{kind=link}

Sterling continues to trade as the strongest one on stimulus optimism while Europe majors are also firm. On the other hand, Dollar remains the weakest one, even worse than Japanese Yen. Stock market rally might take a breath again today with US futures pointing to flat open. Major European indices are also mixed. After all, there is still not clear sign of topping in risk markets despite resurgence of coronavirus infections. But, due to lack of fresh inspirations, movements in the markets are relatively muted.

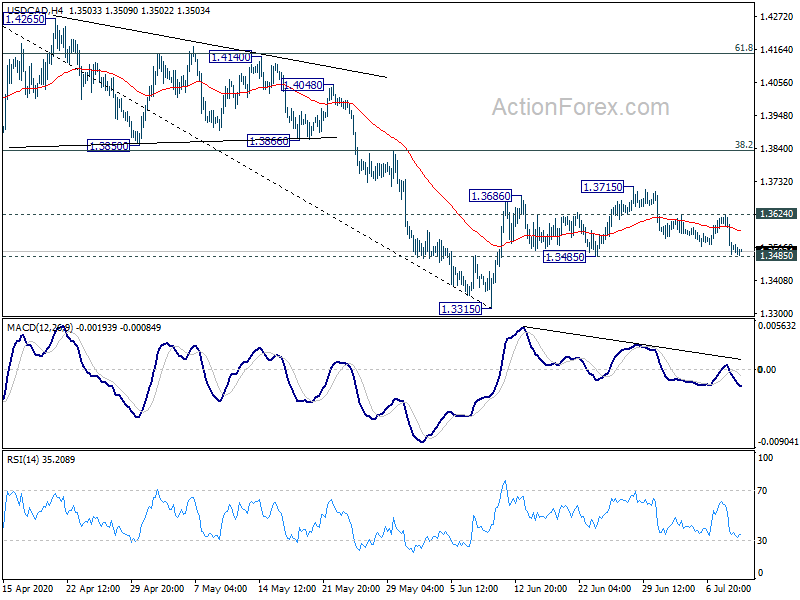

Technically, EUR/USD’s rally is somewhat lacking follow through momentum, partly thanks weakness in EUR/GBP. Nevertheless, further rise is still mildly in favor to retest 1.1422 short term top. EUR/JPY continues to eye 122.11 resistance and break could bring upside acceleration towards 124.43 short term top. If that happens, EUR/USD could be lifted too. Another immediate focus is 1.3485 support in USD/CAD and break will indicate completion of rebound from 1.3315, and bring retest of this low. This might be an early signal of comeback of commodity currencies.

In Europe, currently, FTSE is down -0.43%. DAX is up 1.55%. CAC is up 0.42%. German 10-year yield is down -0.0104 at -0.446. Earlier in Asia, Nikkei rose 0.40%. Hong Kong HSI rose 0.31%. China Shanghai SSE rose 1.39%. Singapore Strait Times dropped -0.63%. Japan 10-year JGB yield dropped -0.0002 to 0.019.

US initial jobless claims dropped -99k to 1314k

US initial jobless claims dropped -99k to 1314k in the week ending July 4, slightly below expectation of 1375k. Four-week moving average of initial claims dropped -63k to 1437k.

Continuing claims dropped -698k to 18062k in the week ending June 27. Four-week moving average of continuing claims dropped -636k to 19.086k.

Germany exports dropped -29.7% yoy in May, imports dropped -21.7% yoy

Germany’s export dropped -29.7% yoy to EUR 80.3B in May. Imports dropped -21.7% yoy to EUR 73.2B. Trade surplus widened to EUR 7.1B (or EUR 7.6B calendar and seasonally adjusted). Current account of the balance of payments showed a surplus of EUR 6.5B.

Exports to EU countries dropped -29.0% yoy while imports dropped -25.2% yoy. Exports to non-EU countries dropped -30.5% yoy while imports dropped -17.5% yoy.

BoJ Kuroda: Severe situation to continue but economy will gradually resume

In the branch managers’ meeting, BoJ Governor Haruhiko Kuroda said “economic activity is expected to gradually resume”. But, for the time being “severe situation will continue due to the impact of infectious diseases both inside and outside Japan”.

“If the impact of the infectious disease then subsides, pent-up demand (restricted demand) is expected to emerge and recovery production is expected. As a result, the Japanese economy is expected to improve,” he added.

As for monetary policy, Kuroda said “we will closely monitor the effects of the new coronavirus infection and, if necessary, take additional monetary easing measures without hesitation. It is assumed that the policy interest rate will remain at or below the current level of long and short interest rates.”

Released from Japan, M2 rose 7.2% yoy in June. Machine orders rose 1.7% mom in May, much better than expectation of -5.4% mom decline.

New Zealand ANZ business confidence rose to -29.8, activity outlook jumped to -6.8

New Zealand ANZ Business Confidence rose 4.6 pts from -34.4 to -29.8 in the preliminary July reading. Own Activity Outlook rose even sharply by 19.1 pts from -25.9 to -6.8. Looking at some other details, investment intentions rose from -20.5 to -4.5. Employment intentions rose from -34.7 to -15.3. Profit expectations rose from -46.8 to -25.8.

ANZ said: “New Zealand is in an enviable position (touch wood), with activity largely back to normal, as demonstrated by traffic and spending data and many other indicators. After the rigorous of lockdown we deserve a pat on the back and a little splurge…. Uncertainty is extreme and the global outlook dire. But for now, we’re getting on with our economic lives, and that’ll be helping to repair business’ balance sheets.”

China CPI accelerated to 2.5%, PPI improved slightly

Headline CPI improved further to 2.5% yoy in June, from 2.4% a month ago. This came in line with market expectations Core CPI (excluding food and energy) eased to 0.9% yoy, from 1.1% in May. While staying in the negative territory, PPI improved to -3% yoy in June, up from -3.7% a month ago. This came in better than consensus of -3.2%.

Inflation is expected to slow in the coming months as the flooding-driven increase in food prices should prove short-lived. The inflation report affirmed our view that PBOC will maintain an expansionary, but targeted, monetary policy stance.

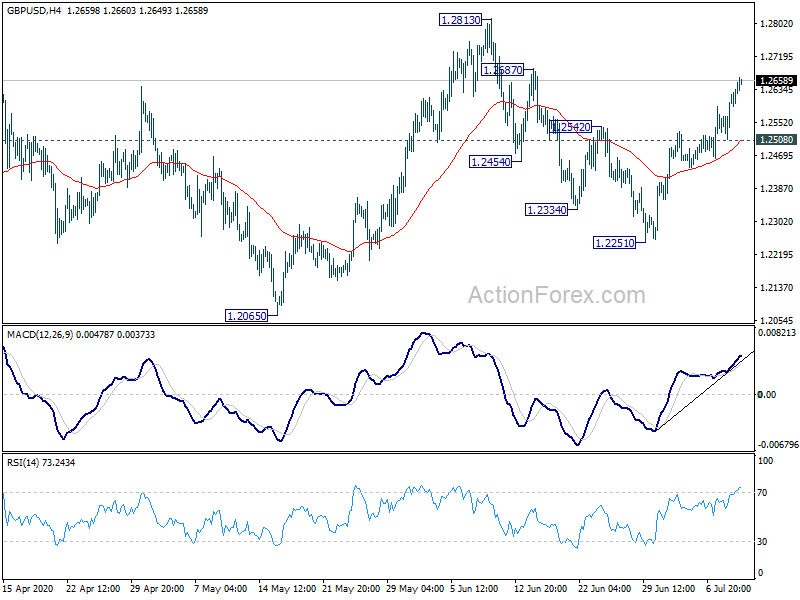

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2541; (P) 1.2582; (R1) 1.2655; More….

Intraday bias in GBP/USD remains on the upside as rise from 1.2251 is in progress for 1.2587 resistance. Break will bring retest of 1.2813 high. On the downside, though, break of 1.2462 support will turn bias back to the downside for 1.2251 support instead.

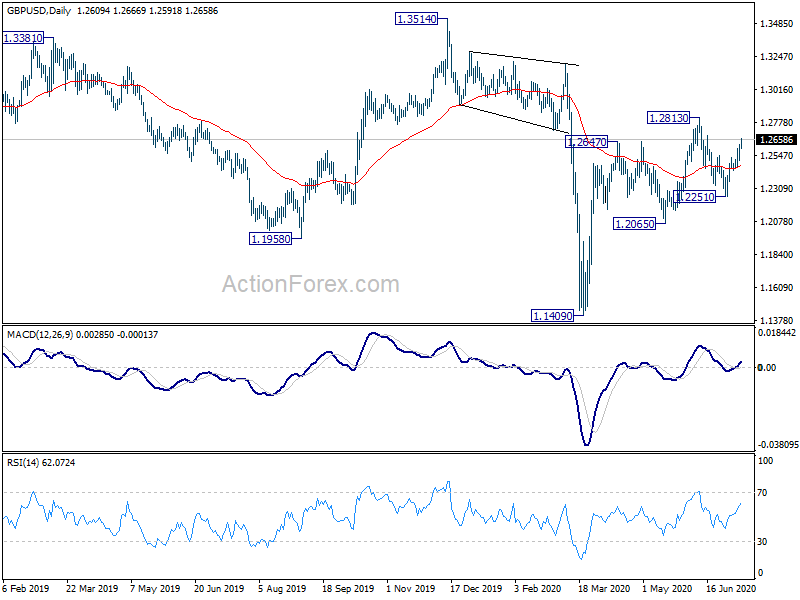

In the bigger picture, while the rebound from 1.1409 is strong, there is not enough evidence for trend reversal yet. Down trend from 2.1161 (2007 high) should still resume sooner or later. However, decisive break of 1.3514 should at least confirm medium term bottoming and turn outlook bullish for 1.4376 resistance first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Jun | -15% | -25% | -32% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Jun | 7.20% | 5.10% | ||

| 23:50 | JPY | Machinery Orders M/M May | 1.70% | -5.40% | -12.00% | |

| 01:30 | CNY | CPI Y/Y Jun | 2.50% | 2.50% | 2.40% | |

| 01:30 | CNY | PPI Y/Y Jun | -3.00% | -3.20% | -3.70% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Jun P | -32.00% | -52.80% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) May | 7.6B | 6.6B | 3.2B | |

| 12:15 | CAD | Housing Starts Jun | 212K | 192.5K | 193.5K | 195K |

| 12:30 | USD | Initial Jobless Claims (Jul 3) | 1314K | 1375K | 1427K | 1413 K |

| 14:00 | USD | Wholesale Inventories May F | -1.20% | -1.20% | ||

| 14:30 | USD | Natural Gas Storage | 60B | 65B |