{kind=link}

Dollar appears to have finally taken a side, the downside, with Fed chair Jerome Powell’s Jackson Hole speech. In short, Fed is now adopting a “flexible form of average inflation targeting”, to achieve inflation that “averages 2 percent over time”. Therefore, following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time. Markets see that Fed would keep monetary policy loose for longer, to allow inflation to overshoot 2%.

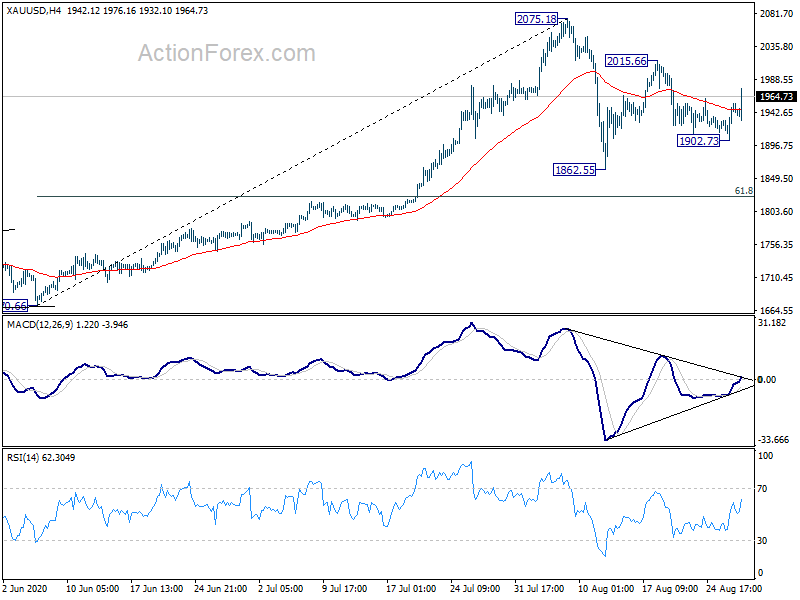

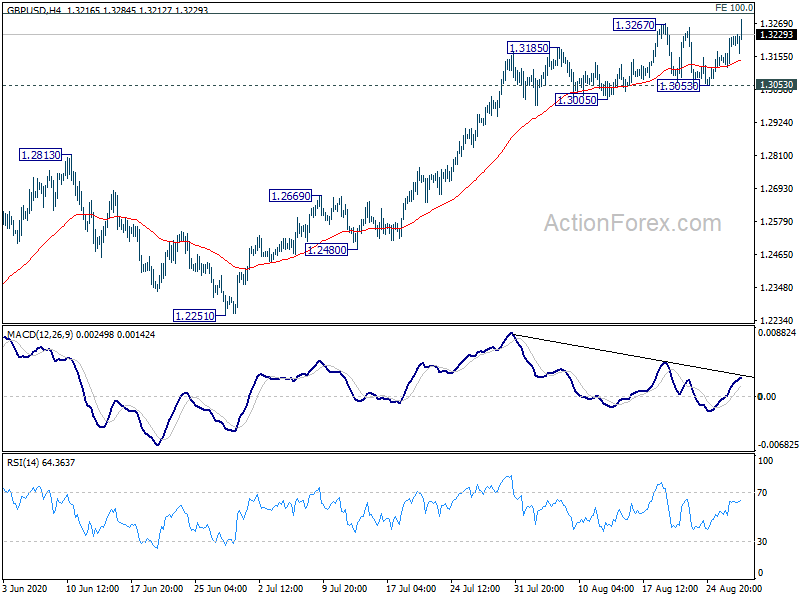

Technically, GBP/USD and AUD/USD have both taken out recent resistance at 1.3267 and 0.7275 respectively, indicating rally resumption. USD/CAD has also dropped through 1.3133 temporary low finally to resume recent fall. Focus is now on whether the relatively weak Euro would take out 1.1965 resistance to align itself with others. At the same time, Gold’s strong rally and firm break of 4 hour 55 EMA suggests completion of the fall from 2015.66. It’s possible that consolidation from 2075.18 has completed. But in any case, further rise is now in favor to 2015.66 resistance first. Break will solidify the bullish case.

In other markets, DOW opens higher up more than 100 pts. In Europe, currently, FTSE is up 0.06%. DAX is down -0.12%. CAC is down -0.09%. German 10-year yield is down -0.041 at -0.455. Earlier in Asia, Nikkei dropped -0.35%. Hong Kong HSI dropped -0.83%. China Shanghai SSE rose 0.61%. Singapore Strait Times dropped -0.88%. Japan 10-year JGB yield dropped -0.0006 to 0.044.

Dollar dives as Fed adopts flexible form of average inflation targeting

Fed Chair Jerome Powell indicates in the Jackson Hole speech that the central bank is adopting a “flexible form of average inflation targeting”. That is, Fed would target to achieve inflation that “averages 2 percent over time”. Therefore, following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.

US initial jobless claims dropped slightly to 1006k

US initial jobless claims dropped slightly by 98k to 1006k in the week ending August 22. Four-week moving average of initial claims dropped 107k to 1068k. Continuing claims dropped -223k to 14535k in the week ending August 15. Four-week moving average of continuing claims dropped -604k to 15216k.

Q2 GDP contraction was revised to -31.7% annualized, comparing to advance estimate of -32.9%. With the second estimate, private inventory investment and personal consumption expenditures (PCE) decreased less than previously estimated.

Swiss GDP contracted -8.2% in Q2, relatively limited in international comparison

Swiss GDP contracted -8.2% qoq in Q2, slightly better than expectation of -8.7% qoq. That’s the biggest decline since records of quarterly data began in 1980. Comparing to Q4 2019, before the pandemic, GDP slumped by a total of -10.5% in H1 2020. SEO said, “domestic economic activity was severely restricted in the wake of the pandemic and the measures taken to contain it”. But Swiss GDP decline remains “limited” in an international comparison.

From Eurozone M3 money supply rose 10.2% yoy in July, above expectation of 9.2% yoy.

Japan government said exports are picking up

In the Japan Cabinet Office’s monthly report, assessment on exports were revised up to “show movements of picking up”, instead of “bottoming out”. Views on overall economy is unchanged as it is “showing movements of picking up”, together with private consumption. Meanwhile, business investments remained “in a weak tone”.

The government also dropped the reference that industrial production is “decreasing as a whole” and only noted some pick up in some sectors. Employment is “showing weakness” and ” consumer prices are flat, both unchanged.

From Japan, all industry activity index rose 6.1% mom in June, below expectation of 6.3% mom.

BoJ Suzuki: Monetary easing will last even longer due to pandemic

BoJ board member Hitoshi Suzuki said “with the economy having lost momentum to achieve our price target due to the pandemic, our monetary easing will last even longer”

He noted that the benefits of the central bank’s ultra-easing monetary policy still outweighs the costs. however, “If a second and third wave of infection hits Japan, financial institutions’ credit costs could balloon to levels near those hit after collapse of Lehman Brothers” during the 2008/09 global financial crisis.

Australia capital expenditure dropped -5.9% in Q2, less severe than expected

Australia total new capital expenditure dropped -5.9% qoq in Q2 to AUD 26.13B, better than expectation of -8.2% qoq. But it’s still down -11.5% yoy comparing to Q2 2019. Building and structures expenditures dropped -4.4% to AUD 14.01B. Equipment, plant and machinery expenditure dropped -7.6% qoq to AUD 12.1B.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3146; (P) 1.3182; (R1) 1.3248; More….

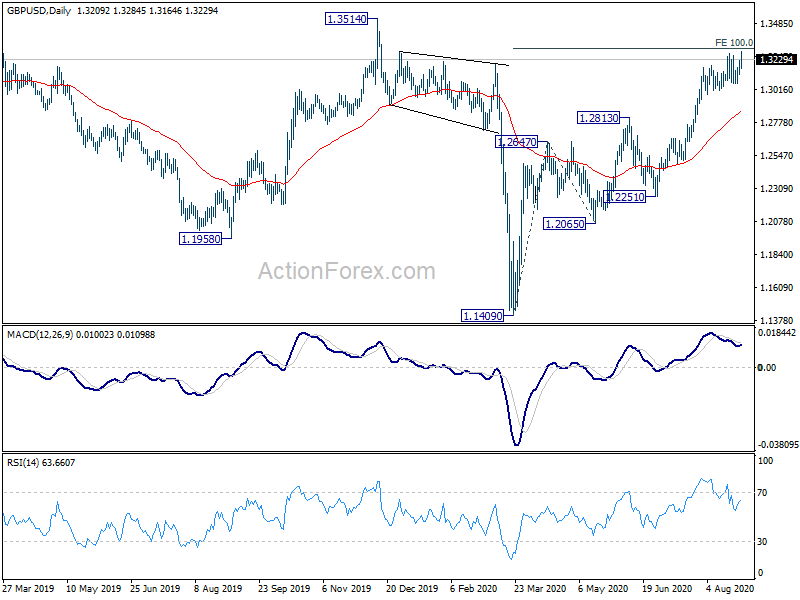

GBP/USD’s break of 1.3267 resistance suggests resumption of recent rise from 1.1409. Intraday bias is back on the upside with focus on 100% projection of 1.1409 to 1.2647 from 1.2065 at 1.3303. Sustained break there will pave the way to 1.3514 structural resistance next. On the downside, break of 1.3053 support will now indicate short term topping. Intraday bias will be turned back to the downside for 55 day EMA (now at 1.2864).

In the bigger picture, while the rebound from 1.1409 is strong, there is not enough evidence for trend reversal yet. Down trend from 2.1161 (2007 high) should still resume sooner or later. However, decisive break of 1.3514 should at least confirm medium term bottoming and turn outlook bullish for 1.4376 resistance first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Private Capital Expenditure Q2 | -5.90% | -8.20% | -1.60% | -2.10% |

| 04:30 | JPY | All Industry Activity Index M/M Jun | 6.10% | 6.30% | -3.50% | |

| 05:45 | CHF | GDP Q/Q Q2 | -8.20% | -8.70% | -2.60% | -2.50% |

| 08:00 | EUR | Eurozone Private Loans Y/Y Jul | 3.00% | 3.00% | 3.00% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | 10.20% | 9.20% | 9.20% | |

| 12:30 | CAD | Current Account (CAD) Q2 | -8.6B | -11.8B | -11.1B | |

| 12:30 | USD | Initial Jobless Claims (Aug 21) | 1006K | 925K | 1106K | 1104K |

| 12:30 | USD | GDP Annualized Q2 P | -31.70% | -32.50% | -32.90% | |

| 12:30 | USD | GDP Price Index Q2 P | -2.00% | -1.80% | -1.80% | |

| 14:00 | USD | Pending Home Sales M/M Jul | 5.50% | 16.60% | ||

| 14:30 | USD | Natural Gas Storage | 39B | 43B |