{kind=link}

Dollar trades generally soft in Asian session but losses are so far limited. The greenback is actually still staying above last week’s low against all but Yen and Kiwi. Major focus will turn to FOMC today and traders could finally commit to a direction, after getting Fed’s new economic projections. As for today, euro is currently the second weakest, followed by Swiss Franc. Kiwi and Aussie are the strongest ones.

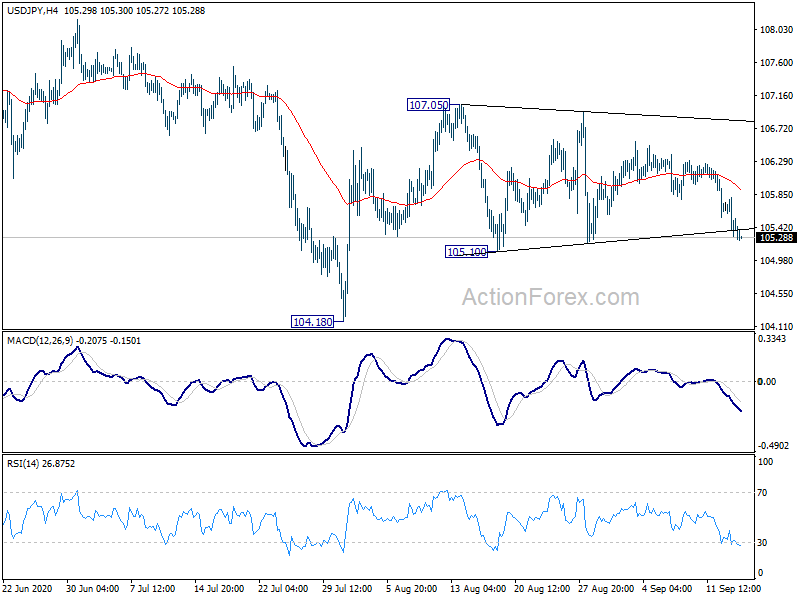

Technically, USD/JPY remains an interesting one to watch today. It’s now eyeing 105.10 support and break will trigger deeper fall to 104.18 low. It’s unsure whether such development would drag down the Dollar, or other Yen crosses more which lifts the greenback elsewhere. Key levels to watch will be 124.44 support in EUR/JPY and 135.53 fibonacci level in GBP/JPY. We might see Dollar strengthens if the breaks of the levels in EUR/JPY and GBP/JPY prompt downside accelerations.

In Asia, currently, Nikkei is up 0.16%. Hong Kong HSI is down -0.24%. China Shanghai SSE is down -0.24%. Singapore Strait Times is up 0.44%. Japan 10-year JGB yield is down -0.005 at 0.015. Overnight, DOW rose 0.01%. S&P 500 rose 0.52%. NASDAQ rose 1.21%. 10-year yield rose 0.008 to 0.679.

Japan exports had 8th straight month of double-digit decline in Aug

In non-seasonally adjusted term, Japan’s expected dropped -14.8% yoy to JPY 5232B in August. That’s the 8th straight month of double-digit decline, as well as the 21st month of contraction. It’s the worst run since the 23-month contraction through July 1987. Exports are generally expected to stay weak and might not reach pre-pandemic level until a least early 2022. Imports dropped -20.8% yoy to JPY 4984B. Trade surplus came in at JPY 248B.

In seasonally adjusted term, exports rose 5.9% mom to JPY 5580B. Imports rose 0.1% mom to JPY 5230B. Trade surplus widened to JPY 350B.

Australia Westpac leading index rose to -2.56, consistent with 4% growth in H2

Australia Westpac leading index rose to -2.56 in August, up from -4.42. Westpac said the improvement was broadly consistent with 1.8% growth in Q3, despite an expected -4% in the coronavirus center Victoria. That would also mean a “somewhat” moderated growth pace in Q4 at 2.2%. The combined second half growth would be 4%, more optimistic that RBA’s expectation of 1.3%.

Westpac also noted some market speculation surfaced after RBA minutes, for a rate cut from 0.25% to 0.1%. Such an option will “remain under considering but there appears to be no urgency”. RBA would indeed focus on supporting government bond markets first, including borrowing of state and territory governments.

US drops tariffs on Canadian aluminum, Canada drops retaliation threat

The US Trade Representative said it will drop the 10% tariffs on Canadian non-alloyed, unwrought aluminum, retroactive to September 1. The tariffs were reimposed in August due to a surge in import earlier this year. But USTR expects the volume to normalize back to 70k to 83k tons a month for the rest of the year, after consultation with Canada.

Canadian also dropped the threat to retaliate after the US move. Trade Minister Mary Ng emphasized “Canada has not conceded anything. We fully retain our right to impose our countermeasures if the U.S. administration decides to reimpose its tariffs on Canadian aluminum products, and we are prepared to do so.” Deputy Prime Minister Chrystia Freeland also insisted: “This is not a negotiated deal … we have not negotiated an agreement with the United States on quotas”.

Separately, USTR blasted WTO’s ruling against US tariffs on Chinese goods. Robert Lighthizer criticized in a statement the WTO “provides no remedy” for China’s “harmful technology practices.” ‘”The United States must be allowed to defend itself against unfair trade practices, and the Trump Administration will not let China use the WTO to take advantage of American workers, businesses, farmers, and ranchers,” he added.

Dollar index struggles to find upside momentum as focus turns to FOMC

Fed will have the first monetary policy decision after adopting “average inflation targeting”. No policy change is expected. Instead, first focus will be on the tweak in the accompanying statement. The statement should reflect that it seeks to seeking to achieve inflation that averages 2% over time. That is, as Chair Jerome Powell said before, “following periods when inflation has been running below 2%, appropriate monetary policy will likely aim to achieve inflation moderately above 2% for some time”. Secondly, new economic projections should reveal Fed’s view on the outlook of both the economy and the policy rate.

Some suggested readings on Fed:

- FOMC Preview – Policy Incorporating Average Inflation Targeting. New Economic Forecasts and Dot Plots Awaited

- Fed Meeting: Justifying the Paradigm Shift

- FOMC Preview

- Fed Monitor: Forward Guidance Linked To Inflation Outcomes And Faster QE Buying On The Cards

- Powell Announced Dovish Shift to Fed’s Monetary Policy, Targeting Averaging Inflation and shortfall of Maximum Employment

- Powell Announces Changes to Monetary Policy Framework

- Fed’s Average Inflation Target Means Low Rates for Longer

Dollar index’s rebound from 91.74 remains unconvincing so far, lacking follow through momentum. the conditions for a rebound are still there, as fall from 102.99 has likely completed with five waves down to 91.74, on bullish convergence condition in daily MACD. Break of 93.66 resistance (with corresponding break of 1.1754 support in EUR/USD), should push DXY through 55 day EMA to 38.2% retracement of 102.99 to 91.74 at 96.03.

Elsewhere

UK will release CPI, PPI today. Eurozone will release trade balance. Canada will also release CPI. From US, in addition to FOMC, retail sales, business inventories, NAHB housing market index and oil inventories will be featured.

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.23; (P) 105.52; (R1) 105.75; More...

Intraday bias in USD/JPY remains neutral first with focus now on 105.10 support. Break will turn bias to the downside for retesting 104.18. Further break there will resume whole decline from 111.71. On the upside, break of 107.05 will revive the case that pull back from 111.71 has completed with three waves down to 104.18. Intraday bias will be turned to the upside for 109.85 resistance.

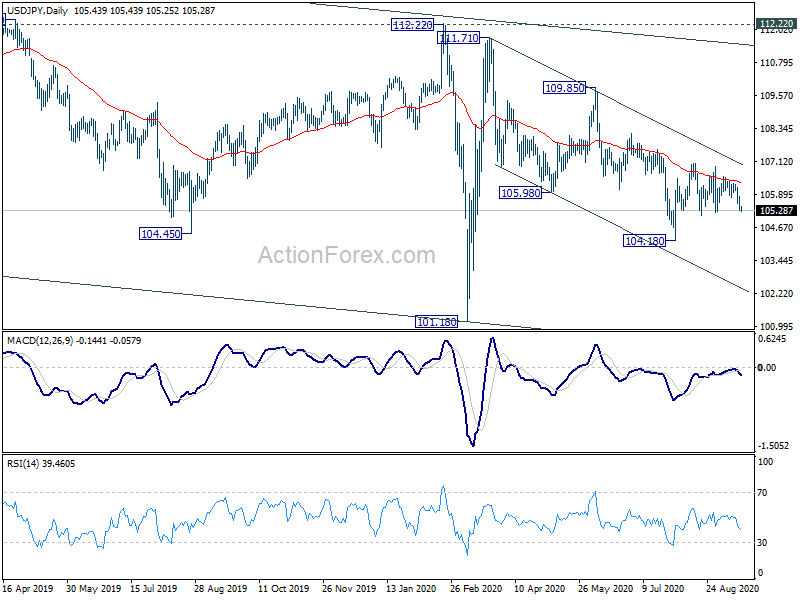

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016). Hence, there is no clear indication of trend reversal yet. The down trend could still extend through 101.18 low. However, sustained break of 112.22 should confirm completion of the down trend and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q2 | 1.83B | 0.69B | 1.56B | 1.90B |

| 23:50 | JPY | Trade Balance (JPY) Aug | 0.35T | -0.03T | 0.04T | |

| 00:30 | AUD | Westpac Leading Index M/M Aug | 0.50% | 0.10% | ||

| 06:00 | GBP | CPI M/M Aug | 0.40% | 0.40% | ||

| 06:00 | GBP | CPI Y/Y Aug | 0.10% | 1.00% | ||

| 06:00 | GBP | Core CPI Y/Y Aug | 0.70% | 1.80% | ||

| 06:00 | GBP | RPI M/M Aug | 0.70% | 0.50% | ||

| 06:00 | GBP | RPI Y/Y Aug | 2.20% | 1.60% | ||

| 06:00 | GBP | PPI Input M/M Aug | 1.30% | 1.80% | ||

| 06:00 | GBP | PPI Input Y/Y Aug | -4.30% | -5.70% | ||

| 06:00 | GBP | PPI Output M/M Aug | -0.10% | 0.30% | ||

| 06:00 | GBP | PPI Output Y/Y Aug | -1.00% | -0.90% | ||

| 06:00 | GBP | PPI Core Output M/M Aug | 0.00% | -0.10% | ||

| 06:00 | GBP | PPI Core Output Y/Y Aug | -0.20% | 0.10% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jul | 17.3B | 17.1B | ||

| 12:30 | USD | Retail Sales M/M Aug | 1.10% | 1.20% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Aug | 1.10% | 1.90% | ||

| 12:30 | CAD | Foreign Securities Purchases (CAD) Jul | -13.52B | |||

| 12:30 | CAD | CPI M/M Aug | 0.40% | 0.00% | ||

| 12:30 | CAD | CPI Y/Y Aug | 0.50% | 0.10% | ||

| 12:30 | CAD | CPI Common Y/Y Aug | 1.30% | |||

| 12:30 | CAD | CPI Median Y/Y Aug | 1.90% | |||

| 12:30 | CAD | CPI Trimmed Y/Y Aug | 1.70% | |||

| 14:00 | USD | Business Inventories Jul | 0.20% | -1.10% | ||

| 14:00 | USD | NAHB Housing Market Index Sep | 78 | 78 | ||

| 14:30 | USD | Crude Oil Inventories | 2.0M | |||

| 18:00 | USD | Fed Interest Rate Decision | 0.25% | |||

| 18:30 | USD | FOMC Press Conference |