7413 resistance in AUD/USD, and 1.2928 support in USD/CAD. Also, eyes will be on the next move in Sterling in response to Brexit talk progress, with focuses on 0.9004 resistance in EUR/GBP and 1.1989 support in GBP/CHF.

In Asia, currently, Nikkei is down -0.56%. Hong Kong HSI is down -0.50%. China Shanghai SSE is up 1.07%. Singapore Strait Times is down -0.49%. Japan 10-year JGB yield is up 0.0025 at 0.032.

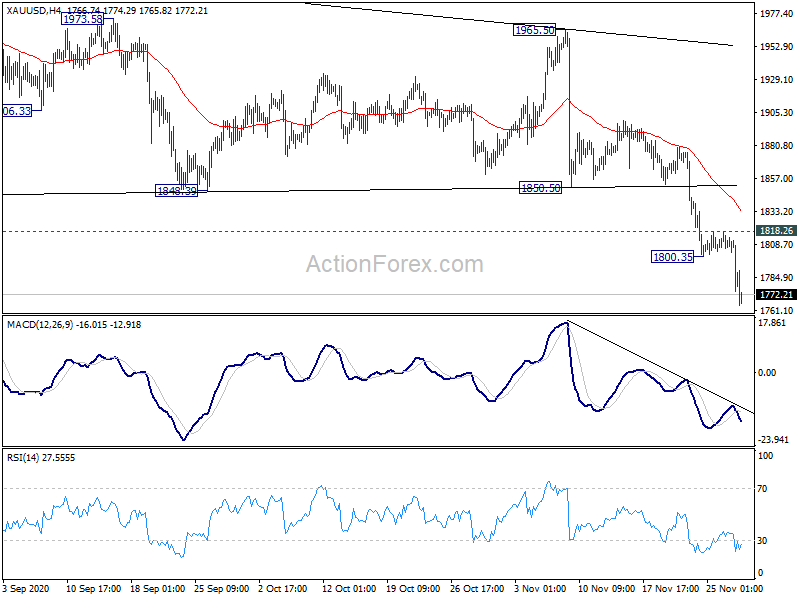

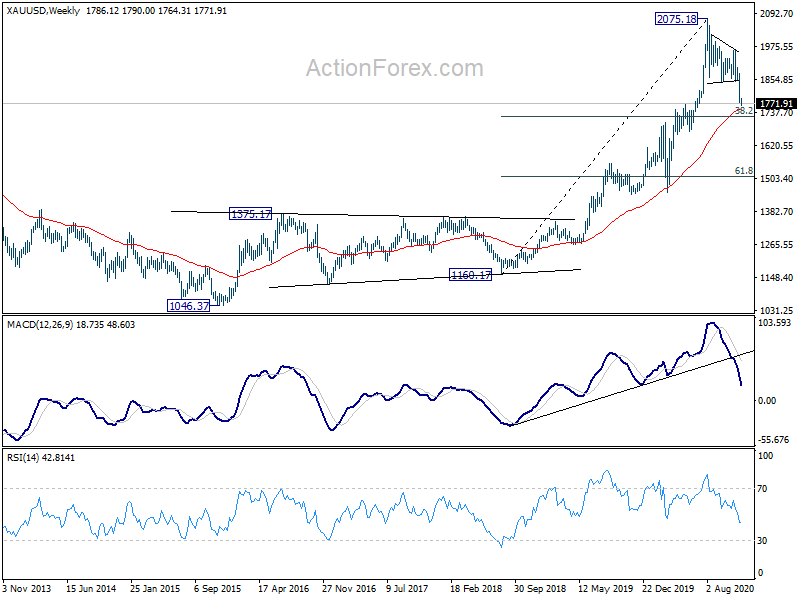

Gold selloff resumes, strong support expected around 1725

Gold’s selloff resumes today by breaking through 1800 handle and hits as low as 1764.31 so far. Further decline is now expected as long as 1818.26 resistance holds. Current decline from 2075.18 is seen as correcting whole up trend from 1160.17. Deeper fall should be seen to 55 week EMA (now at 1749.77) and possibly slightly below.

But we’d expect strong support from 38.2% retracement of 1160.17 to 2075.18 at 1725.64 to contain downside and bring rebound. However, Sustained break of 1749.77 could bring even deeper correction to 61.8% retracement at 1509.70.

Japan industrial production rose 3.8% mom in Oct, 5th straight month of growth

Japan industrial production rose 3.8% mom in October, well above expectation of 2.3% mom, and not much slower than September’s 3.9% mom. It’s also the fifth straight month of increase. The Ministry of Economy, Trade and Industry also said manufacturers expected growth to continue with another 2.7% mom in November, but a decline of -2.4% mom in December.

Retail sales rose 6.4% yoy in October, matched expectations. That’s the first annual rise in eight months., following a -8.7% yoy decline in September.

China PMI manufacturing rose to 52.1 in Nov, highest in three years

The official China PMI Manufacturing rose to 52.1 in November, up from 51.4, above expectation of 51.5. That’s the highest reading in more than three years. It’s also the ninth straight month of growth reading. PMI Services rose to 56.4, up from 56.2, above expectation of 56.0.

According the Zhao Qinghe, the bureau’s senior statistician. Four factors grove manufacturing activity. Both supply and demand of Chinese manufactured goods continued to improve. Imports and exports steadily recovered. Prices of both raw materials and output rose. Prospect of manufacturers of all sizes also improved.

New Zealand ANZ business confidence jumped to -6.9 in Nov, surge in manufacturing

New Zealand ANZ Business Confidence jumped to -6.9 in November, well above preliminary reading of -15.6 and October’s final of -15.7. Manufacturing confidence surged 14.5 pts and turned positive to 6.7. Retail confidence and services confidence also rose 17.9 pts and 10.2 pts to -3.8 and -6.6 respectively. Agriculture and construction dropped by -2.4 and -15.8 to -52.4 and -3.3.

Activity Outlook rose to 9.1, versus preliminary reading of 4.6 and October’s 4.7. Manufacturing outlook rose 13.4 to 15.0. Construction rose 14.5 to 23.3. Services rose 3.2 to 9.2. But retail dropped -2.2 to 0 while agriculture dropped -5.1 to -9.1.

ANZ noted: “Monetary and fiscal policy have undoubtedly done their jobs this year. But it’s worth remembering that both work by bringing forward spending from the future. There’s no free lunch, and they need to be used judiciously. The true underlying momentum of the economy should become clearer over the next few months as the impact of one-offs fade, but the case for further life-support measures is becoming less clear by the day. And that’s certainly something to celebrate.”

From Australia, TD securities inflation rose 0.3% mom in November. Private sector credit rose 0.0% mom in October. Company gross operating profits rose 3.2% qoq in Q3.

Extremely busy week ahead

It’s an extremely busy week ahead on the data front. Important data to watch include US ISMs and employment, Eurozone CPI, Canada GDP and employment; Australia GDP; China PMIs etc. RBA rate decision and Fed Beige Book are unlikely to trigger much reactions, though. Here are some highlights for the week:

- Monday: Japan industrial production, retail sales, housing starts; New Zealand ANZ business confidence; Australia company operating profits, private sector credit; China PMIs; Swiss retail sales, KOF economic barometer; UK M4 money supply, mortgage approvals; Germany CPI flash; Canada building permits, current account, IPPI and RMPI; US Chicago PMI, pending home sales.

- Tuesday; Japan unemployment rate, capital spending, PMI manufacturing final; RBA rate decision, building approvals current account; China Caixin PMI manufacturing; Swiss GDP; Swiss PMI manufacturing; Germany unemployment; Eurozone PMI manufacturing final, CPI flash; UK PMI manufacturing final; Canada GDP, PMI manufacturing; US ISM manufacturing, construction spending.

- Wednesday: Japan monetary base, consumer confidence; Australia GDP; Germany retail sales; Swiss CPI; Eurozone PPI, unemployment rate; US ADP employment, Fed’s Beige book.

- Thursday: Australia AiG construction, trade balance; New Zealand building permits; China Caixin PMI services; Eurozone PMI services final, retail sales; UK PMI services final; US jobless claims; ISM non-manufacturing.

- Friday: Australia retail sales; Germany factory orders; UK PMI construction; Canada employment, trade balance; US non-farm payroll, trade balance, factory orders.

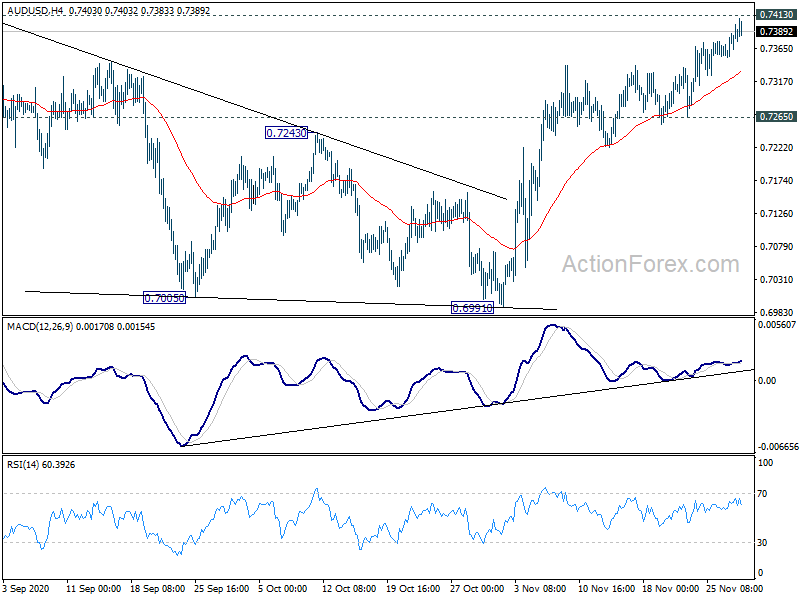

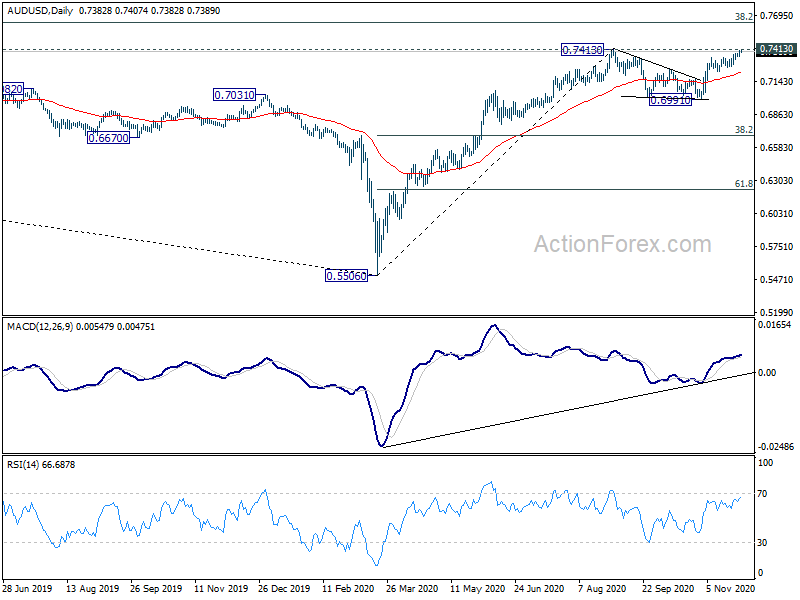

AUD/USD Daily Report

Daily Pivots: (S1) 0.7360; (P) 0.7379; (R1) 0.7406; More…

Intraday bias in AUD/USD remains on the upside for 0.7413 high. Decisive break there will resume whole rebound from 0.5506 and target 0.7635 long term fibonacci level. On the downside, however, break of 0.7265 support will extend the consolidation from 0.7413 with another falling leg. Intraday bias will be turned back to the downside for 0.6991 support instead.

In the bigger picture, the sustained trading above 55 week EMA (now at 0.6978) is a sign of medium term bullishness. Nevertheless, AUD/USD will still need to overcome 38.2% retracement of 1.1079 (2011 high) to 0.5506 (2020 low) at 0.7635 decisively to indicate completion of long term down trend from 1.1079. Otherwise, current rebound from 0.5506 could still turn out to be a correction in the long term down trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Oct P | 3.80% | 2.30% | 3.90% | |

| 23:50 | JPY | Retail Trade Y/Y Oct | 6.40% | 6.40% | -8.70% | |

| 0:00 | NZD | ANZ Business Confidence Nov | -6.9 | -15.6 | ||

| 0:00 | AUD | TD Securities Inflation M/M Nov | 0.30% | -0.10% | ||

| 0:30 | AUD | Private Sector Credit M/M Oct | 0.00% | 0.10% | 0.00% | |

| 0:30 | AUD | Company Gross Operating Profits Q/Q Q3 | 3.20% | 4.50% | 15.00% | 15.80% |

| 1:00 | CNY | NBS Manufacturing PMI Nov | 52.1 | 51.5 | 51.4 | |

| 1:00 | CNY | Non-Manufacturing PMI Nov | 56.4 | 56 | 56.2 | |

| 5:00 | JPY | Housing Starts Y/Y Oct | -8.3% | -8.60% | -9.90% | |

| 7:30 | CHF | Real Retail Sales Y/Y Oct | 0.30% | |||

| 8:00 | CHF | KOF Leading Indicator Nov | 101 | 106.6 | ||

| 9:30 | GBP | Mortgage Approvals Oct | 85K | 91K | ||

| 9:30 | GBP | M4 Money Supply M/M Oct | 1.00% | 0.90% | ||

| 13:00 | EUR | Germany CPI M/M Nov P | -0.70% | 0.10% | ||

| 13:00 | EUR | Germany CPI Y/Y Nov P | -0.20% | -0.20% | ||

| 13:30 | CAD | Industrial Product Price M/M Oct | -0.10% | |||

| 13:30 | CAD | Raw Material Price Index Oct | -2.20% | |||

| 13:30 | CAD | Current Account (CAD) Q3 | -8.63B | |||

| 13:30 | CAD | Building Permits M/M Oct | 17.00% | |||

| 14:45 | USD | Chicago PMI Nov | 59.2 | 61.1 | ||

| 15:00 | USD | Pending Home Sales M/M Oct | 1.00% | -2.20% |