{kind=link}

Reactions to the better than expected job data from US and Canada are rather muted. The greenback is currently trying to extend recovery. Yet, it’s still the worst performing one for the week. Eyes remain on developments of US-China relations. But it probably takes a bit more time for the US to announce follow-up actions to the TikTok/WeChat ban. As for the week, Sterling is currently the second weakest, followed by Swiss Franc. Australian Dollar is still the strongest. But Canadian Dollar has the potential to overtake it before weekly close.

Technically, it remains to be seen if Dollar could finally be successful in its rebound attempt. The levels to watch include 1.1695 support in EUR/USD, 1.2982 support in GBP/USD, 0.7067 support in AUD/USD, 0.9241 resistance in USD/CHF and 1.3459 resistance in USD/CAD. As usual, we’ll also watch 2028.34 support in gold to confirm any underlying strength of Dollar.

In Europe, currently, FTSE is down -0.04%. DAX is up 0.29%. CAC is down -0.18%. German 10-year yield is up 0.005 at -0.525. Earlier in Asia, Nikkei dropped -0.39%. Hong Kong HSI dropped -1.60%. China Shanghai SSE dropped -0.96%. Singapore Strait Times dropped -0.53%. Japan 10-year JGB yield dropped -0.0085 to 0.010.

US NFP grew 1763k, unemployment rate dropped to 10.2%

US non-farm payroll employment grew 1763k in July, above expectation of 1510k. Notable job gains occurred in leisure and hospitality, government, retail trade, professional and business services, other services, and health care.

Unemployment rate dropped to 10.2%, down from 11.1%, better than expectation of 10.7%. Labor force participation was little changed at 61.4%. Average hourly earning rose 0.2% mom, better than expectation of -0.5% mom decline.

Canada employment grew 418.5k, unemployment rate dropped to 10.9%

Canada employment grew 418.5k in July, below expectation of 653.3k. Combined with the 953k added in June and 290k in May, employment was brought back to within 1.3m (-7.0%) of pre-pandemic February level.

Unemployment rate dropped to 10.9%, down form 12.3%, much better than expectation of 12.8%. Labor force participation rate rose back to 64.3%, within 1.2% from February level of 65.5%.

Trade surplus in Germany and Italy widened

Germany exports dropped -9.4% yoy to EUR 96.1B in June. Imports dropped -10.0% yoy to EUR 80.5B. Trade surplus came in at EUR 15.6B. In calendar and seasonally adjusted terms, trade surplus widened to EUR 14.5B, up from EUR 7.6B, above expectation of EUR 10.3B. Industrial production rose 8.9% mom in June, above expectation of 8.8% mom.

France trade deficit widened slightly to EUR -8.0B in June, up fro EUR -7.1B. Industrial output rose 12.7% mom, above expectation of 10.0% mom. Italy trade surplus widened slightly to EUR 6.23B, up from EUR 5.58B.

China exports rose 7.2% in July, imports dropped -1.4%

In USD term, China’s exports rose 7.2% yoy to USD 237.6B in July. Imports dropped -1.4% yoy to USD 175.3B. Trade surplus came in at USD 62.3B, widened from June’s USD 46.4B, beat expectation of USD 42.5B.

Year-to-July, overall:

- Exports dropped -4.1% yoy to USD 1336B.

- Imports dropped -5.7% yoy to USD 1106B.

- Trade surplus was at USD 230B.

Year-to-July, with EU:

- Exports rose 0.7% yoy to USD 209.2B.

- Imports dropped -8.5% yoy to USD 133.5B.

- Trade surplus was at USD 75.7B.

Year-to July, with US

- Exports dropped -7.3% yoy to USD 221.3B.

- Imports dropped -3.5% yoy to USD 67.7B.

- Trade surplus was at USD 153.6B.

RBA paints slower recovery, says no to negative rates and intervention

In the Monetary Policy Statement, RBA revised down GDP projections for 2021, projecting a slower recovery. There were also upward revisions in unemployment rate forecasts and downward in inflation forecasts. The central bank also reiterated that currency intervention and negative rates no appropriate for the moment.

GDP contraction for year ending December 2020 was maintained at -6%. But a slower recovery is projected, at 5% for year ending December 2021, revised down from 6%. Growth is expected to slow further to 4% in the year ending December 2022.

Unemployment rate is projected be at 10% (revised from 9%) by 2020 end, then drop to 8.5% (revised up from 7.5%) in 2021 end, then to 7% in 2022 end. Trimmed mean inflation projections were also revised down to 1.00% (from 1.25%) in 2020 end, then 1.00% (from 1.25%) in 2021 end, and crawl back to 1.50% in 2020 end.

RBA said: “At a time when the value of the Australian dollar is broadly in line with its fundamentals and the market was working well, there was not a case for intervention in the foreign exchange market. Intervention in such circumstances is likely to have limited effectiveness.”

“The Board continues to view negative interest rates as being extraordinary unlikely in Australia. The main potential benefit is downward pressure on the exchange rate. But negative rates come with costs too. They can cause stresses in the financial system that are harmful to the supply of credit, and they can encourage people to save rather than spend.”

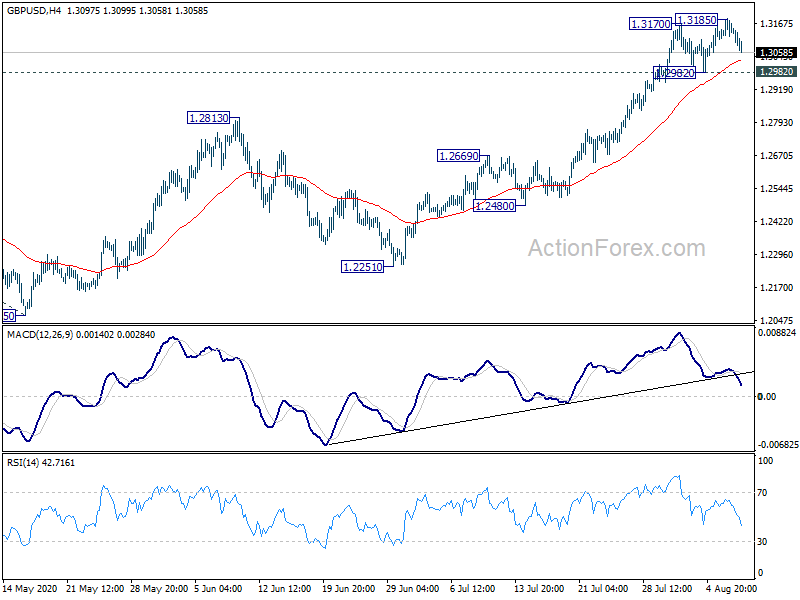

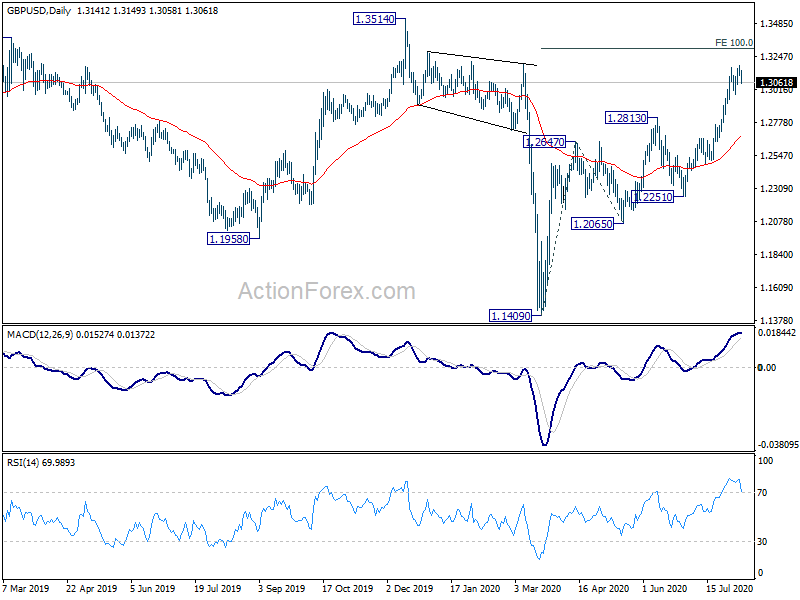

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3109; (P) 1.3147; (R1) 1.3182; More….

Intraday bias in GBP/USD remains neutral for the moment. Further rise will remain in favor as long as 1.2982 support holds. On the upside, break of 1.3185 will resume larger rally to 100% projection of 1.1409 to 1.2647 from 1.2065 at 1.3303 next. However, firm break of 1.2982 will suggest short term topping and turn bias to the downside for deeper correction to 1.2813 resistance turned support.

In the bigger picture, while the rebound from 1.1409 is strong, there is not enough evidence for trend reversal yet. Down trend from 2.1161 (2007 high) should still resume sooner or later. However, decisive break of 1.3514 should at least confirm medium term bottoming and turn outlook bullish for 1.4376 resistance first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Jul | 44 | 31.5 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jun | -1.70% | -0.60% | -2.30% | |

| 23:30 | JPY | Household Spending Y/Y Jun | -1.2 | -7.50% | -16.20% | |

| 01:30 | AUD | RBA Monetary Policy Statement | ||||

| 02:00 | CNY | Trade Balance (USD) Jul | 62.3B | 42.5B | 46.4B | |

| 02:00 | CNY | Exports (USD) Y/Y Jul | 7.20% | -0.60% | 0.50% | |

| 02:00 | CNY | Imports (USD) Y/Y Jul | -1.40% | 1.00% | 2.70% | |

| 02:00 | CNY | Trade Balance (CNY) Jul | 442B | 265B | 329B | |

| 02:00 | CNY | Exports (CNY) Y/Y Jul | 10.40% | 2.30% | 4.30% | |

| 02:00 | CNY | Imports (CNY) Y/Y Jul | 1.60% | -0.70% | 6.20% | |

| 05:00 | JPY | Leading Economic Index Jun P | 85 | 78.8 | 78.4 | |

| 06:00 | EUR | Germany Industrial Production M/M Jun | 8.90% | 8.80% | 7.80% | 7.40% |

| 06:00 | EUR | Germany Trade Balance (EUR) Jun | 14.5B | 10.3B | 7.6B | |

| 06:45 | EUR | France Trade Balance (EUR) Jun | -8.0B | -7.1B | ||

| 06:45 | EUR | France Industrial Output M/M Jun | 12.70% | 10.00% | 19.60% | |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jul | 846B | 850B | 851B | |

| 08:00 | EUR | Italy Trade Balance(EUR) Jun | 6.23B | 5.58B | ||

| 12:30 | USD | Nonfarm Payrolls Jul | 1763K | 1510K | 4800K | 4791K |

| 12:30 | USD | Unemployment Rate Jul | 10.20% | 10.70% | 11.10% | |

| 12:30 | USD | Average Hourly Earnings M/M Jul | 0.20% | -0.50% | -1.20% | -1.30% |

| 12:30 | CAD | Net Change in Employment Jul | 418.5K | 653.3K | 952.9K | |

| 12:30 | CAD | Unemployment Rate Jul | 10.90% | 12.80% | 12.30% | |

| 14:00 | USD | Wholesale Inventories Jun F | -2.00% | -2.00% | ||

| 15:00 | CAD | Ivey PMI Jul | 58.2 |