{kind=link}

Dollar’s sell-off slowed mildly as stocks turned into consolidation ahead of Thanksgiving holiday in the US. But for now, the greenback remains the second worst performing for the week, just next to Yen, followed by Swiss Franc. Commodity currencies are strongest together with Sterling. Mixed economic data from US provided little inspirations to investors. It’s unlikely for FOMC minutes to have some drastic too.

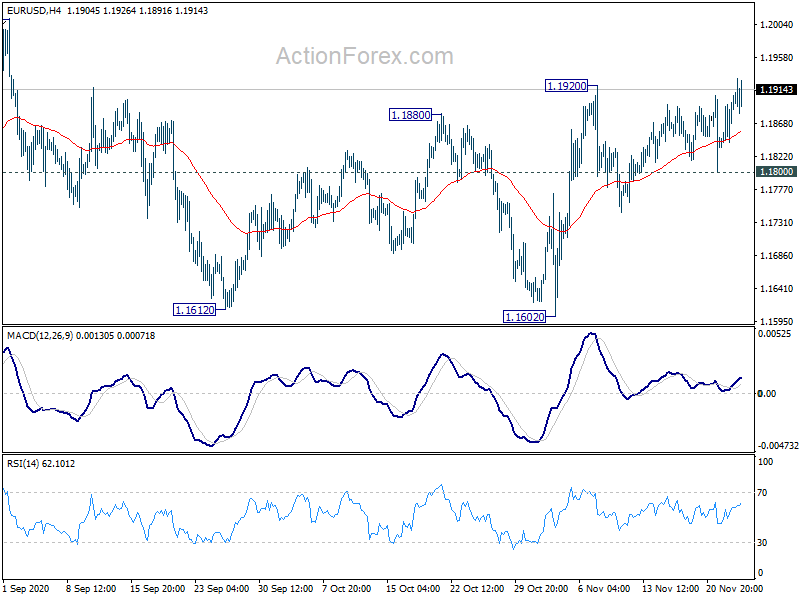

Technically, EUR/USD’s breach of 1.1920 resistance suggests that rebound from 1.1602 is resuming for 1.2011 high. GBP/USD is heading to equivalent resistance at 1.3482 while AUD/USD is targeting 0.7413 resistance. We’ll see if the greenback could finally break through these near term support levels before weekly close.

In other markets, DOW is currently down -0.55%. FTSE is down -0.62%. DAX is down -0.07%. CAC is up 0.11%. German 10-year yield is down -0.0084 at -0.569. Earlier in Asia, Nikkei rose 0.50%. Hong Kong HSI rose 0.31%. China Shanghai SSE dropped -1.56%. Singapore Strait Times dropped -0.76%. Japan 10-year JGB yield dropped -0.0090 to 0.018.

Mixed economic data released from US

Initial jobless claims rose 30k to 778k in the week ending November 21, well above expectation of 725k. Four-week moving average of initial claims rose 5k to 748.5k. Continuing claims dropped -229k to 6071k in the week ending November 14. Four-week moving average of continuing claims dropped -438k to 6165k.

Durable goods orders rose 1.3% mom to USD 240.8B in October, better than expectation of 1.0% mom. That’s the six consecutive months of increase. Ex-transport orders rose 1.3% mom, well above expectation of 0.4% mom. Ex-defense orders rose 0.2% mom. Transportation equipment, up five of the last six months, rose 1.2% mom.

Persona income dropped -0.7% mom in October, well below expectation of 0.1% rise. Spending rose 0.5%, versus expectation of 0.4% mom. Headline PCE price index slowed to 1.4% yoy while core PCE price index also slowed to 1.4%.

New home sales dropped to 999k in October, Goods trade deficit rose 1.2% mom to USD -80.3B. Wholesale inventories rose 0.9% to USD 646.2B.

GDP grew 33.1% annualized in Q3, according to the second estimate, comparing to Q2’s -31.4% annualized contraction. With the second estimate, upward revisions to nonresidential fixed investment, residential investment, and exports were offset by downward revisions to state and local government spending, private inventory investment, and personal consumption expenditures (PCE). Imports, which are a subtraction in the calculation of GDP, were revised up.

EU von der Leyen: Well prepared for a no-deal Brexit scenario

European Commission president Ursula von der Leyen said there were “genuine progress” in post-Brexit negotiations with the UK. She emphasized that “the next days are going to be decisive,” on whether a deal could be clinched.

“With very little time ahead of us, we will do all in our power to reach an agreement. We are ready to be creative. But we are not ready to put into question the integrity of our single market,” she added.

“We need to establish robust mechanisms, ensuring that competition is – and remains – free and fair over time. In the discussions about state aid, we still have serious issues, for instance when it comes to enforcement,” said von der Leyen.

She also reiterated, “the European Union is well prepared for a no-deal-scenario, but of course we prefer to have an agreement.”

ECB Mersch: Recalibration could be rectification or more targeted and focused

ECB Executive Board member Yves Mersch said in an interview that the second coronavirus lockdown in European has been “much less growth-damaging and much more targeted “. Still there is an “increase in fragmentation”, with divergence between services and manufacturing sectors. Some countries are more exposed to the pandemic consequences.

Overall, it’s “difficult to maintain positive growth going into the fourth quarter”. Germany might achieve it but others not. But it’s “premature to conclude that will last into next year with consecutive quarters of negative growth.

On ECB’s policies, Mersch said recalibration could be rectification, “simply an extension “on the time axis” or “of the volume or the intensity”. A second approach is “more targeted, or more focused, or on the contrary consider now untested instruments, a theoretical possibility in an all encompassing discussion.”

RBNZ Orr: Financial system not been tested as severely as it could have been

RBNZ Governor Adrian Orr said the New Zealand economy has been “relatively resilient” to the economic shock from the pandemic so far. The financial system “as not been tested as severely as it could have been”. However, he warned, “businesses domestically and internationally face ongoing challenges as fiscal support measures unwind, which will lead to an increase in loan impairments for banks.”

On the topic of house prices, Deputy Governor Geoff Bascand said, “high leverage in the housing sector poses risks if house prices fall sharply or unemployment rises, reducing the ability to service loans”. Hence, RBNZ “intends to re-impose LVR restrictions to guard against continued growth in high-risk lending and ensure that banks remain resilient to a future housing market downturn.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1854; (P) 1.1874; (R1) 1.1912; More…..

EUR/USD’s breach of 1.1920 suggests that rebound from 1.1602 is resuming. Intraday bias is back on the upside for retesting 1.2011 high. Decisive break there will resume whole rally from 1.0635 low. On the downside, though, break of 1.1800 support will turn bias to the downside, to extend the consolidation pattern from 1.2011 with another falling leg.

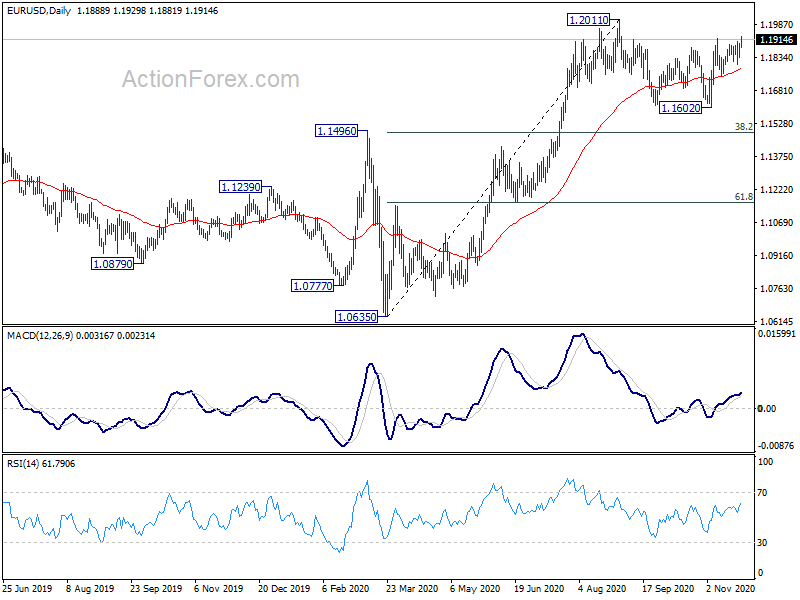

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1422 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | -0.60% | -0.60% | 1.30% | 1.40% |

| 00:30 | AUD | Construction Work Done Q3 | -2.60% | -2.00% | -0.70% | 0.50% |

| 09:00 | CHF | Credit Suisse Economic Expectations Nov | 30 | 2.3 | ||

| 13:30 | USD | GDP Annualized Q3 P | 33.10% | 33.10% | 33.10% | |

| 13:30 | USD | GDP Price Index Q3 P | 3.60% | -2.00% | 3.70% | |

| 13:30 | USD | Initial Jobless Claims (Nov 20) | 778K | 725K | 742K | 748K |

| 13:30 | USD | Wholesale Inventories Oct P | 0.90% | 0.40% | 0.40% | |

| 13:30 | USD | Durable Goods Orders Oct | 1.30% | 1.00% | 1.90% | |

| 13:30 | USD | Durable Goods Orders ex Transportation Oct | 1.30% | 0.40% | 0.90% | |

| 15:00 | USD | Personal Income M/M Oct | -0.70% | 0.10% | 0.90% | |

| 15:00 | USD | Personal Spending Oct | 0.50% | 0.40% | 1.40% | |

| 15:00 | USD | PCE Price Index M/M Oct | 0.00% | 0.20% | ||

| 15:00 | USD | PCE Price Index Y/Y Oct | 1.20% | 1.40% | ||

| 15:00 | USD | Core PCE Price Index M/M Oct | 0.00% | 0.00% | 0.20% | |

| 15:00 | USD | Core PCE Price Index Y/Y Oct | 1.40% | 1.40% | 1.50% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Nov F | 76.9 | 77 | 77 | |

| 15:00 | USD | New Home Sales Oct | 999K | 972K | 959K | 1002K |

| 15:30 | USD | Crude Oil Inventories | -0.8M | 0.1M | 0.8M | |

| 17:00 | USD | Natural Gas Storage | 33B | 31B | ||

| 19:00 | USD | FOMC Minutes |