{kind=link}

The markets continue trade in consolidative mode today. US stocks reversed earlier loss to closed higher overnight, ignoring the surge in coronavirus cases. Asian markets are mixed, with mild weakness in Hong Kong HSI. it’s weighed down by US Senate’s unanimous passage of a bill that could lead to sanctions on Chinese and Hong Kong officials, as well as banks and companies, who undermine the city’s autonomy. In the currency markets, all major pairs and crosses are confined within last week’s range, with Yen, Canadian and Dollar on the red side.

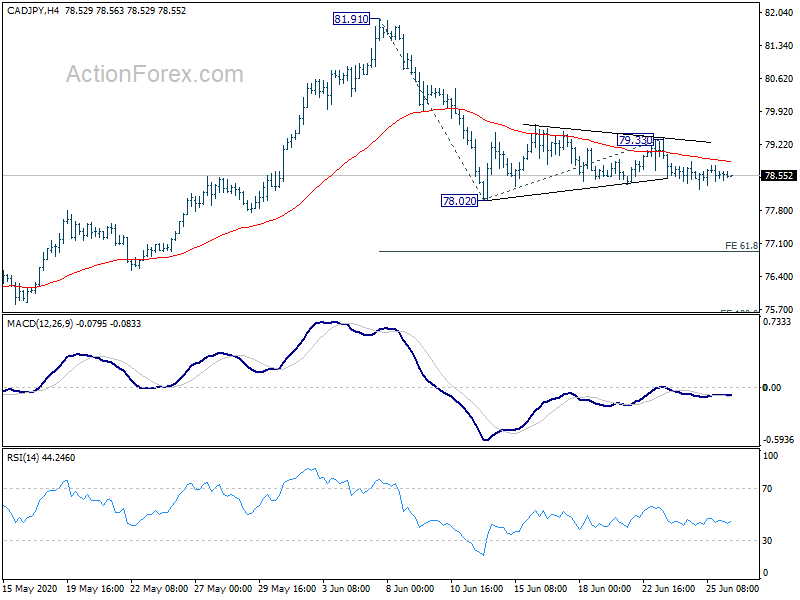

Technically, the markets remain rather dull in range. But recent development favors more downside in commodity currencies, in particular against Yen. Focus will be on 78.02 support in CAD/JPY, 72.52 support in AUD/JPY and 68.19 support in NZD/JPY. Break of these levels could be triggered by deeper corrections in global stocks. But that might not happen before during the rest of this week.

In Asia, currently, Nikkei is up 1.37%. Hong Kong HSI is down -0.57%. China Shanghai SSE rose 0.30%. Singapore Strait Times rose 0.93%. Japan 10-year JGB yield is down -0.0047 at 0.012. Overnight, DOW rose 1.18%. S&P 500 rose 1.10%. NASDAQ rose 1.09%. 10-year yield dropped -0.010 to 0.674.

BoJ Kuroda: No need to further lower the entire yield curve for now

BoJ Governor Haruhiko Kuroda said today that “at this moment, we didn’t see the need to further lower the entire yield curve”. The economy has been in a “extremely severe situation” with “considerable negative growth” in Q2. Nevertheless, “once the impact of COVID-19 on the economy has subsided, the economy starts to recover and comes back to a normal growth path, then of course our extraordinary measures may be gradually curtailed.”

But he also noted that “there are significant uncertainties over the outlook for the economy.” The coronavirus pandemic “continues on a global basis, and concern about a second wave of the virus has increased recently.”

He added that 2% inflation target is “unlikely to be met in the short run”. Also, “the BOJ’s expanded balance sheet would not be normalized until 2% inflation is achieved.”

Released from Japan, Tokyo CPI was unchanged at 0.2% yoy in June, matched expectations.

Fed George: Takes a while before dust settles before seeing need for further accommodation

Kansas City Fed President Esther George warned yesterday that “a full recovery is still far off” despite the strong job gains in some industries in May.

“Extraordinary uncertainty about the path of the pandemic over the second half of the year and the economic outlook will require a fair amount of patience and wisdom as we navigate the likely long-lasting implications of the coronavirus shock,” She added.

“Indicators are expected to improve in the third quarter even as the level of activity remains depressed,” but “it might be awhile before the dust settles and we gain insight on whether further accommodation is necessary or not,” she said.

Looking ahead

Eurozone will release M3 money supply in European session. Later in the day, US will release personal income and pending, together with PCE inflation.

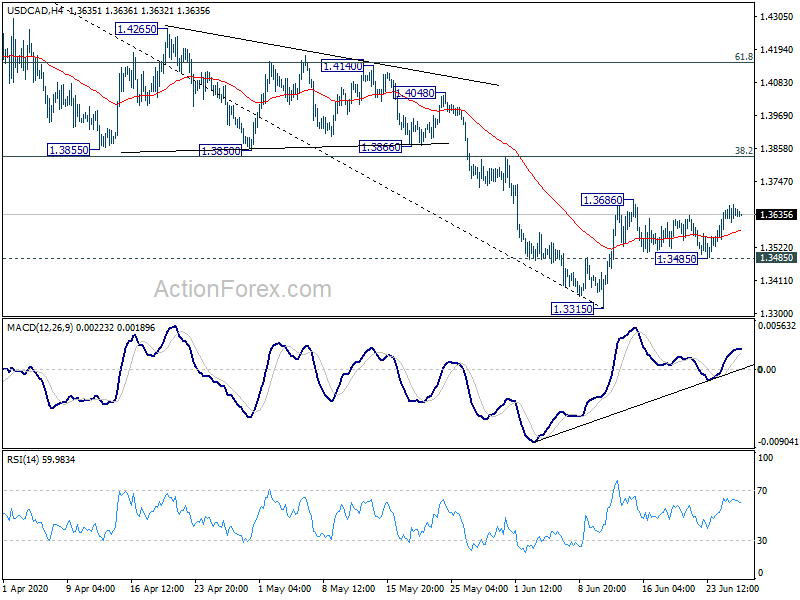

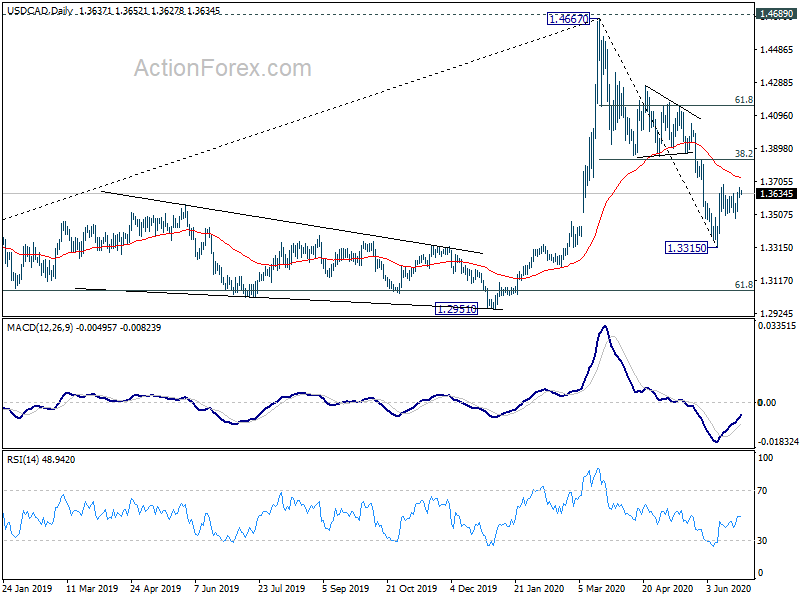

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3610; (P) 1.3640; (R1) 1.3672; More….

Intraday bias in USD/CAD stays neutral as range trading continues. Rebound from 1.3315 short term bottom is likely not over. On the upside, break of 1.3686 will turn bias to the upside for 38.2% retracement of 1.4667 to 1.3315 at 1.3831 next. However, break of 1.3485 minor support will turn bias back to the downside for retesting 1.3315 low.

In the bigger picture, the rise from 1.2061 (2017 low) could have completed at 1.4667 after failing 1.4689 (2016 high). Fall from 1.4667 could be the third leg of the corrective pattern from 1.4689. Deeper fall is expected to 61.8% retracement at 1.3056 and possibly below. This will now remain the favored case as long as 1.3855 support turned resistance holds. However, sustained break of 1.3855 will turn focus back to 1.4689 key resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Jun | 0.20% | 0.20% | 0.20% | |

| 8:00 | EUR | Eurozone Private Loans Y/Y May | 3.20% | 3.00% | ||

| 8:00 | EUR | Eurozone M3 Money Supply Y/Y May | 8.50% | 8.30% | ||

| 12:30 | USD | Personal Income M/M May | -6.00% | 10.50% | ||

| 12:30 | USD | Personal Spending May | 9.00% | -13.60% | ||

| 12:30 | USD | PCE Price Index M/M May | -0.50% | |||

| 12:30 | USD | PCE Price Index Y/Y May | 0.50% | |||

| 12:30 | USD | Core PCE Price Index M/M May | 0.00% | -0.40% | ||

| 12:30 | USD | Core PCE Price Index Y/Y May | 0.90% | 1.00% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun F | 79 | 78.9 |