{kind=link}

The forex markets open the week in quiet mode, which Asian stocks are mixed. Australian and New Zealand Dollars are mildly higher. Dollar, Yen and Canadian are softer. But major pairs and crosses are generally stuck inside Friday’s range. The economic calendar is rather light today. Traders could probably wait for the wave of PMI data to featured on Tuesday before taking a move.

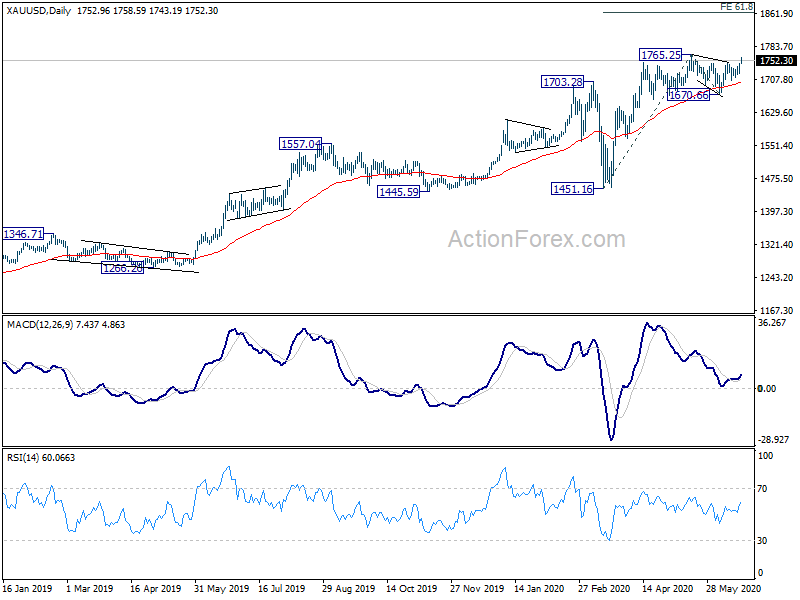

Technically, Gold’s rally is a point to note today as it’s now heading to 1765.25 resistance. Firm break there will resume larger up trend for 61.8% projection of 1451.16 to 1765.25 from 1670.66 at 1864.76. Dollar’s move in accordance will be an interesting point to watch. In particular, USD/JPY remains resilient above 106.57 temporary low so far. But break will resume fall from 109.85 to 105.98 support next.

In Asia, Nikkei is currently down -0.08%. Hong Kong HSI is down 0.53%. China Shanghai SSE is up 0.30%. Singapore Strait Times is up 0.28%. Japan 10-year JGB yield is up 0.0033 at 0.016.

RBA Lowe: Interest rate to stay at current level for years

RBA Governor Philip Lowe said today that “it’s likely we’re going to see interest rates at their current level for years”. “We do face a world where there’ll be a shadow from the virus for quite a few years,” he added”. “People will be more risk-averse, they won’t want to borrow, in Australia we’re going to have lower population dynamics.”

He also said the 7.1% unemployment in Australia was a “misleading indicator” because many people had already given up looking for jobs. Work hours were also lower than they would want. “We just don’t know what constitutes full employment in terms of an unemployment rate,” he said. “We should be seeking to get to full employment however we define that in terms of unemployment, underemployment and hours worked.”

Regarding the Australian Dollar, he’d “like a lower” one, with “lower unemployment and slightly higher inflation”.

Bundesbank Weidmann: Economic trough is behind, but followed only by a gradual recovery

Germany Bundesbank President Jens Weidmann said the country suffered the “deepest economic slump” in history in the last months. Nevertheless, “the good news is: the trough should be behind us by now, and things are looking up again,” he added. “But the deep slump is being followed only by a comparatively gradual recovery.”

He also hailed that the government was right to act quickly in supporting the economy with stimulus. The image of a frugal nation was wrongly portrayed. “She is not saving for the sake of saving, but so that there is money that can be spent sensibly and in case there are difficult times. And that is precisely the case here,” he noted.

Separately, the Robert Koch Institute (RKI) said the estimate 4-day R-value of coronavirus jumped to 2.88 on Sunday. That’s a sharp increase from 1.06 on Friday. It’s also back at the level since early March. The number means that out of 100 people who contracted the coronavirus, a further 288 other people will get infected. To keep the pandemic under control, the R-value needs to be kept below 1. The surge in R-value indicates the risk of a second wave in Germany.

Global PMIs to show relative strength of economic recovery

PMI data from Australia, Japan, Eurozone, UK, and US will provide much insight into the momentum, and relative strength, of upcoming economic recovery. Sentiment indicators like Germany Ifo business climate will also be watched. Additionally, US will release durable goods orders, trade balance, personal income and spending as well ass PCE inflation.

RBNZ rate decision is the only central bank feature this week. It’s widely expected to keep OCR at 0.25%. The central bank should welcome the country’s success in containing coronavirus. The economy is also starting to improve as lockdown exit is in progress. Yet, RBNZ would remain cautious regarding the outlook and keep the door open for further easing. Though, it’s been clearly communicated that negative rate is an option only for next year, not for now.

Suggested reading – RBNZ Preview: Cautiously Optimistic about Recovery while Pledges to Do More if Needed

Here are some highlights for the week:

- Monday: Eurozone consumer confidence; CBI industrial orders expectations, US existing home sales.

- Tuesday. Australia CBA PMIs; Japan PMI manufacturing; Eurozone PMIs; UK PMIs; US PMIs, new home sales.

- Wednesday: RBNZ rate decision; Germany Ifo business climate; US house price index.

- Thursday: New Zealand trade balance; Japan all industry index; Germany Gfk consumer climate; US Q1 GDP final, durable goods orders, jobless claims, goods trade balance, wholesale inventories.

- Friday: Japan Tokyo CPI; Germany import prices, Eurozone M3 money supply; US personal income and spending.

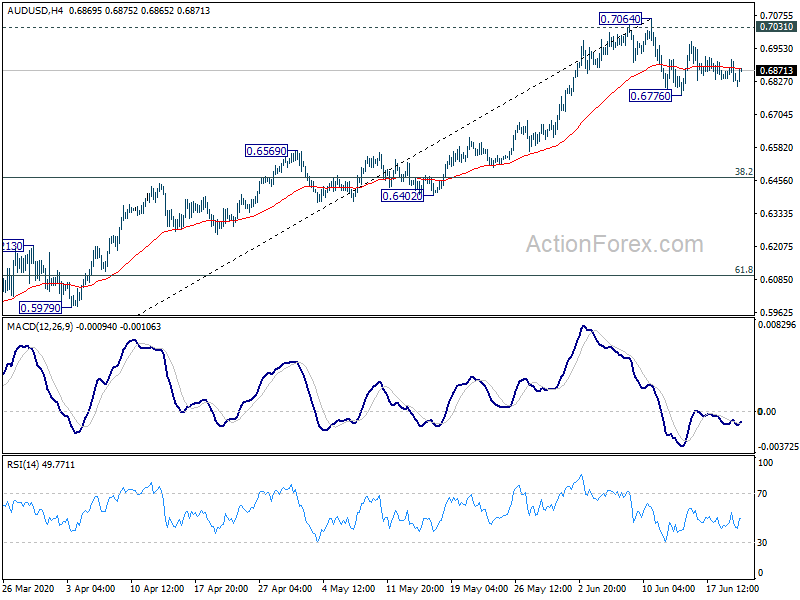

AUD/USD Daily Report

Daily Pivots: (S1) 0.6807; (P) 0.6859; (R1) 0.6888; More…

Intraday bias in AUD/USD remains neutral for the moment. We’d still expect correction from 0.7064 short term top to extend with another decline. Break of 0.6776 will target 38.2% retracement of 0.5506 to 0.7064 at 0.6469. Nevertheless, sustained break of 0.7064 will resume whole rise from 0.5506 instead.

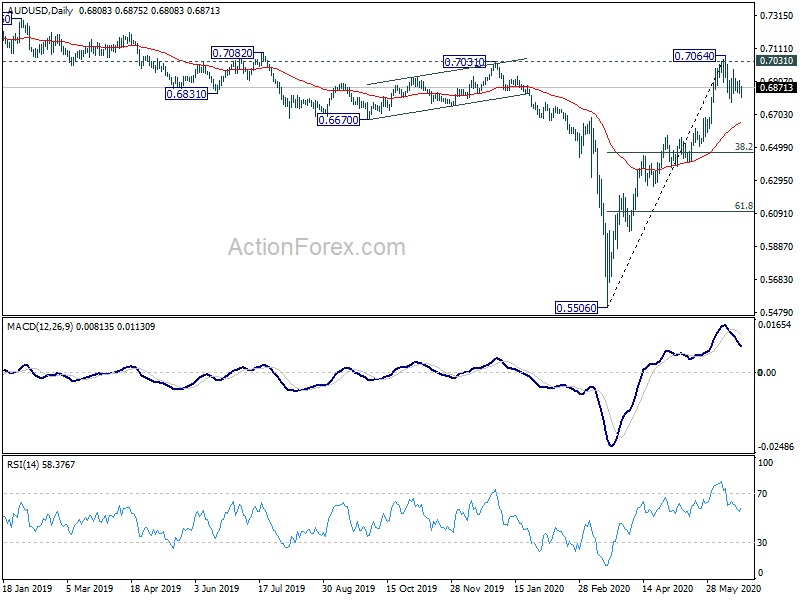

In the bigger picture, rebound from 0.5506 medium term bottom could be correcting whole long term down trend form 1.1079 (2011 high). Further rally would be seen to 55 month EMA (now at 0.7340). This will remain the preferred case as long as it stays above 55 week EMA (now at 0.6727). Sustained trading below 55 week EMA will turn focus back to 0.5506 low instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 10:00 | GBP | CBI Industrial Order Expectations Jun | -59 | -62 | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jun P | -15 | -18.8 | ||

| 14:00 | USD | Existing Home Sales May | 4.20M | 4.33M |