{kind=link}

The forex markets continue to be lacking a clear direction for now. New Zealand and Australian Dollar are mildly softer today, following weaker than expected data. But losses are so far limited. Yen, Euro and Dollar strengthen mildly but there is also no follow through buying. Focus will turn to SNB and BoE monetary policy decisions today. In particular, BoE is widely expected to expand asset purchases, and could hint on more easing ahead.

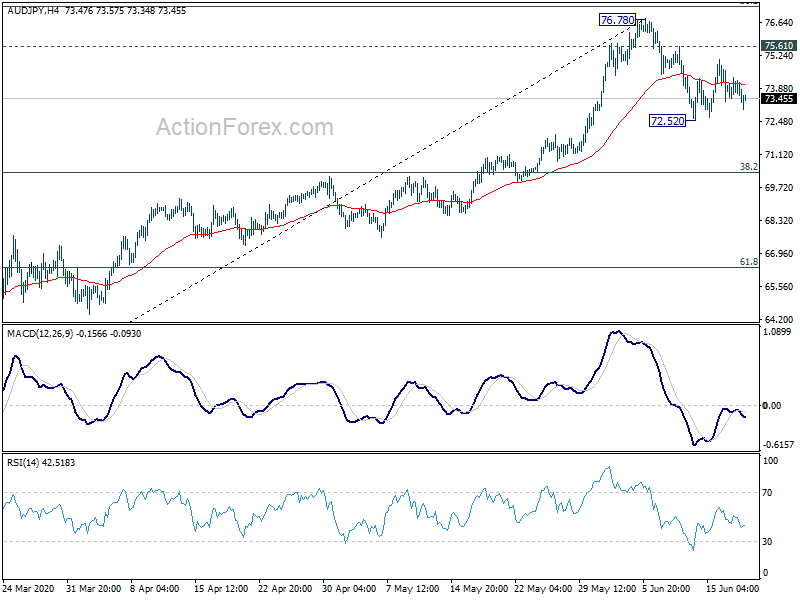

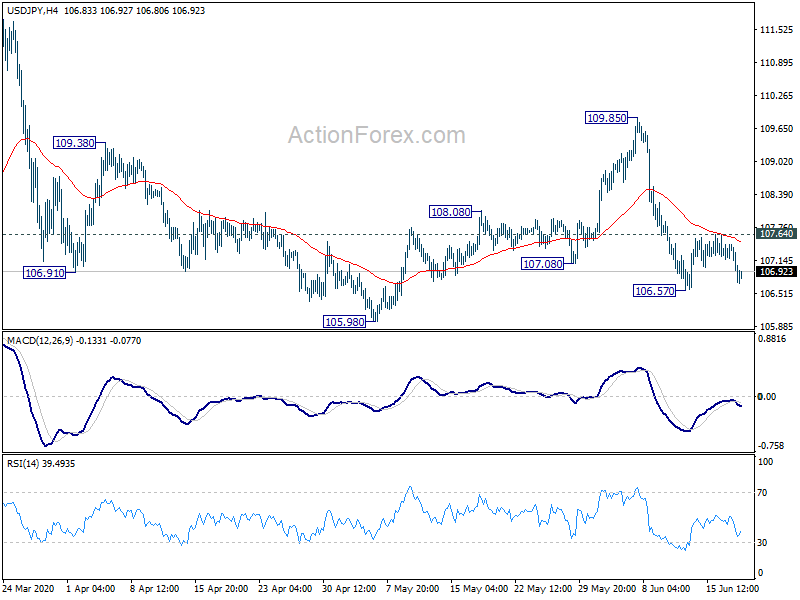

Technically, Yen is showing some sign of strength but more effective is needed. EUR/JPY’s break of 120.25 suggests resumption of the decline from 124.43. Deeper fall is in favor to next fibonacci level at 118.24. But other yen pairs are still range bound. Focuses will be on 106.57 temporary low in USD/JPY, 133.50 in GBP/JPY, 72.52 in AUD/JPY and 78.02 in CAD/JPY. These levels need to be taken out firmly to solidify for case for more Yen rally.

In Asia, Nikkei closed down -0.45%. Hong Kong HSI is down -0.60%. China Shanghai SSE is down -0.03%. Singapore Strait Times is down -0.12%. Japan 10-year JGB yield is down -0.0102 at 0.011. Overnight, DOW dropped -0.65%. S&P 500 dropped -0.36%. NASDAQ rose 0.15%. 10-year yield dropped -0.023 to 0.733.

BoE to keep bank rate unchanged and expand asset purchases

BoE is widely expected to expand stimulus today, through expansion of the quantitative easing program. The asset purchase target would be increased by GBP 100B to GBP 745B. There are some expectations of further increase later in the second half of the year. Bank rate would be held unchanged at 0.10%. BoE officials have ruled out negative interest rate for the near term. As Chief economist Andy Haldane suggested, BoE is “not remotely closed” to negative rates. Though, discussions will likely be carried out on the topic.

Suggested readings on BoE:

- BOE to Expand QE and Discuss Negative Rates

- Bank of England to Ramp Up QE as UK GDP Collapses, Brexit Clock Ticking

SNB: Economic and financial conditions for the banking sector deteriorated markedly

SNB rate decision will be a focus in the markets today. It’s widely expected to keep expansionary monetary policy unchanged. Sight deposit rate should be held at -0.75%. It will also reiterate that “negative interest and interventions are necessary to reduce the attractiveness of Swiss franc investments and thus counteract the upward pressure on the currency.”

Ahead of the policy decision, SNB also released the Financial Stability Report today. it’s noted that “economic and financial conditions for the Swiss banking sector deteriorated markedly during the last few months of the reporting period:. The coronavirus pandemic “triggered a significant correction on financial markets and a sharp drop in global economic activity”. Economic and financial outlook “has worsened considerably” and is “subject to unusually high uncertainty”.

Suggested reading on SNB:

Australia employment contracted -227.7k in May, unemployment rate jumped to 7.1%

Australia employment contracted -227.7k in May, nearly double of expectation of -125.0k. After the decline, 12.2m people were employment. Full-time jobs dropped -89.1k to 8.54m. Part-time jobs dropped -138.6k to 3.62m. Unemployment rate rose 0.7% to 7.1%, worse than expectation of 7.0%. That’s also the highest level in 19 years since October 2001. Participation rate also dropped -0.7% to 62.9%.

“The ABS estimates that a combined group of around 2.3 million people – around 1 in 5 employed people – were affected by either job loss between April and May or had less hours than usual for economic reasons in May,” Bjorn Jarvis, head of labour statistics at the ABS said.

New Zealand GDP shrank -1.6% qoq in Q1, biggest impact to be seen in Q2

New Zealand GDP shrank -1.6% qoq in Q1, worst than expectation of -1.0% qoq. That’s also the largest decline in 29% as the initial effects of coronavirus restrictions impacted on economic activity. “The 1.6 percent fall surpassed quarterly falls during the global financial crisis in the late 2000s,” national accounts senior manager Paul Pascoe said. “It is the largest quarterly fall since the 2.4 percent decline in the March 1991 quarter.”

Finance Minister Grant Robertson said “the biggest impact of the global recession and Alert Level 4 public health restrictions will be seen in the current June quarter.” He added, “now, our focus is on protecting jobs and supporting the economy to recover and rebuild through the investments made in Budget 2020 and by the COVID Response and Recovery Fund. By opening up the economy quicker than forecast, we’ve got a head start on our recovery.”

Fed Mester: Will take quite some time for activity and jobs to approach normal

Cleveland Fed President Loretta Mester said in a speech yesterday that she expected to see “an improvement in the second half of the year as the economy reopens”. However, “it will take quite some time for economic activity and job levels to approach more normal levels”. The improvements will also “vary across sectors”. Some industries like travel and leisure and hospitality will “take quite a while longer “.

By the end of 2020, the output level will see be about 6% below its level at the end of last year. Unemployment would be around (% while inflation will remain below the 2% goal “for some time to come”.

She added that it “makes sense” to continue to monitor the economy and to “to remember that there are several different scenarios that could play out, and to stand ready to use all of our tools to mitigate lasting damage and to support the economy’s recovery”.

Later in the day

Canada will release ADP employment, wholesale sales and new housing price index. US will release jobless claims and Philly Fed survey.

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.83; (P) 107.13; (R1) 107.31; More...

USD/JPY dips notably today but stays above 106.57 temporary low. Intraday bias remains neutral first. Further decline is expected as long as 107.64 resistance holds. Break of 106.57 will target 105.98 support and below. In that case, But downside should be contained by 61.8% retracement of 101.18 to 111.71 at 105.20 to bring rebound. On the upside, break of 107.64 will turn bias back to the upside for 109.85 resistance instead.

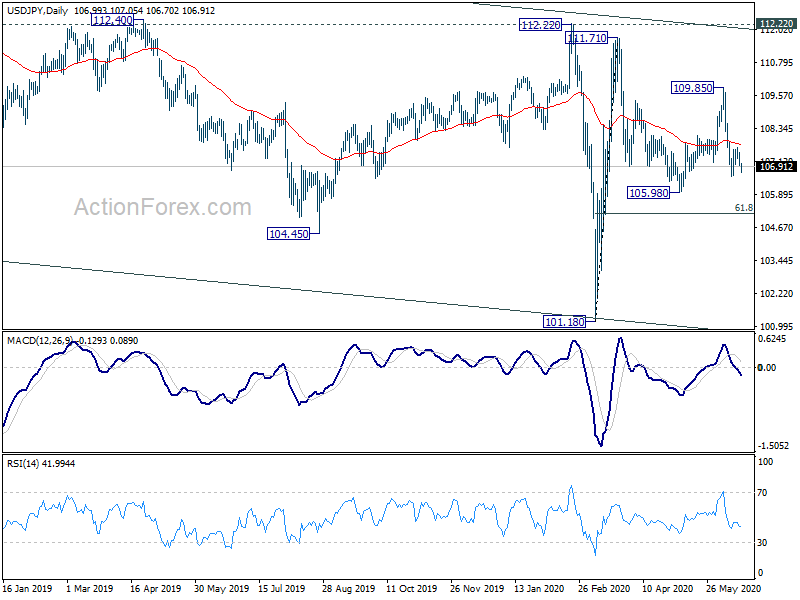

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec2016). Hence, there is no clear indication of trend reversal yet. Break of 105.98 support could extend the down trend through 101.18 low. However, sustained break of 112.22 should confirm completion of the down trend and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | -1.60% | -1.00% | 0.50% | |

| 1:30 | AUD | Employment Change May | -227.7K | -125.0K | -594.3K | -607.4K |

| 1:30 | AUD | Unemployment Rate May | 7.10% | 7.00% | 6.20% | 6.40% |

| 1:30 | AUD | RBA Bulletin | ||||

| 6:00 | CHF | Trade Balance (CHF) May | 2.80B | 4.04B | ||

| 7:30 | CHF | SNB Interest Rate Decision | -0.75% | -0.75% | ||

| 8:00 | EUR | Italy Trade Balance (EUR) Apr | 5.69B | |||

| 8:00 | EUR | ECB Monthly Bulletin | ||||

| 11:00 | GBP | BoE Interest Rate Decision | 0.10% | 0.10% | ||

| 11:00 | GBP | BoE Asset Purchase Facility | 745B | 645B | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 0-0–9 | 0–0–9 | ||

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0–9–0 | 2–0–7 | ||

| 12:30 | CAD | ADP Employment Change May | -226.7K | |||

| 12:30 | CAD | Wholesale Sales M/M Apr | -10.60% | -2.20% | ||

| 12:30 | CAD | New Housing Price Index M/M May | 0.20% | 0.00% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 12) | 1300K | 1542K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jun | -22.7 | -43.1 | ||

| 14:30 | USD | Natural Gas Storage | 93B |