{kind=link}

Asian markets open the week mildly lower on concerns of another coronavirus outbreak in Beijing. Meanwhile, disappointing economic data from China also weigh on sentiments. Yen, Swiss Franc and Dollar are trading generally higher. Aussie is leading commodity currencies lower. But major pairs and crosses are staying inside Friday’s range. Breakout is awaited, probably not until European markets open.

Technically, a main focus this week is whether concerns over second wave of coronavirus pandemic would solidify risk reversals. If that happens, which on of Dollar, Yen and Swiss Franc would outperform. USD/CHF’s correction from 0.9901 could have completed at 0.9376 with Friday’s rebound. Sustained trading above 4 hour 55 EMA (now at 0.9533) would solidify this case and turn near term outlook bullish. USD/JPY’s recovery on Friday was relatively weaker. Further fall remains mildly in favor and break of 106.57 temporary low will extend the corrective pattern fro1 117.71 for 105.98 support and below.

In Asia, Nikkei is currently down -0.55%. Hong Kong HSI is down -0.86%. China Shanghai SSE is down -0.09%. Singapore Strait Times is down -1.55%. Japan 10-year JGB yield is down -0.0018 at 0.015.

China industrial production continues to rebound while retail sales shrink

Released from China, industrial production grew 4.4% yoy in May, accelerated from April’s 3.9% yoy, but missed expectation of 5.0% yoy. Retail sales’s contraction slowed to -2.8% yoy, up from April’s -5.7% yoy, and missed expectation of -2.0% yoy. Fixed asset investment dropped -6.3% ytd yoy, missed expectation of -5.9% ytd yoy too.

Outlook of China’s economy is clouded by the resurgence of coronavirus risk in its capital city. Beijing reported a cluster of new coronavirus cases linked to its biggest wholesale food markets overnight weekend, which is now shutdown. Authorities in Beijing locked down 11 residential communities near the Xinfadi market. Additionally, the China Southern Airlines was required to suspend flights between Dhaka, Bangladesh, and the southern city of Guangzhou for four weeks.

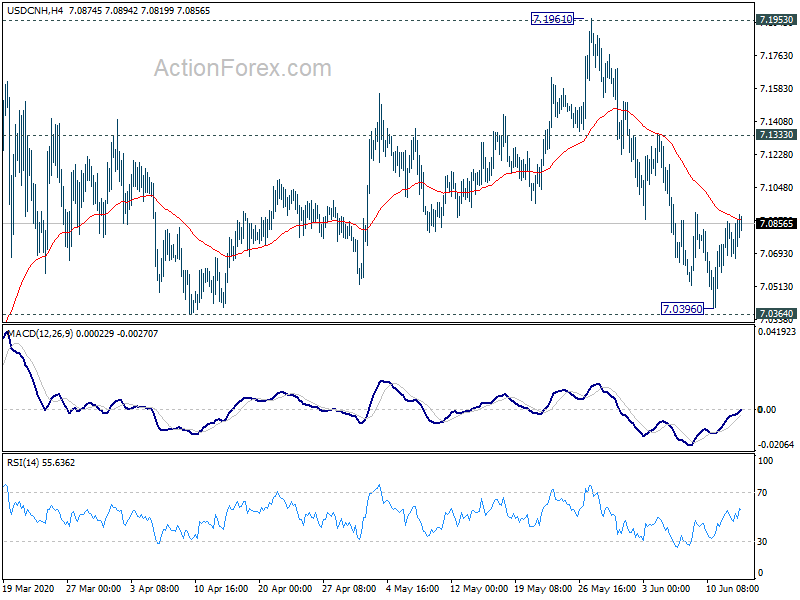

USD/CNH recovered after dipping to 7.0396 last week, ahead of 7.0364 support. Further decline is still expected as long as 7.1333 resistance holds. we’re seeing fall form 7.1961 as the third leg of the consolidation pattern from 7.1953. Sustained break of 7.0364 support would pave the way to retest 6.8452 next.

Fed Kaplan expects positive job growth from here

Fed Kaplan expects positive job growth from here

Dallas Fed President Robert Kaplan said the US is “on our way down right now” with unemployment. “We’re going to get positive job growth in June, July and from here,” he added. However, “even with that growth, we’re going to end the year with an elevated unemployment rate.” He expected unemployment rate to end 2020 at 8% or above.

Kaplan also urged that it’s “critical” for people to “widely” wear masks, with good coronavirus testing and contract tracing implemented in the society. “The extent we do that well will determine how quickly we recover. We’ll grow faster if we do those things well,” he said. “And right now, it’s relatively uneven.”

UK Johnson to seek high quality FTA by Autumn at high level talks with EU

A “high-level” meeting on Brexit is scheduled for today, involving top officials from UK and EU. But expectations are relatively low regarding the meeting. It’s reported that UK Prime Minister Boris Johnson would push for a post Brexit agreement by Autumn at the latest. He would demand a high quality FTA that is consistent with what EU have agreed with others. Meanwhile, he would also insist on not seeking an extension to the transition period, and leave the EU on December 31.

Last Friday, the UK government laid out a three-phased plan for Brexit border checks. Full border controls on goods entering the UK will not be implemented until July 2021. Duchy of Lancaster, Michael Gove also noted that “”We have informed the EU today that we will not extend the transition period. The moment for extension has now passed.”

BoE to expand asset purchase, BoJ and SNB to stand pat

Three central banks will meet this week. BoJ is not expected to take any fresh stimulus action for now. But there might be some adjustment in the outlook and the statement, as well as some lending programs. SNB is also expected to stand pat for now, and reiterate the need for negative interest rate and currency intervention.

BoE is the bigger focus this week. While officials have basically ruled out negative rates for the near term, given the sharp -20.4% mom GDP contraction recorded in April, there is a need to boost stimulus. BoE could opt for expanding the asset purchase program by another GBP 100B.

Fed Chair Jerome Powell will testify before Congress but he’s not expected to deliver anything different from the post FOMC press conference last week. He is expected to reiterate that interest rate will stay near zero for a prolonged period, and negative rate is not suitable for the US. Though, he may share more of his views regarding yield curve control.

The economic data schedule is rather busy this week too. Here are some highlights:

- Monday: China industrial production, retail sales, fixed asset investment; Japan tertiary industry index; Swiss PPI; Eurozone trade balance; Canada manufacturing sales; US Empire state manufacturing.

- Tuesday: RBA minutes, Australia house price index; BoJ rate decision; Germany CPI final; UK employment; Germany ZEW economic sentiment; US retail sales, industrial production, business inventories, NAHB housing index.

- Wednesday: New Zealand current account; Japan trade balance; UK CPI, PPI; Eurozone CPI final; Canada CPI; US housing starts and building permits.

- Thursday: New Zealand GDP; Australia employment, RBA bulletin; Swiss trade balance, SNB rate decision; ECB monthly bulletin; BoE rate decision; Canada ADP employment, new housing price index, wholesale sales; US Philly Fed survey, jobless claims.

- Friday: Japan national CPI core; BoJ minutes; Australia retail sales; UK retail sales, public sector net borrowing; Eurozone current account; Canada retail sales; US current account.

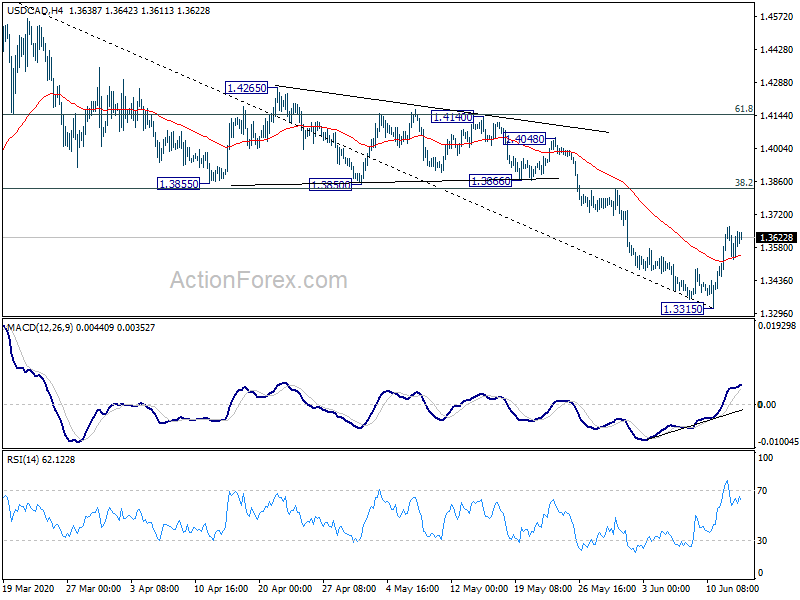

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3519; (P) 1.3593; (R1) 1.3658; More….

Intraday bias in USD/CAD remains mildly on the upside at this point. Rebound from 1.3315 short term bottom would target 38.2% retracement of 1.4667 to 1.3315 at 1.3831 first. Firm break there will target 61.8% retracement at 1.4151. On the downside, break of 1.3315 is now needed to confirm resumption of fall from 1.4667. Otherwise, risk will stay mildly on the upside in case of retreat.

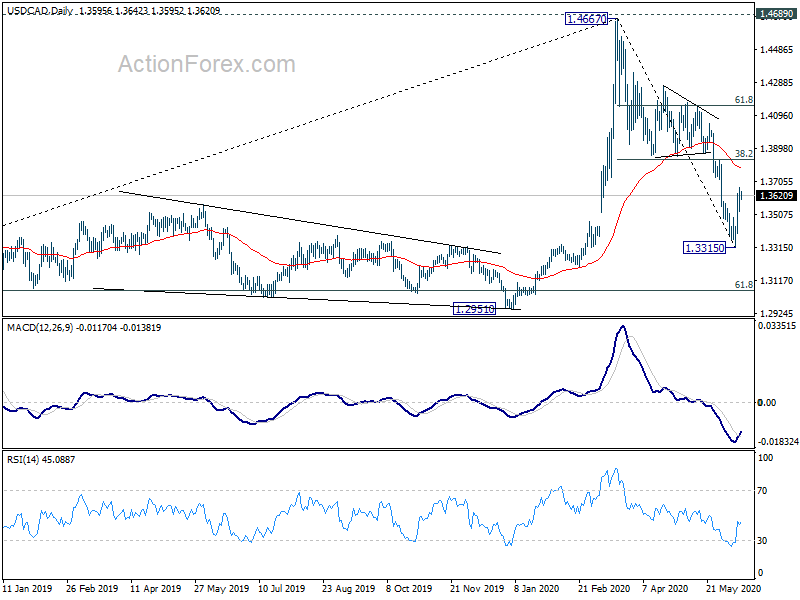

In the bigger picture, the rise from 1.2061 (2017 low) could have completed at 1.4667 after failing 1.4689 (2016 high). Fall from 1.4667 could be the third leg of the corrective pattern from 1.4689. Deeper fall is expected to 61.8% retracement at 1.3056 and possibly below. This will now remain the favored case as long as 1.3855 support turned resistance holds. However, sustained break of 1.3855 will turn focus back to 1.4689 key resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | CNY | Retail Sales Y/Y May | -2.80% | -2.00% | -7.50% | |

| 02:00 | CNY | Industrial Production Y/Y May | 4.40% | 5.00% | 3.90% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y May | -6.30% | -5.90% | -10.30% | |

| 04:30 | JPY | Tertiary Industry Index M/M Apr | -7.50% | -4.20% | ||

| 06:30 | CHF | Producer and Import Prices M/M May | -0.90% | -1.30% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y May | -4.60% | -4.00% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | 20.3B | 23.5B | ||

| 12:30 | USD | Empire State Manufacturing Index Jun | -30 | -48.5 | ||

| 12:30 | CAD | Manufacturing Sales M/M Apr | -5.70% | -9.20% |