{kind=link}

Dollar stays firm as recovery continues while Yen is following as the second strongest. While US stocks continued their record run overnight, Asian markets are generally in red outside of Japan. As for today, Euro is currently the worst performing, followed by Sterling, and then Australian Dollar. Focuses will turn to ISM non-manufacturing from US today, and more importantly, non-farm payrolls tomorrow.

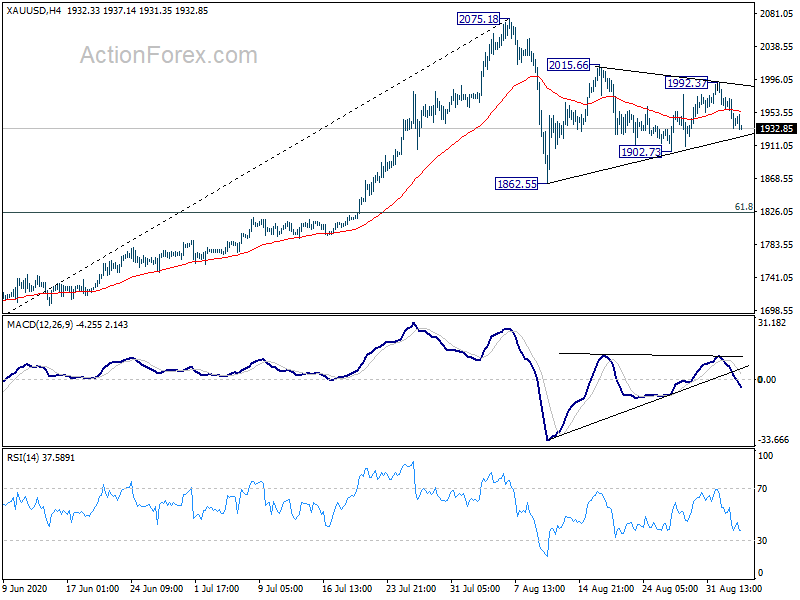

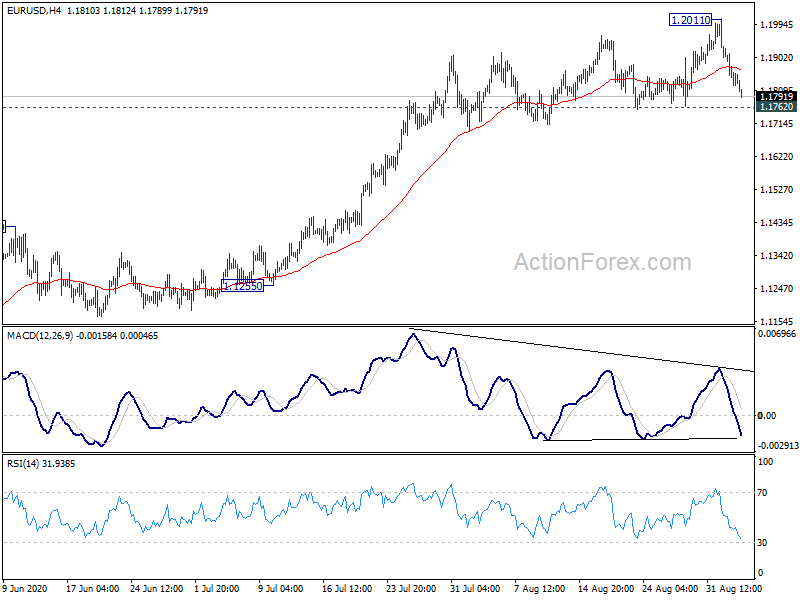

Technically, Gold’s break of 4 hour 55 EMA suggests that the recovery from 1902.73 has completed. Consolidation from 2075.18 is extending with another falling leg to 1902.73 support, and likely below. Such development would be supportive to the greenback. Still, we’d prefer to see, at least, solid break of 1.1762 support in EUR/USD, as well as 0.9161 resistance in USD/CHF to confirm that a genuine rebound in the greenback is underway.

In Asia, Nikkei closed up 0.94%. Hong Kong HSI is down -0.57%. China Shanghai SSE is down -0.67%. Singapore Strait Times is down -0.63%. Japan 10-year JGB yield is down -0.0084 at 0.037. Overnight, DOW rose 454.84 pts or 1.59% to 29100.50. 29568.57 record high is now within reach. S&P 500 rose 1.54% to 3580.84, record. NASDAQ rose 0.98% to 12056.44, also record. 10-year yield dropped -0.021 to 0.651.

Fed Williams: New Framework addresses problems of low neutral rate and persistently low inflation

New York Fed President John Williams said in a speech, Fed’s new framework statement “directly and effectively addresses the problems caused by a low neutral rate and persistently low inflation.”

“First, it stipulates that, following periods when inflation has been running persistently below 2 percent, a temporary overshooting of the longer-run inflation target will likely be desirable to keep inflation and inflation expectations centered on 2 percent.

“Second, it makes clear that we seek inflation that averages 2 percent over time, consistent with our longer-run target.

“Finally, the statement makes unequivocally clear that we seek maximum employment and will aim to eliminate shortfalls from this broad and inclusive goal. These changes are mutually reinforcing and will meaningfully improve our ability to achieve both of our dual mandate goals in an environment of a very low neutral rate.”

Fed Mester: Strong employment is not a concern in absence of inflationary pressures

Cleveland Fed Bank President Loretta Mester said in a speech, Fed’s new strategy statement “is now more explicit about how we will go about achieving” the inflation goal. “The new language is a stronger statement than we have made in the past”, she added.

“We are now clear that after inflation has been running persistently below 2 percent, not only will we tolerate serendipitous shocks that move inflation above 2 percent, but that we will likely set policy with the intention to move inflation moderately above 2 percent for some time.”

Also, “the new statement language clarifies that in the absence of inflationary pressures or risks to financial stability, strong employment is not a concern and monetary policy will not react to it”.

BoE Vlieghe: Easing lockdown insufficient to bring back economic activity

BoE MPC member Gertjan Vlieghe said in the annual report to Treasury Select Committee of Parliament, from different pandemic experiences, it’s “not just the economic lockdown that suppresses economic activity”. There’s also a “large behavioural response of households and firms to the prevalence of the virus, which suppresses demand for certain types of economic activity even without any lockdown measures in place.” Thus, “easing lockdown measures is not sufficient to bring back economic activity.”

He also warned, “the longer the virus remains prevalent enough to affect patterns of consumption, investment and employment, the higher the likelihood that some sectors will not be able to return to their previous level of activity”. That would “imply that demand in other sectors needs to rise sufficiently to use up the resulting spare capacity in the labour force and in other inputs”. Such “reorientation of the economy towards a difference sectorial composition” is likely to be a slow process.

“Based on these considerations, there is a material risk in my view that it could take several years for the economy to return to full capacity and inflation to return sustainably to target, even with monetary policy at its current settings.”

Bundesbank Weidmann: Monetary and fiscal stimulus must be scaled back after crisis

Bundesbank President Jens Weidmann urged that after the pandemic crisis, “the emergency monetary-policy measures must be scaled back again”. Further, “if the price outlook so requires, then monetary policy as a whole must be normalized” as risks and side effects “can increase over time.”

Also, “fiscal policy should also not get used to an easy course, nor should it rely on interest rates to remain so low over the long term.” “The state has to be careful not to interfere too much in corporate decisions, for example in the case of new investments,” Weidmann said. “The state is not the better entrepreneur.”

BoJ Kataoka: Stronger easing actions to show our determination and credibility

BoJ board member Goushi Kataoka, a known dove, urged strong easing actions “to show our determination we won’t tolerate deflation, we can improve the credibility of our price target.”

“The job market is worsening due to the pandemic, which will drag on consumption,” he added. “If the pandemic’s impact is prolonged and hurts companies’ medium- to long-term growth expectations, they may be forced to slash future demand projections and adjust capital spending plans.”

Australia trade surplus shrank to 4.6B in Jul as exports fell

Australia export of goods and services dropped -4% mom to AUD 34.5B in July. Imports rose 7% mom to AUD 29.9B. Trade surplus shrank to AUD 4.6B, down from AUD 8.2B, missed expectation of AUD 5.0B.

AiG Performance of Construction index dropped -4.8 pts to 37.9 in August. Ai Group Head of Policy, Peter Burn, said: “The sharp fall in activity in Victoria was a major factor in the downturn while border restrictions in other states have hampered builders and constructors who are reliant on interstate supplies and the availability of tradies from across borders.”

China PMI services ticked down to 54.0, but employment grew again

China Caixin PMI Services dropped slightly by -0.1 to 54.0 in August, matched expectations. Markit said new order growth eased further but remained strong. Staff numbers expanded for the first time since January. Output prices rose amid further increase in operating costs. PMI Composite rose to 55.1, up from July’s 54.5.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, the recovery of the manufacturing and services sectors from the epidemic remained the main theme of the economy. Supply and demand both expanded. The gauges for orders, purchases and inventories all remained strong. Price measures remained stable. Over the past half year, external demand and employment remained subdued generally, but in August, employment for the services sector started to improve and employment for the manufacturing sector approached a turning point.

” However, there were still uncertainties from Covid-19 overseas, which could constrain the “dual circulation” of domestic and international markets. Improvement in employment in the post-epidemic era requires longer-term market recovery and longer-term stability of business expectations. During this process, support from relevant macroeconomic policies is essential.”

Looking ahead

Eurozone and UK services PMI final will be released in European session. European will also release retail sales. Later in the day, US ISM services will take center stage, while trade balance and jobless claims will be featured. Canada will also release trade balance.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1808; (P) 1.1869; (R1) 1.1915; More…..

Intraday bias in EUR/USD stays neutral first with focus on 1.1762 support. As long as this support holds, another rise is still in favor and break of 1.2011 will will resume the whole rise from 1.0635. However, firm break of 1.1762 will confirm short term topping and turn bias to the downside for deeper pull back, to 55 day EMA (now at 1.1630) and below.

In the bigger picture, down trend from 1.2555 (2018 high) has completed at 1.0635 already. Rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally rise should be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516 ). This will remain the favored case as long as 1.1422 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index Aug | 37.9 | 42.7 | ||

| 01:00 | NZD | ANZ Commodity Price Aug | -0.90% | 2.30% | 2.90% | |

| 01:30 | AUD | Trade Balance (AUD) Jul | 4.61B | 5.00B | 8.20B | 8.15B |

| 01:45 | CNY | Caixin Services PMI Aug | 54.0 | 54.0 | 54.1 | |

| 06:30 | CHF | CPI M/M Aug | 0.00% | -0.40% | -0.20% | |

| 06:30 | CHF | CPI Y/Y Aug | -0.90% | -1.10% | -0.90% | |

| 07:45 | EUR | Itay Services PMI Aug | 64.7 | 51.6 | ||

| 07:50 | EUR | France Services PMI Aug F | 51.9 | 51.9 | ||

| 07:55 | EUR | Germany Services PMI Aug F | 50.8 | 50.8 | ||

| 08:00 | EUR | Eurozone Services PMI Aug F | 50.1 | 50.1 | ||

| 08:30 | GBP | Services PMI Aug | 60.1 | 60.1 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Jul | 1.30% | 5.70% | ||

| 11:30 | USD | Challenger Job Cuts Aug | 262.649K | |||

| 12:30 | CAD | International Merchandise Trade (CAD) Jul | -3.2B | |||

| 12:30 | USD | Initial Jobless Claims (Aug 28) | 965K | 1006K | ||

| 12:30 | USD | Trade Balance (USD) Jul | -52.2B | -50.7B | ||

| 13:45 | USD | Services PMI Aug F | 54.8 | 54.8 | ||

| 14:00 | USD | ISM Services PMI Aug | 57.1 | 58.1 | ||

| 14:30 | USD | Natural Gas Storage | 37B | 45B |