{kind=link}

Dollar trades broadly lower today but there seems to be no clear unified theme in the financial markets. Stocks are in risk-on mode, lifting the Australian Dollar. But Yen is also generally higher despite some mild recovery in treasury yields. Sterling’s recovery is understandable as it’s digesting some of last week’s steep losses. Brexit uncertainty will cap the Pound’s recovery. the markets could probably continue to trade on their own until Fed’s announcement tomorrow.

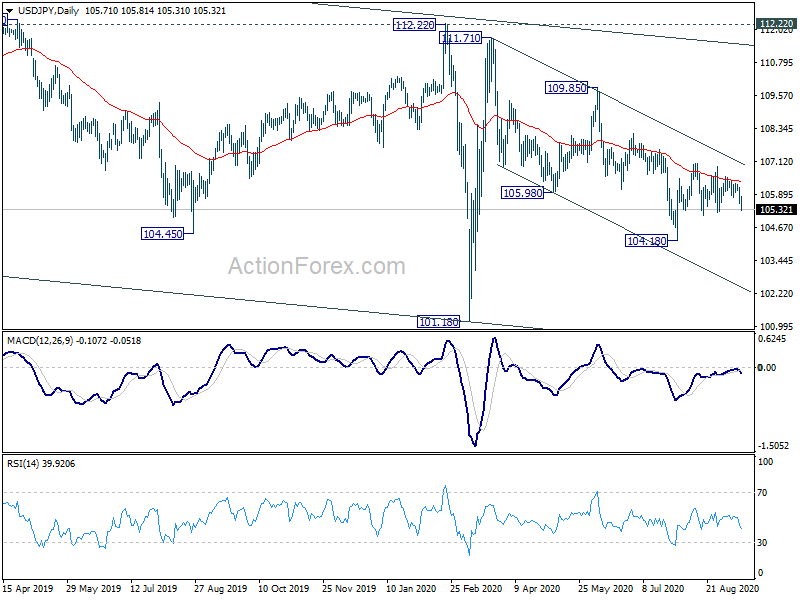

Technically, USD/JPY could finally really have a breakout, to the downside. Break of 105.10 support will bring deeper decline to 104.18. Break there will resume larger down trend from 111.71. At the same time, EUR/JPY could be heading back to 124.44 support and bring will confirm the start of short term correction. GBP/JPY could also be extending fall from 142.71 towards 131.11 fibonacci level.

In Europe, currently, FTSE is up 1.28%. DAX is up 0.45%. CAC is up 0.60%. German 10-year yield is up 0.0018 at -0.475. Earlier in Asia, Nikkei dropped -0.44%. Hong Kong HSI rose 0.38%. China Shanghai SSE rose 0.51%. Singapore Strait Times roes 0.13%. Japan 10-year JGB yield rose 0.0007 to 0.020.

US Empire State manufacturing rose to17, hours worked surged

US Empire State Manufacturing index rose to 17.0 in September, up from 3.7, beat expectation of 6.2. Looking at some details, new orders rose 8.8 pts to 7.1. Shipments rose 7.4 pts to 14.1. Price paid rose 9.2 pts to 25.2. Prices received rose 1.8 pts to 4.7. Number of employees rose 0.2 pts to 2.6. Average employee workweek jumped sharply by 13.5pts to 6.7. The workweek number was also the first positive reading since the pandemic began. Future business conditions also rose 6 pts to 40.3, suggesting some optimism ahead.

Also released, US import price rose 0.9% mom in August, above expectation of 0.5% mom. Industrial production rose 0.4% mom, below expectation of 0.8% mom. Canada manufacturing sales rose 7.0% mom in July, below expectation of 8.8% mom.

German ZEW rose to 77.4, noticeable recovery expected despite Brexit and coronavirus

Germany ZEW Economic Sentiment rose to 77.4 in September, up from 71.5, beat expectation of 70.0. Current Situation rose 15.1 pts to -66.2. Eurozone ZEW Economic Sentiment rose 9.9 pts to 73.9, Current Situation rose 8.9 pts to -80.9.

“The ZEW Indicator of Economic Sentiment has increased again, signalling that the experts continue to expect a noticeable recovery of the German economy. Stalled Brexit talks and rising COVID-19 cases could not dampen the positive mood. However, the still negative outlook for the banking sector reveals fears of a rising number of loan defaults in the coming six months,” comments ZEW President Professor Achim Wambach.

UK unemployment rate rose to 4.1%, claimant count rose 73.7k

UK unemployment rate rose to 4.1% in the three month to July, up from 3.9%, matched expectations. Unemployment rate for rose to 4.3% and that for women rose to 3.8%. Average earnings including bonus dropped -1.0% 3moy, above expectation of -1.1% 3moy. Average earnings excluding bonus rose 0.2% 3moy, better than expectation of -0.6% 3moy.

Claimant count rose 73.7k or 2.8% mom to 2.7. Since March this year, Claimant count has increased by 120.8% or 1.5m.

RBA will continue to consider how further monetary measures could support recovery

In the minutes of September meeting, RBA said the board agreed to “maintain highly accommodative settings as long as required”. A surprised addition in the language is that the central bank will “continue to consider how further monetary measures could support the recovery”. While it’s still early, the minutes indicated that RBA would be ready to ease further if circumstances warrant so.

Other than that, the minutes continued little new. The pandemic economic downturn “had not been as severe as earlier expected”/. Recovery, however, was “likely to be uneven”, with the outbreak in Victoria having a major effect. Uncertainty was “continuing to affect the spending plans of many households and businesses”. Wage and price pressures “remained subdued” and this was “likely to continue for some time”.

Also from Australia, house price index dropped -1.8% qoq in Q2, worse than expectation of -1.3% qoq.

More on RBA

- AUD Strengthened on Upbeat Chinese Data, RBA Minutes Contained Little News

- RBA Minutes – Strong Support for the States

China data beat expectations, USD/CNH breaks key fibonacci support

August economic data released from China today were generally better than expected. Industrial production continued its bounce and rose 5.6% yoy versus expectation of 5.1% yoy. That’s also the fastest rise in eight months. Retail sales rose 0.5% yoy versus expectation of 0.0% yoy. Sales were finally growth after a seven-month downturn. Fixed asset investment dropped -0.3% ytd yoy, above expectation of -0.5% ytd yoy.

More on China:

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.46; (P) 105.82; (R1) 106.08; More...

USD/JPY drops sharply today but stays in range of 105.10/107.05. Intraday bias remains neutral first. On the downside, break of 105.10 will bring retest of 104.18 low first. Break there will resume whole decline from 111.71. On the upside, break of 107.05 will revive the case that pull back from 111.71 has completed with three waves down to 104.18. Intraday bias will be turned to the upside for 109.85 resistance.

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016). Hence, there is no clear indication of trend reversal yet. The down trend could still extend through 101.18 low. However, sustained break of 112.22 should confirm completion of the down trend and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | NZD | Westpac Consumer Survey Q3 | 95.1 | 97.2 | ||

| 01:30 | AUD | House Price Index Q/Q Q2 | -1.80% | -1.30% | 1.60% | |

| 01:30 | AUD | RBA Minutes | ||||

| 02:00 | CNY | Retail Sales Y/Y Aug | 0.50% | 0.00% | -1.10% | |

| 02:00 | CNY | Industrial Production Y/Y Aug | 5.60% | 5.10% | 4.80% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Aug | -0.30% | -0.50% | -1.60% | |

| 06:00 | GBP | Claimant Count Change Aug | 73.7K | 94.4K | 69.69K | |

| 06:00 | GBP | Claimant Count Rate Aug | 7.60% | -2.20% | 7.50% | |

| 06:00 | GBP | ILO Unemployment Rate 3M Jul | 4.10% | 4.10% | 3.90% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jul | -1.00% | -1.10% | -1.20% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jul | 0.20% | -0.60% | -0.20% | |

| 06:30 | CHF | Producer and Import Prices M/M Aug | -0.40% | -0.20% | 0.10% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Aug | -3.50% | -2.40% | -3.30% | |

| 06:45 | EUR | France CPI M/M Aug F | -0.10% | -0.10% | -0.10% | |

| 06:45 | EUR | France CP Y/Y Aug F | 0.20% | 0.20% | 0.20% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | 77.4 | 70 | 71.5 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Sep | 73.9 | 62.8 | 64 | |

| 12:30 | CAD | Manufacturing Sales M/M Jul | 7.00% | 8.80% | 20.70% | 23.00% |

| 12:30 | USD | Empire State Manufacturing Index Sep | 17 | 6.2 | 3.7 | |

| 12:30 | USD | Import Price Index M/M Aug | 0.90% | 0.50% | 0.70% | 1.20% |

| 13:15 | USD | Industrial Production M/M Aug | 0.40% | 0.80% | 3.00% | |

| 13:15 | USD | Capacity Utilization Aug | 71.40% | 71.20% | 70.60% |