{kind=link}

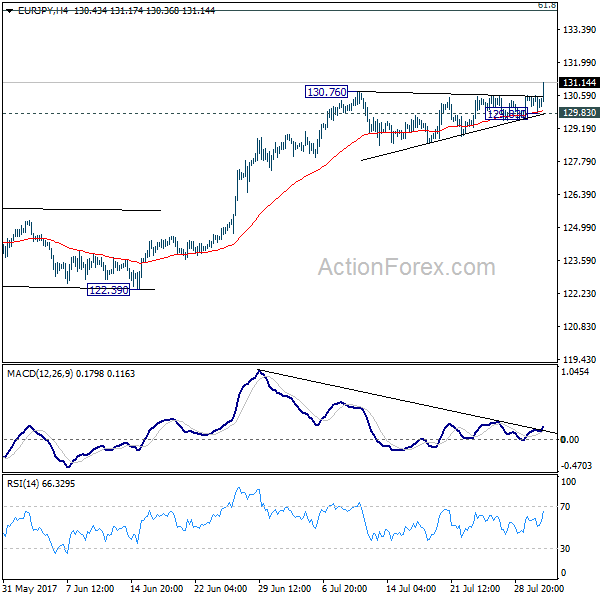

Yen falls sharply in Asian session on risk appetite flows. Strong earnings from Japanese companies lifted Nikkei back above 20000 handle as the index is trading up 0.6% at the time of writing. That followed another record close in DOW overnight, at 21963.92, up 0.33%. Euro is benefiting most from the developments, in particular, with EUR/JPY finally taking out 130.76 resistance to resume recent rally. Markets will have an eye on German DAX today, which rebound by 1.1% yesterday. That mark the complete of a recent correction and if that’s the case, strength in DAX would likely support the Euro further. Meanwhile, Dollar also recovers mildly today, against most except Euro as markets await ADP private employment data from US. Talking about employment, New Zealand Dollar is trading as the weakest one as dragged down by Q2 job data.

DAX could have finished pull back

DAX recover strongly after drawing support from medium term channel. It was also kept slightly above key cluster support at 11941.57, 38.2% retracement of 10402.59 to 12951.54 at 11977.84, as well as 12000 psychological level. Focus is now back on 12341.03 resistance. Break will suggest that the correction from 12951.53 has completed. And in that case, further rise would be seen back to retest 12951.54 later in the quarter. Such development would be Euro supportive.

Oil failed 50, lifting USD/CAD

Oil price is another one to watch today. WTI reached as high as 50.43 earlier this week but failed to sustain above 50 handle. It’s now back below 49. The development is lifting USD/CAD through 1.2575 resistance. This signals that USD/CAD has bottomed at 1.2412 in near term after drawing support from 1.2460 key support level. As long as WTI stays above 47.32 in the current pull back, rebound in USD/CAD should be limited. But break of 47.32 in oil will possibly send USD/CAD back towards 1.3 handle in a larger scale corrective rebound.

BoJ Funo urges structural reforms

BoJ board member Yukitoshi Funo reiterated the central bank’s stance that "powerful" monetary stimulus should be maintained to boost inflation, which is far below target. But he emphasized that monetary stimulus alone is not enough and called for structural reforms. He said that "japan’s economy still has room to raise productivity when seen from a global perspective." And, "now is a good chance to proceed with structural reforms and growth strategies, because monetary conditions are very loose and the job market is tight." He is optimistic that a strong economy and a tightening job market will likely gradually push up wages and inflation.

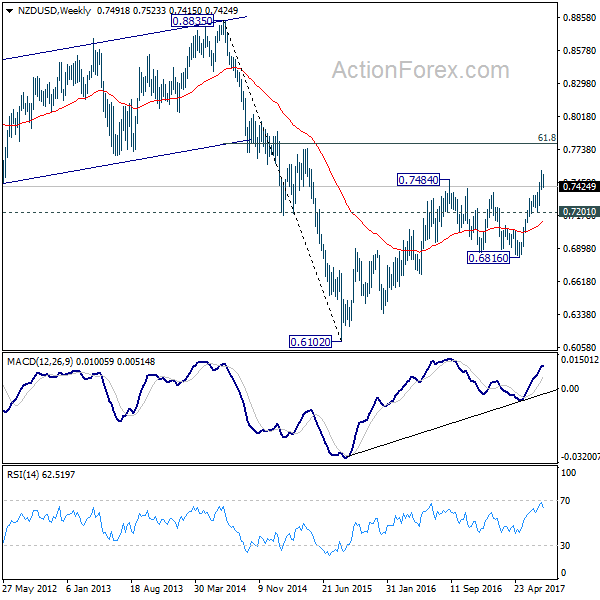

Kiwi lower as employment shrank in Q2

New Zealand employment dropped -0.2% qoq in Q2, much weaker than expectation of 0.7% qoq rise. Unemployment rate dropped to 4.8%, down from 4.9%. Private sector labor cost rose 0.4% qoq, in line with consensus. The data affirmed RBNZ’s stance to stand pat in the environment of global policy stimulus exit. NZD/USD dips notable today to 0.7420 and the development confirms short term topping at 0.7553 last week. But overall, there is no change in the bullish outlook. NZD/USD is now in short term consolidation and could dip lower. But downside should be contained by 0.7201 support to bring another rise. Rise from 0.6816 is seen as resuming the medium term rebound from 0.6102. Another rally is expected to 61.8% retracement of 0.8835 to 0.6102 at 0.7791 next.

US ADP to highlight the day

Also released earlier today, Australia building approvals rose 10.9% mom in June. Japan monetary base rose 15.6% yoy in July. UK BRC shop price index dropped -0.4% yoy in July. Swiss will release a bunch of data today including SECO consumer confidence, SVME PMI and retail sales. UK will release construction PMI. Eurozone will release PPI. US ADP private employment will be the main focus of the day.

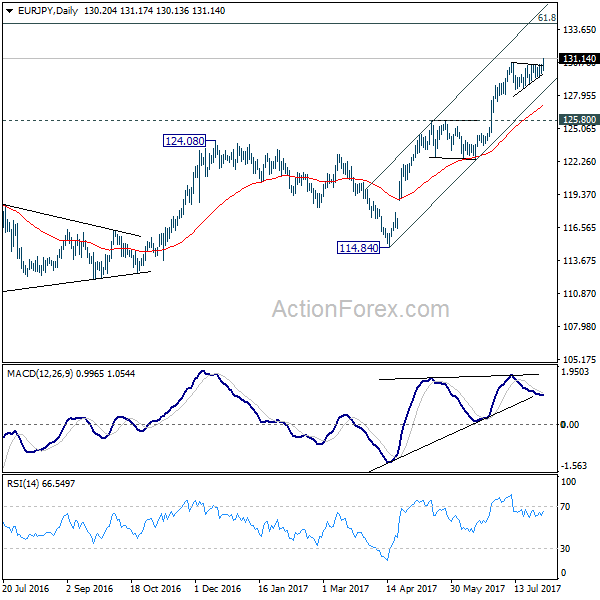

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.87; (P) 130.23; (R1) 130.63; More…

EUR/JPY’s rally resumes by taking out 130.76 and reaches as high as 131.17 so far. Intraday bias is back on the upside. Current rise should now target next long term fibonacci level at 134.20. On the downside, break of 129.83 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 125.80 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Unemployment Rate Q2 | 4.80% | 4.80% | 4.90% | |

| 22:45 | NZD | Employment Change Q/Q Q2 | -0.20% | 0.70% | 1.20% | 1.10% |

| 22:45 | NZD | Labor Cost Private Sector Q/Q Q2 | 0.40% | 0.40% | 0.40% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Jul | -0.40% | -0.30% | ||

| 23:50 | JPY | Monetary Base Y/Y Jul | 15.60% | 16.60% | 17.00% | |

| 1:30 | AUD | Building Approvals M/M Jun | 10.90% | 1.00% | -5.60% | -5.40% |

| 5:00 | JPY | Consumer Confidence Index Jul | 43.5 | 43.3 | ||

| 5:45 | CHF | SECO Consumer Confidence Jul | -3 | -8 | ||

| 7:15 | CHF | Retail Sales (Real) Y/Y Jun | 1.30% | -0.30% | ||

| 7:30 | CHF | SVME PMI Jul | 58.8 | 60.1 | ||

| 8:30 | GBP | Construction PMI Jul | 54 | 54.8 | ||

| 9:00 | EUR | Eurozone PPI M/M Jun | -0.10% | -0.40% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Jun | 2.40% | 3.30% | ||

| 12:15 | USD | ADP Employment Change Jul | 190K | 158K | ||

| 14:30 | USD | Crude Oil Inventories | -7.2M |