{kind=link}

Sterling tumbles broadly today as another round of Brexit negotiations ended without making any significant progress. Though, Aussie is even weaker as traders are finally taking profits on this week’s strong rally. Swiss Franc, on the other hand, rebound strongly, particular against Euro as the lift from EU recovery funds fade. Dollar is mixed for today, staying as the weakest for the week together with Yen. Stock markets are mixed, shrugging off rebound in US jobless claims, continuously increasing global coronavirus cases, and quickly deteriorating US-China relations.

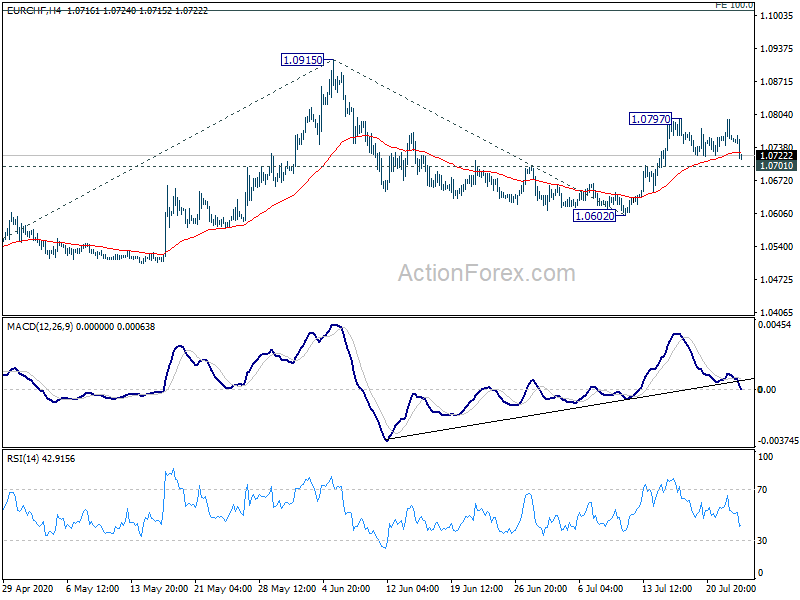

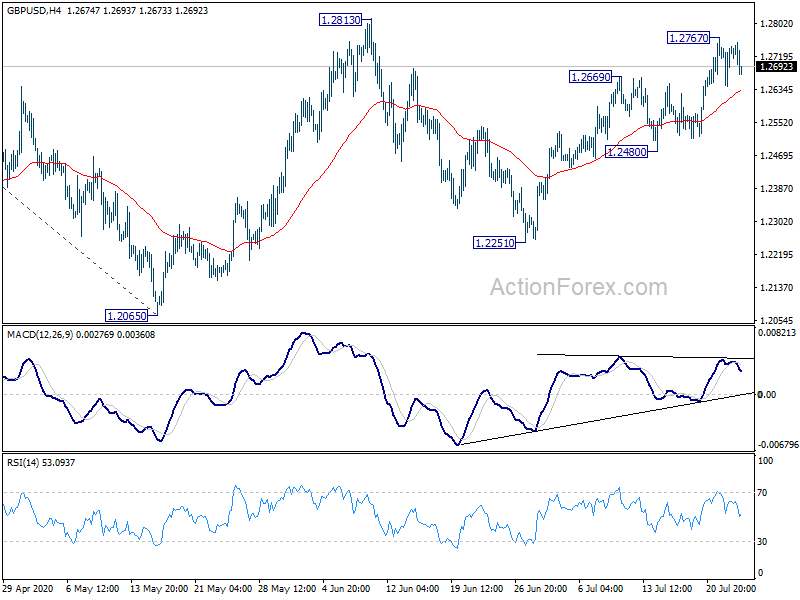

Technically, Dollar should have found a temporary low against Euro, Sterling and Australia. But no bottoming is confirmed until 1.1402 support in EUR/USD, 1.2480 support in GBP/USD and 0.6963 support in AUD/USD are taken out. EUR/CHF could be a focus before weekly close. As long as 1.0701 minor support holds, rise from 1.0602 is still expected to resume through 1.0797 to 1.0915 high. But break of 1.0701 will suggest completion of the rebound and turn focus back to 1.0602.

In Europe, currently, FTSE is up 0.34%. DAX is up 0.11%. CAC is up 0.01%. German 10-year yield is up 0.003 at -0.487. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.82%. China Shanghai SSE dropped -0.24%. Singapore Strait Times rose 0.69%.

US initial jobless claims rose back to 1416k, above expectations

US initial jobless claims rose 109k to 1416k in the week ending July 18, above expectation of 1280k. Four-week moving average of initial claims dropped -16.5k to 1360k. Continuing claims dropped -1107k to 16197k in the week ending July 11. Four-week moving average of continuing claims dropped -759k to 17505k.

Considerable gaps remain in the most difficult areas after Brexit talks

Another round of Brexit negotiations have completed in London and there appeared to be no significant progress. UK chief negotiator David Frost said “considerable gaps remain in the most difficult areas. That is, the so-called level playing field and on fisheries.” “Early understanding on the principles underlying any agreement” wouldn’t be reached within this month.

But Frost added: “Despite all the difficulties, on the basis of the work we have done in July, my assessment is that agreement can still be reached in September, and that we should continue to negotiate with this aim in mind.”

EU chief negotiator Michel Barnier said: “By its current refusal to commit to conditions of open and fair competition and to a balanced agreement on fisheries, the UK makes a trade agreement – at this point – unlikely.”

BoE Haskel: Evidence emerging that dominant driver of current activity on demand side

BoE MPC member Jonathan Haskel said in a speech that the coronavirus lockdown can be thought of as a “supply shock” to the economy. But at the same time, consumers’ behavioral response” could be though of as a “demand shock”. “Evidence is emerging that the dominant driver of activity will in fact be on the demand side,” he added.

“When the economy re opens, customers might still fear infection and therefore stay away from consumption that has a social element to it (pubs, restaurants etc.). It seems likely that such demand weakness will therefore drag on the economy and hold back the recovery.”

“The path of recovery crucially depends therefore on the fear of infection, which in turn depends on the mix of public (e.g. track and trace) and private (e.g. screens in shops) health measures undertaken. It also depends on the fear, or realisation, of unemployment, as weak activity and capacity constraints on the operation of surviving businesses, and insolvencies, translate into a fall in the demand for labour.”

UK CBI order book balance rose to -46, tentative signs of gradual recovery on the horizon

UK CBI monthly order book balance rose to -46 in July, up from -58. While that was the best reading since March, it missed expectation of -35. Output volumes dropped further to -59, down from -57, worst on record since 1975.

Rain Newton-Smith, CBI Chief Economist, said: “There are tentative signs of gradual recovery on the horizon, with firms expecting output and orders to begin to pick up in the next three months. But demand still remains deeply depressed.”

Tom Crotty, Group Director at INEOS and Chair of the CBI Manufacturing Council, said: “The latest survey showcases the significant challenges that manufacturers have faced over the last three months due to the COVID-19 crisis. However, these results may prove to be a low point in the crisis, with manufacturers expecting output to grow for the first time since the pandemic hit.”

Germany Gfk consumer sentiment rose to -0.3, V-sharped trend emerging

Germany Gfk consumer sentiment for August rose to -0.3, up from -9.6, beat expectation of -4.5. Gfk said: “Consumers are “gradually putting the coronavirus shock of earlier this year behind them. While economic expectations have once again gained slightly, income expectations and the propensity to buy have seen a significant increase for the third consecutive time.” Gfk added, “a V-shaped trend is currently emerging for the consumer climate:”

Looking at some details, economic expectations rose from 8.5 to 10.6. Income expectations rose from 6.6 to 18.6. Propensity to buy rose from 19.4 to 42.5.

Australia budget deficit widened to 4.3% of GDP in fiscal 2020, sets to balloon further

Australia Treasurer Josh Frydenberg said the country’s budget balance had turned into a massive deficit of AUD 85.8B, or 4.3% of GDP, in the fiscal year ended June 2020. The deficit is expected to widen further to AUD 184.5B in fiscal 2020-21. Gross debt is projected to rise from AUD 684.3B in 2019-20 to AUD 851.9B in 2020-21.

He added that GDP could have falling by -7% in June quarter. GDP is expected to drop -0.25% in fiscal 2019-20 and -2.25% in fiscal 2020-21. Unemployment rate is expected to climb from 7.0% to 8.75% in 2020-21, and would probably hit 9.25% by Christmas this year.

S&P Global Ratings said Australia’s AAA credit rating could withstand the large widening in budget deficit as projected. The rating reflects the expectation that the economy will begin to recover from recessing during fiscal 2021. Nevertheless, “risks to our rating remain tilted toward the downside as the effects of the COVID-19 pandemic and government responses on the economy, budget, and financial markets evolve.”

Australia NAB business confidence dropped to -15 in Q2, forward looking conditions deteriorated

Australia NAB Quarterly Business Confidence dropped to -15 in Q2, down from Q1’s -12. Current Business Conditions dropped to -26, down from -3. That’s also the lowest reading since early 1990s. Conditions for next three months dropped to -22, down from -4. Conditions for the next 12 months dropped to -18, down form 7. Next 12 months capex plan also dropped to -8, down from 17.

South Korea GDP dropped -3.3% qoq in Q2, worst since 1998

South Korea’s GDP contracted -3.3% qoq in Q2, as shown in data released by Bank of Korea. The decline was the worst since Q1 1998, and steeper than analysts’ expectations of around -2.3% qoq. Also, with Q1’s -1.3% fall, South Korean’s economy has formally entered a technical recession this year, joining other major Asian countries like Japan and Singapore. Annually, GDP shrank -2.9% yoy in Q2.

“It’s possible for us to see China-style rebound in the third quarter as the pandemic slows and activity in overseas production, schools and hospitals resume,” South Korean finance minister finance minister Hong Nam-ki said after the data was released.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2674; (P) 1.2709; (R1) 1.2774; More….

Intraday bias in GBP/USD is turned neutral for consolidation below 1.2767 temporary top. Further rise will remain in favor as long as 1.2480 support holds. On the upside, above 1.2767 will target 1.2813 resistance first. Break there will resume whole rise from 1.1409. Next target will be 100% projection of 1.1409 to 1.2647 from 1.2065 at 1.3303.

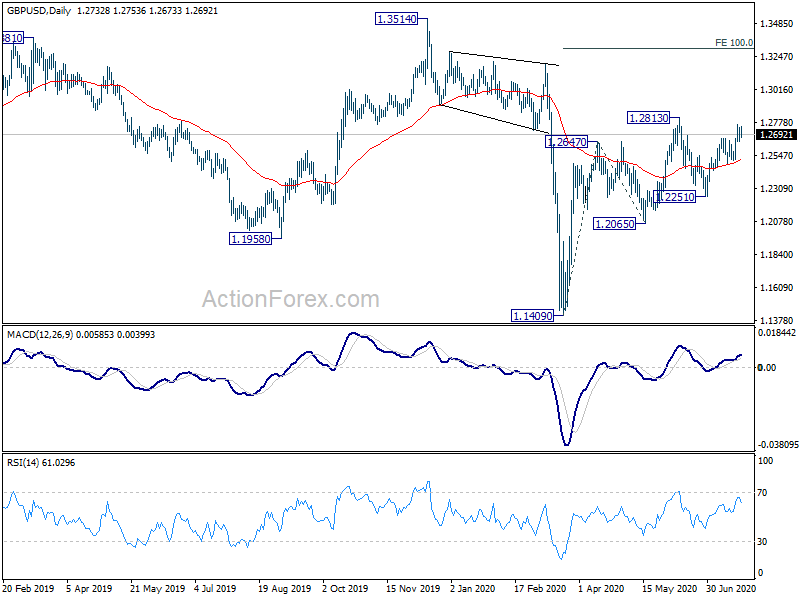

In the bigger picture, while the rebound from 1.1409 is strong, there is not enough evidence for trend reversal yet. Down trend from 2.1161 (2007 high) should still resume sooner or later. However, decisive break of 1.3514 should at least confirm medium term bottoming and turn outlook bullish for 1.4376 resistance first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | NAB Business Confidence Q2 | -15 | -11 | -12 | |

| 6:00 | EUR | Germany Gfk Consumer Confidence Aug | -0.3 | -4.5 | -9.6 | |

| 10:00 | GBP | CBI Industrial Order Expectations Jul | -46 | -35 | -58 | |

| 12:30 | USD | Initial Jobless Claims (Jul 17) | 1416K | 1280K | 1300K | 1307K |

| 14:00 | EUR | Eurozone Consumer Confidence Jul P | -12 | -15 | ||

| 14:30 | USD | Natural Gas Storage | 37B | 45B |