{kind=link}

Yen and Swiss Franc are trading as the strongest ones for today as stock markets are weighed down by escalating US-China tensions. Though, negative sentiments in Europe was partly offset by much stronger than expected Eurozone and UK PMIs. Signs of a V recovery are there even though the development will depend very much on the second wave of coronavirus infections. Both Euro and Sterling are resilient today. On the other hand, Australian Dollar leads other commodity currencies as the worst performing ones.

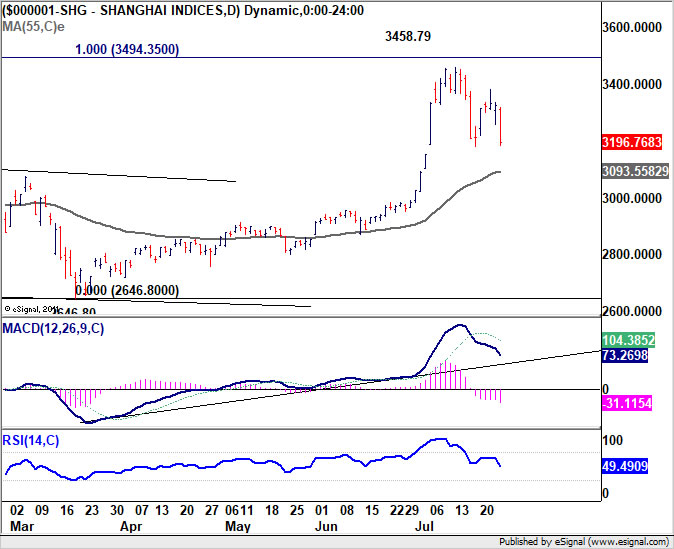

In other markets, Gold is on track to retest 1920 record high. WTI crude oil is struggling to get through 42 key resistance level. Weakness in European stocks is relatively limited. At the time of writing, FTSE is down -1.15%. DAX is down -1.53%. CAC is down -1.26%. German 10-year yield is up 0.028 at -0.451. Earlier in Asia, selloff mainly concentrated in Hong Kong and China while Japan was on holiday. Hong Kong HSI dropped -2.21%. China Shanghai SSE dropped -3.86%. Singapore Strait Times dropped -1.26%.

UK PMI composite rose to 57.1, 61-mth high, V-shaped recovery by no means assured yet

UK PMI Manufacturing rose to 53.6 in July, up from 50.1, well above expectation of 51.0. That’s also a 16-month high. PMI Services rose to 56.6, up from 47.1, above expectation of 51.0. That’s the highest level in 60 months. PMI Composite rose to 57.1, up from 47.7, a 61-month high.

Chris Williamson, Chief Business Economist at IHS Markit, said: “The UK economy started the third quarter on a strong footing as business continued to reopen doors after the COVID-19 lockdown… However, while the recession looks to have been brief, the scars are likely to be deep. Even with the July rebound there’s a long way to go before the output lost to the pandemic is regained and, while businesses grew more optimistic about the year ahead, a V-shaped recovery is by no means assured…. July’s PMI represents a step in the right direction, but there is a mountain still to climb before a sustainable recovery is in sight.”

Retail sales, in volume term, rose 13.9% mom in June, much better than expectation of 8.5% mom. Excluding automotive fuel, sales rose 13.5% mom, also well above expectation of 7.5% mom. Total sales have now recovered back to similar levels as before the coronavirus pandemic.

Gfk Consumer Confidence came in at -27 in July, up from June’s -30, unchanged from flash reading. Joe Staton, GfK’s Client Strategy Director, says: “There’s been little to boost the public’s mood as the cost of the pandemic to the UK’s economy is becoming apparent. Amidst significant job losses and the end of the furlough scheme, it is perhaps surprising Consumer Confidence has held steady at -27 this month.

Eurozone PMI composite rose to 54.8, 25-mth high, hints at initial V recovery

Eurozone PMI Manufacturing rose to 51.1 in July, up from 47.4, a 19-month high. PMI Services rose to 55.1, up from 48.3, a 25-month high. PMI Composite rose to 54.8, up from 48.5, a 25-month high.

Chris Williamson, Chief Business Economist at IHS Markit said: “Companies across the euro area reported an encouraging start to the third quarter, with output growing at the fastest rate for just over two years in July as lockdowns continued to ease and economies reopened…. However, while the survey’s output measures hint at an initial v-shaped recovery, other indicators such as backlogs of work and employment warn of downside risks to the outlook…. The concern is that the recovery could falter after this initial revival.”

Germany PMI Manufacturing rose to 50.0 in July, up from 45.2, better than expectation of 48.3. PMI Services rose to 56.7, up from 47.3, hitting a 30-month high. PMI Composite rose to 55.5, up from 47.0, a 23-month high. It’s also the first expansionary reading since February.

France PMI Manufacturing rose dropped to 52.0 in June, down from 52.3, missed expectation of 53.2. PMI Services rose to 57.8, up from 50.7, well above expectation of 52.3. That’s also the highest level in 30 months. PMI Composite rose to 57.6, up from 51.7, also a 30-month high.

Australia CBA PMI services rose to record 58.5, PMI manufacturing up to 53.4

Australia CBA PMI Composite rose to 57.9, up from 52.7, highest since April 2017. PMI Services rose to 58.5, up from 53.1, highest on record since the survey began in May 2016. PMI Manufacturing rose to 53.4 in July, up from 51.2.

CBA Head of Australian Economics, Gareth Aird said: “The improvement in growth momentum in July is welcome, but concerns around COVID-19 and the potential policy responses to a lift in the number of new cases continue to weigh on activity. The fall in employment looks a little surprising given some other measures of labour demand have firmed more recently. But encouragingly the acceleration of growth in new orders suggests labour demand should improve. The lack of any inflationary pulse was once again evident. That supports our view that we will be in a low inflation environment for an extended period of time”.

New Zealand reported first quarterly trade surplus since 2014, NZD/JPY rejected by 71.66 resistance

New Zealand’s good exports rose 2.2% yoy, or NZD 107m, to NZD 5.1B in June. Goods imports rose 0.2% yoy, or NZD 11m, to NZD 4.6B. Monthly trade surplus narrowed to NZD 426m, down from may’s NZD 1286m, slightly below expectation of NZD 450m.

Over June quarter, goods exports dropped -5.8% yoy, or NZD 904m, to NZD 14.7B. Goods imports dropped -16% yoy, or NZD 2.5B, to NZD 13.2B. Quarterly trade balance was a surplus of NZD 1.4B, first quarterly surplus since Q1 2014.

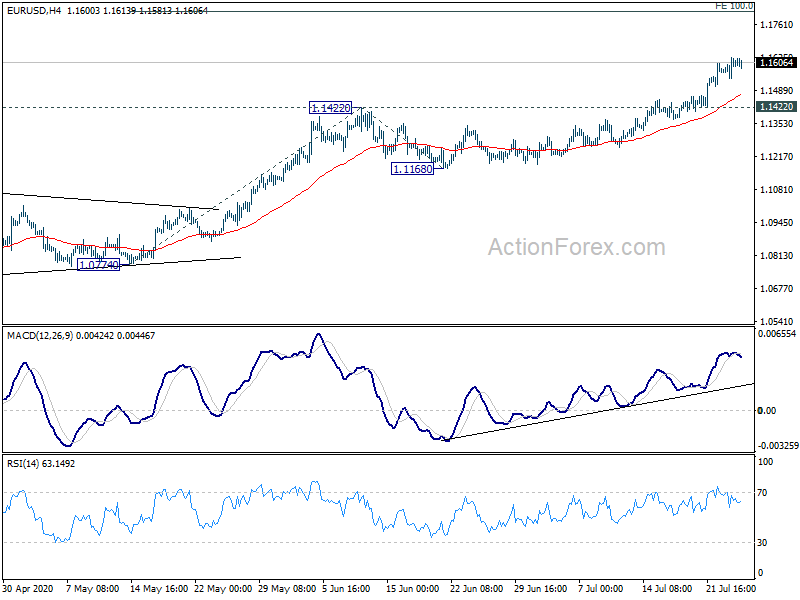

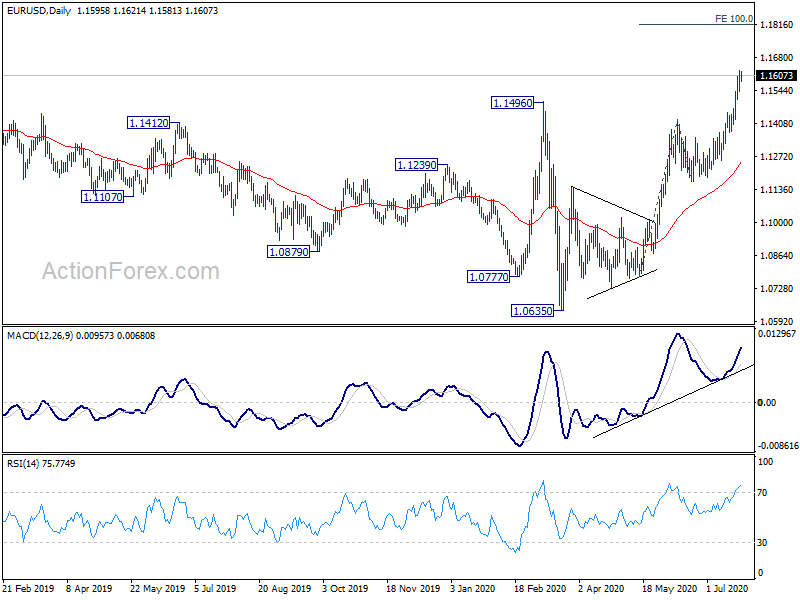

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1548; (P) 1.1588; (R1) 1.1635; More…..

Intraday bias in EUR/USD remains on the upside at this point. Current rise from 1.0635 is still in progress for 100% projection of 1.0774 to 1.1422 from 1.1168 at 1.1816 next. On the downside, break of 1.1422 resistance turned support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, sustained trading above 1.1496 key resistance will argue that whole down trend from 1.2555 (2018 high) has completed at 1.0635. Rise from 1.0635 would then be seen as the third leg of the pattern from 1.0339. Further medium term rally would be seen to retest 1.2555. This will now be the favored case as long as 1.1168 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jun | 426M | 450M | 1253M | 1286M |

| 23:00 | AUD | CBA Manufacturing PMI Jul P | 53.4 | 51.2 | ||

| 23:00 | AUD | CBA Services PMI Jul P | 58.5 | 53.1 | ||

| 23:01 | GBP | GfK Consumer Confidence Jul | -27 | -26 | -27 | |

| 6:00 | GBP | Retail Sales M/M Jun | 13.90% | 8.50% | 12.00% | |

| 6:00 | GBP | Retail Sales Y/Y Jun | -1.60% | -6.20% | -13.10% | |

| 6:00 | GBP | Retail Sales ex-Fuel M/M Jun | 13.50% | 7.50% | 10.20% | |

| 6:00 | GBP | Retail Sales ex-Fuel Y/Y Jun | 1.70% | -3.70% | -9.80% | |

| 7:15 | EUR | France Manufacturing PMI Jul P | 52 | 53.2 | 52.3 | |

| 7:15 | EUR | France PMI Services Jul P | 57.8 | 52.3 | 50.7 | |

| 7:30 | EUR | Germany Manufacturing PMI Jul P | 50 | 48.3 | 45.2 | |

| 7:30 | EUR | Germany Services PMI Jul P | 56.7 | 50.4 | 47.3 | |

| 8:00 | EUR | Eurozone Manufacturing PMI Jul P | 51.1 | 49.5 | 47.4 | |

| 8:00 | EUR | Eurozone Services PMI Jul P | 55.1 | 51 | 48.3 | |

| 8:30 | GBP | Manufacturing PMI Jul P | 53.6 | 51 | 50.1 | |

| 8:30 | GBP | Services PMI Jul P | 56.6 | 51 | 47.1 | |

| 13:45 | USD | Manufacturing PMI Jul P | 51.3 | 49.8 | ||

| 13:45 | USD | Services PMI Jul P | 50.2 | 47.9 | ||

| 14:00 | USD | New Home Sales Jun | 700K | 676K |