{kind=link}

The forex markets continue to stay in rather tight range today, shrugging off strong movements in the stock markets. Yen is generally soft but there is no sign of breakout yet. Similarly, Dollar is also struggling to find a clear direction, staying as the second weakest for the week next to Yen. Australian Dollar is currently the firmer one, together with Sterling. The markets might need to have some real inspirations from Fed Chair Jerome Powell later in the week to make the next move.

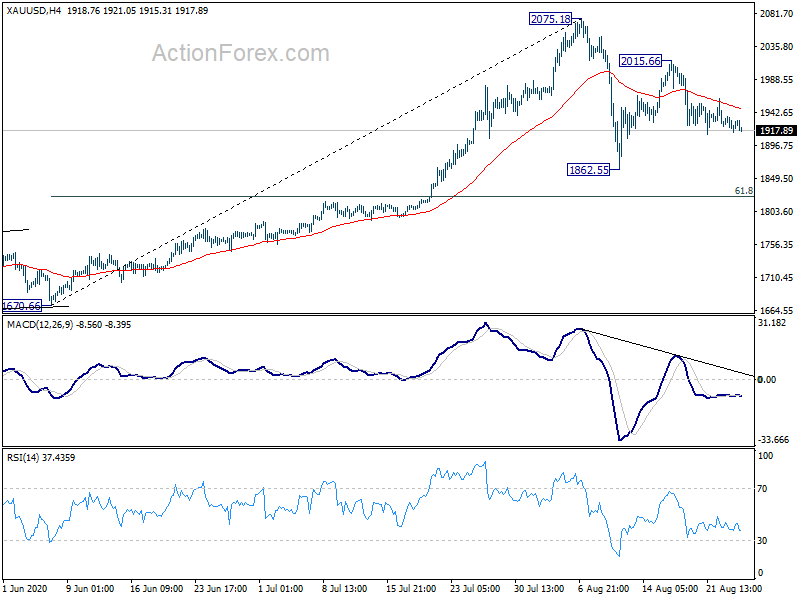

Technically, Gold and Crude oil might be the focuses for today. Gold was rejected by 4 hour 55 EMA earlier, affirming near term downside bias. Break of 1911.43 will resume the fall from 2015.66, as the third leg of the consolidation pattern from 2075.18, to 1862.55.

WTI is now eyeing 43.38 resistance ahead of oil inventories report. Break there will resume larger rebound and could prompt downside breakout in USD/CAD through 1.3133 temporary low.

In Asia, Nikkei closed down -0.03%. Hong Kong HSI is down -0.12%. China Shanghai SSE is down -1.38%. Singapore Strait Times is down -0.80%. Japan 10-year JGB yield is up 0.0102 at -0.414. Overnight, DOW dropped -0.21%. But S&P 500 rose 0.36% to new record of 3443.62. NASDAQ rose 0.76% to new record of 11466.47. 10-year yield rose 0.036 to 0.682, after hitting 0.716.

Former BoJ Kiuchi: Core inflation to be slightly negative for three years, but BoJ actions unlikely

Former BoJ policy maker Takahide Kiuchi said the central bank is unlikely to ease further due to risks of banking-sector problems. He said, “Japan will likely see more small and midsized firms go under as the pandemic’s pain deepens, which could boost credit costs for lenders through next year… The pandemic has forced the BOJ to be more mindful of the risk of banking-sector problems, which means it can’t cut interest rates easily,”

Kiuchi expected GDP to take around give years to return to pre-pandemic levels. Also, core consumer inflation will hove in “slightly negative territory for about three years”. Nevertheless, “the BOJ has already detached its policy from its 2% inflation target, which means it won’t take action to prop up prices.”

New Zealand imports plunged -18% yoy in Jul, NZD/USD hovers in range

New Zealand’s goods exports dropped -0.2% yoy or NZD 9.8m to NZD 4.9B in July. Goods imports dropped -18% yoy or NZD 1.0B to NZD 4.6B. Trade surplus came in at NZD 282m, down from June’s NZD 475m, slightly below expectation of NZD 285m. Imports from all major trading partners expect China were down. On the other hand, exports to China and Japan decreased, while exports to USA, EU and Australia rose.

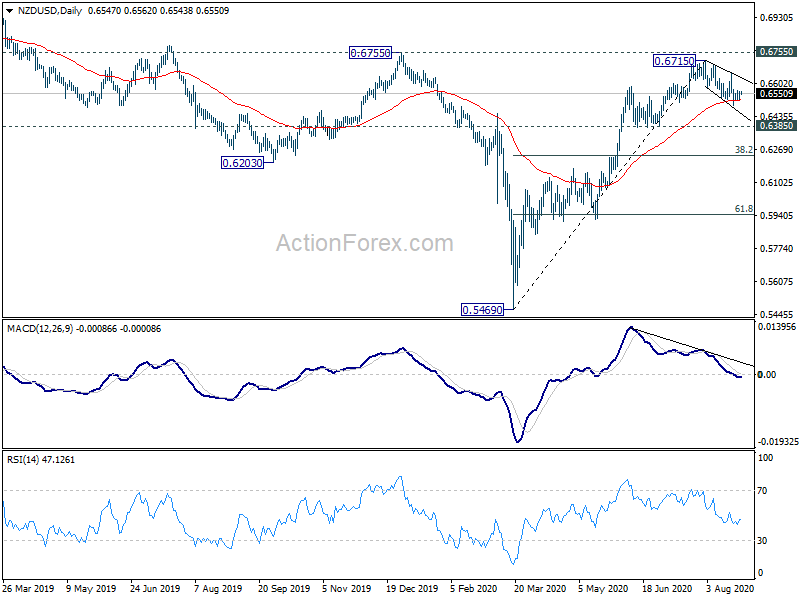

NZD/USD continues to hover slightly above 55 day EMA, drawing support from there. But at this point, correction from 0.6715 is still extended to extend lower. Firm break of the 55 day EMA would pave the way to 0.6385 support, and possibly to 38.2% retracement of 0.5469 to 0.6715 at 0.6239.

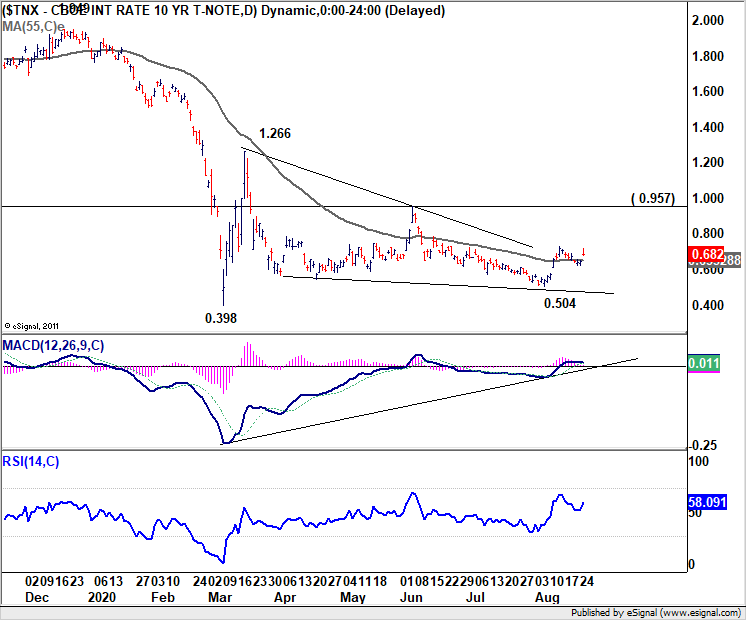

US 10-yr yield in another rally attempt after defending 55 day EMA

While S&P 500 and NASDAQ continued to make record highs overnight, it’s the development in treasury yields that’s worth more a mention. 10-year yield hit as high as 0.716, then pared back some gains to close at 0.682, up 0.036. It’s now trading above 0.71 handle in Asian session.

Unlike what happened after June’s spike, TNX is holding on to 55 day EMA this time, suggesting some resilience there. Focus is back on 0.727 resistance. Firm break there will firstly resume the rebound from 0.504. Secondly, that will suggest that the triangle pattern form 1.266 has completed. Stronger rise would then be seen back towards June’s high at 0.957. That could give Dollar a lift for the overdue corrective rebound. The next move would very much depends on Fed Chair Jerome Powell’s Jacksonhole speech.

Elsewhere

Australia construction work done dropped -0.7% in Q2, better than expectation of -5.8%. Japan corporate service price index rose 1.2% yoy in July, above expectation of 0.8% yoy. US durable goods orders and crude oil inventories will be the main focus for today.

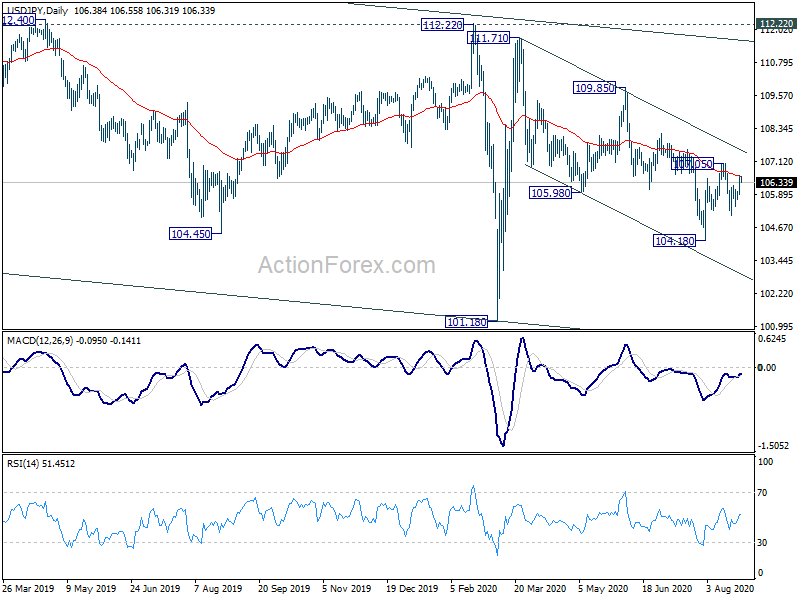

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.99; (P) 106.28; (R1) 106.70; More...

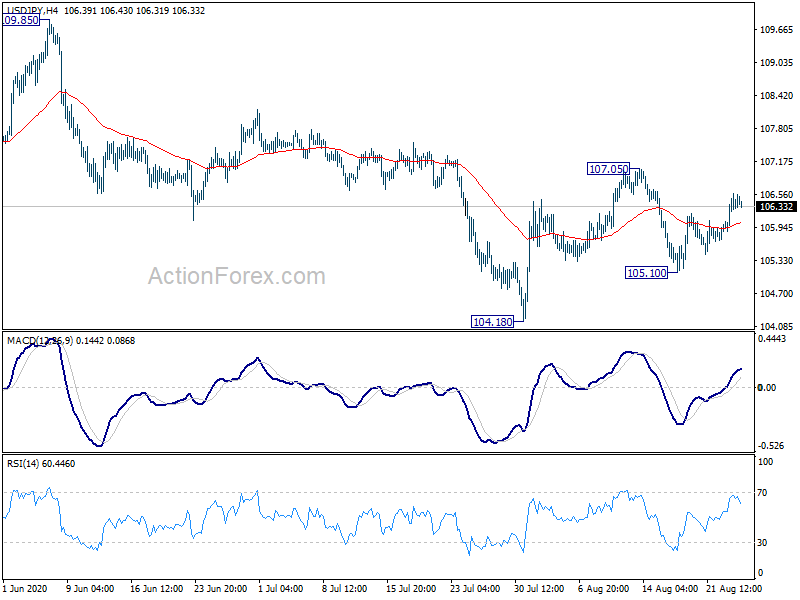

USD/JPY’s recovery from 105.10 extended higher but it’s staying in range after all. Intraday bias remains neutral first. On the upside, break of 107.05 will revive the case of near term reversal and bring stronger rally. On the downside, break of 105.10 will target a test on 104.18. Break there will resume whole decline from 111.71.

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016). Hence, there is no clear indication of trend reversal yet. The down trend could still extend through 101.18 low. However, sustained break of 112.22 should confirm completion of the down trend and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jul | 282M | 285M | 426M | 475M |

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | 1.20% | 0.80% | 0.80% | 0.90% |

| 1:30 | AUD | Construction Work Done Q2 | -0.70% | -5.80% | -1.00% | |

| 9:00 | CHF | ZEW Survey ?Expectations Aug | 42.4 | |||

| 12:30 | USD | Durable Goods Orders Jul | 3.30% | 7.60% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Jul | 2.00% | 3.40% | ||

| 12:30 | USD | Nondefense Capital Goods Orders ex Aircraft Jul | 2.30% | 3.40% | ||

| 14:30 | USD | Crude Oil Inventories | -1.6M |