{kind=link}

Yen and Dollar weaken generally in Asian session today as strong risk appetite continues. Notable rally is also seen in gold today, extending its near term rally. New Zealand Dollar is currently leading other commodity currencies higher. European majors are generally mixed. Focus would turn to the neverending Brexit negotiations, as EU chief negotiator Michel Barnier is back in London.

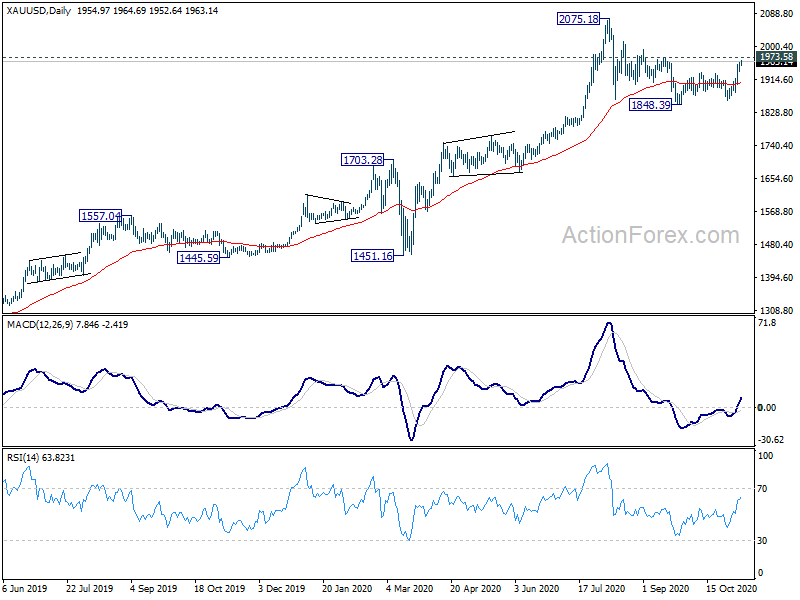

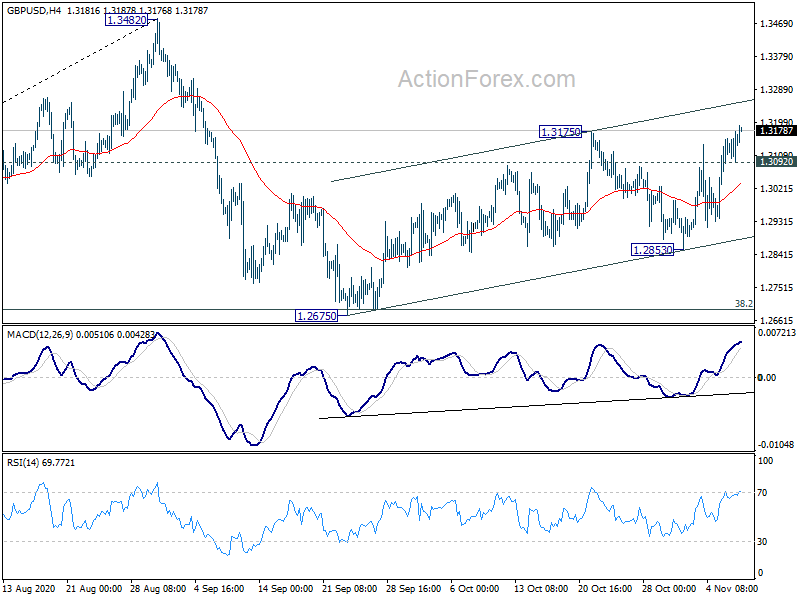

Technically, GBP/USD’s break of 1.3175 resistance is a progress in Dollar’s broad based down trend resumption. USD/CAD is set to take on 1.2994 support, and break will confirm down trend resumption. Gold is eyeing 1973.58 near term resistance now. Firm break there should pave the way to retest 2075.18 high.

In Asia, Nikkei is currently up 2.28%. Hong Kong HSI is up 1.62%. China Shanghai SSE is up 1.90%. Singapore Strait Times is up 1.14%. Japan 10-year JGB yield is up 0.0002 at 0.022.

BoJ members concerned with prolonged fight against coronavirus

In the Summary of Opinions at BoJ’s October 28/29 monetary policy meeting, it’s noted that “the fight against COVID-19 may be prolonged”. The central bank “should avoid brining a premature end to its current monetary policy responses”. BoJ should “exercise utmost vigilance against the possibility of a sudden change in financial markets and make policy responses flexibly when necessary”

Additionally, one member warned that “if economic recovery is delayed, credit risk might materialize, leading to a risk on the financial system side.” It’s “top priority” to ensure corporate financing and sustain employment”. Also, BoJ should “further look for ways to enhance the sustainability” of ETFs and J-REITs purchases.

“If COVID-19 spreads again and economic activity is pushed down, the CPI could stay in negative territory for a protracted period and deflation might take hold.”

Reuters Tankan manufacturing rose to -13, still well below pre-pandemic level

The Reuters Tankan sentiment index for Japanese manufacturers improved to -13 in November, up from October’s -16. That’ marked improvement over the cyclic low of -46 registered back in June. However, the index remained negative for the 16th straight months since August 2019. It’s also staying well below February’s pre-pandemic level at -5.

Non-manufacturing index was up slightly to -13, from October’s -16. Improvement over May’s low of -36 is less drastic. It’s, nonetheless, still the 9th straight month of negative reading since March.

Overall, the data suggested that the Japan economy is still struggling to shake off the drag from the pandemic crisis.

RBNZ to stand pat, relatively quiet week ahead

RBNZ is generally expected to keep interest rate unchanged at 0.25% this week. It’s still moving towards negative interest rate but that might happen early next year. BoJ will release summary of opinions and ECB will release monthly bulletin. UK data will catch a lot of attention with, employment and GDP featured. Eurozone will released Sentix investor confidence, GDP and German ZEW; US will release CPI and PPI. Overall, it’s more likely a quiet week in terms of economic events and central bank activities.

Here are some highlights of the week:

- Monday: BoJ summary of opinions; Swiss unemployment rate; Eurozone Sentix investor confidence.

- Tuesday: Japan current account; Eco watchers sentiment; China CPI, PPI; Australia NAB business confidence; UK BRC retail sales monitor, employment; Germany ZEW economic sentiment.

- Wednesday: RBNZ rate decision; Australia Westpac consumer sentiment; Japan machine tools orders.

- Thursday: Japan machine orders, PPI, tertiary industry index; Germany CPI final; Eurozone industrial production, ECB monthly bulletin; UK GDP, trade balance, productions; US CPI, jobless claims.

- Friday: New Zealand businessNZ manufacturing; Swiss PPI; Eurozone GDP, employment change, trade balance; US PPI, U of Michigan sentiment.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3102; (P) 1.3140; (R1) 1.3186; More…

GBP/USD’s break of 1.3175 resistance suggests resumption of rebound from 1.2675. Intraday bias is now on the upside. Break of near term channel resistance (now at 1.3252) will indicate upside acceleration and pave the way to retest 1.3482 high. On the downside, break of 1.3092 support will mix up the near term outlook and turn intraday bias neutral again.

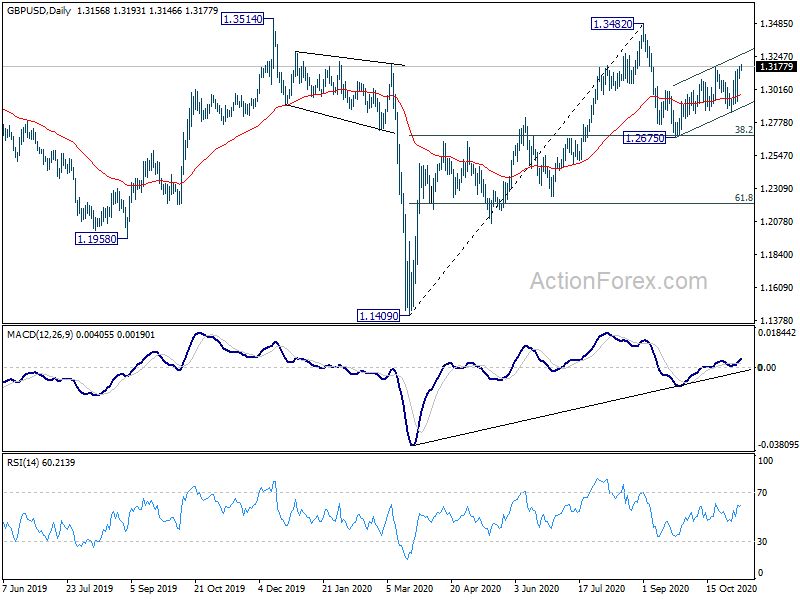

In the bigger picture, focus stays on 1.3514 key resistance. Decisive break there should also come with sustained trading above 55 month EMA (now at 1.3307). That should confirm medium term bottoming at 1.1409. Outlook will be turned bullish for 1.4376 resistance and above. Nevertheless, rejection by 1.3514 will maintain medium term bearishness for another lower below 1.1409 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 05:00 | JPY | Leading Economic Index Sep P | 92.9 | 88.4 | ||

| 06:45 | CHF | Unemployment Rate Oct | 3.40% | 3.30% | ||

| 07:00 | EUR | Germany Trade Balance Sep | 17.2B | 15.7B | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | -14.0 | -8.3 |