{kind=link}

Dollar is trading a touch softer in early US session after poor durable goods orders. Euro, on the other hand, is trying to extend the EU stimulus triggered gains. Overall, movements in the forex markets today are relatively limited. Yen and the greenback remain the weakest for the week while commodity currencies are strongest. Directions in other markets are also relatively unclear with US stocks opening higher but DOW struggles to extend rally through 25750 handle.

Technically, Euro’s rally will continue to be a focus, with attention on 0.9000 resistance in EUR/GBP, 1.6763 resistance in EUR/AUD and 1.5142 resistance in EUR/CAD. EUR/USD is still some way below key near term fibonacci resistance at 1.1167, and thus, there is room for more upside.

In Europe, currently, FTSE is up 1.12%. DAX is up 0.73%. CAC is up 1.29%. German 10-yaer yield is down -0.0053 at -0.417. Earlier in Asia, Nikkei rose 2.32%. Hong Kong HSI dropped -0.72%. China Shanghai SSE rose 0.33%. Singapore Strait Times dropped -0.17%. Japan 10-year JGB yield dropped -0.0031 to -0.001.

US initial jobless claims dropped to 2.1m, durable orders dropped -17.2%

US initial jobless claims continued to drop, by -323k to 2123k in the week ending May 23. Four-week moving average of initial claims dropped -436k to 2608k. Continuing claims dropped -3860k to 21052k in the week ending May 16. Four-week moving average of continuing claims rose 765.25k to 22722k.

Durable goods orders dropped -17.2% to USD 170.0B in April, better than expectation of -18.1%. That’s still the second month of sharp decline, following -16.6% in March. Ex-transport orders dropped -7.4%. Ex-defense orders dropped -16.2%.

According to second estimate, GDP contracted -5.0% annualized in Q1, worse than first estimate of-4.8% annualized. A downward revision to private inventory investment was partly offset by upward revisions to personal consumption expenditures (PCE) and nonresidential fixed investment. PCE price index was unrevised at 1.3% yoy. PCE core price index was revised down to 1.6% yoy, down from 1.8% yoy.

Pending home sales dropped -21.8% mom in April, worse than expectation of -15.0% mom.

BoE Saunders: Safer to err on the side of easing somewhat too much

BoE policymaker Michael Saunders, a known dove, warned of the risks of a “vicious circle whereby the economy gets stuck in a self-feeding loop of weak activity, pessimistic expectations and low investment.”

“The searing experience of such a dramatic drop in incomes, jobs and profits is likely to have lasting behavioural effects, as after previous crises,” he said.

He maintained he dovish stance and urged,

“it is safer to err on the side of easing somewhat too much, and then if necessary tighten as capacity pressures eventually build, rather than ease too little and find the economy gets stuck in a low inflation rut.”

Ifo: Germany business think they will most likely return to normal in nine months

Ifo updated their German economic forecasts and now expects GDP to shrink by -6.6% this year. A strong rebound of 10.2% GDP growth is expected in 2021. “This is based on our evaluation of the ifo survey conducted among companies in May. On average, participants consider it most likely that their own business situation will return to normal in nine months,” says Timo Wollmershaeuser, Head of Forecasts at ifo.

The forecast depends heavily on how quickly companies’ business situation returns to normal. In the best case, companies indicate that this might take an average of only five months. GDP could shrink only -3.9% this year and grow 7.4% next.

In the worst case, with an average normalization period of 16 months, economic output would shrink by -9.3% this year and grow by 9.5% next year. The recovery would then be drawn out well into 2022.

Also, the new forecast was prepared based on the assumption not that the coronavirus is defeated in the coming months, but that its spread can be contained and a second wave of infection avoided.

Eurozone economic sentiment rose slgihtly to 67.5, employment expectations jumped

Eurozone Economic Sentiment Indicator rose slightly to 67.5 in May, up from 64.9, but missed expectations of 70.5. Employment Expectations Indicator led the way, jumped to 70.2, up from 58.9. Industrial Confidence rose to -27.5, up from -32.5. Consumer Confidence rose to -18.8, up from -22.0. Retail Trade Confidence rose slightly to -29.7, up from -30.1. On the other hand, Services Confidence dropped to -43.6, down from -38.6. Construction Confidence dropped to -17.4, down from -16.1. Business Climate dropped to -2.43, down from -18.1.

From Germany, CPI came in at -0.1% mom, 0.6% yoy in May, matched expcetations.

RBA Lowe: Economy better than baseline, negative rates extraordinarily unlikely

RBA Governor Philip Lowe said that the economy could be “better than the baseline” scenario as forecast earlier this month. RBA projected that GDP could contract by -6% this year with unemployment rise to 9%. “With the national health outcomes better than earlier feared, it is possible that the economic downturn will not be as severe as earlier thought. Much depends on how quickly confidence can be restored,” he added.

Lowe also noted that the monetary stimulus package was working as expected. If we had to do more we could purchase more government bonds. But as things stand at the moment, we don’t see the need to doing more,” he said. He also reiterated negative interest rates were “extraordinarily unlikely”.

Released from Australia, Private capital expenditure dropped -1.5% in Q1, better than expectation of -2.7%.

New Zealand ANZ Business Confidence rose to -41.8, recovery going to be a long haul

New Zealand ANZ Business Confidence improved to -41.8 in May, up from May’s prelim reading of -45.6, and April’s -66.6. All industry stayed negative, worst in Agriculture at -82.1. Activity Outlook improved to -38.7, up from May’s prelim reading of -42.0, and April’s -55.1. Retail activity was worst at -45.3. Also, with the Activity Outlook stayed well below 2008.09 lows, and would “need to rise another 17 points just to reach its lows from the 2009 recession”.

ANZ also noted, “it’s a long way back to normality” while “the recession is just starting to make itself felt”. The economy needs to “reshape to face to the new reality”, in particular, the loss of international tourists “completely for now, but likely still at a hugely significant scale for years”. “Fiscal and monetary policy are doing what they can to cushion the blow and sow the seeds of recovery, but it’s going to be a long haul.”

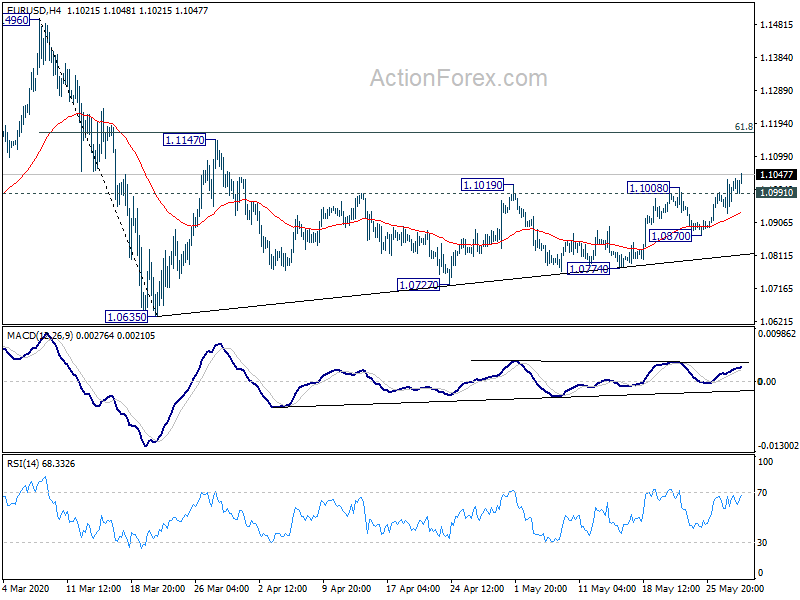

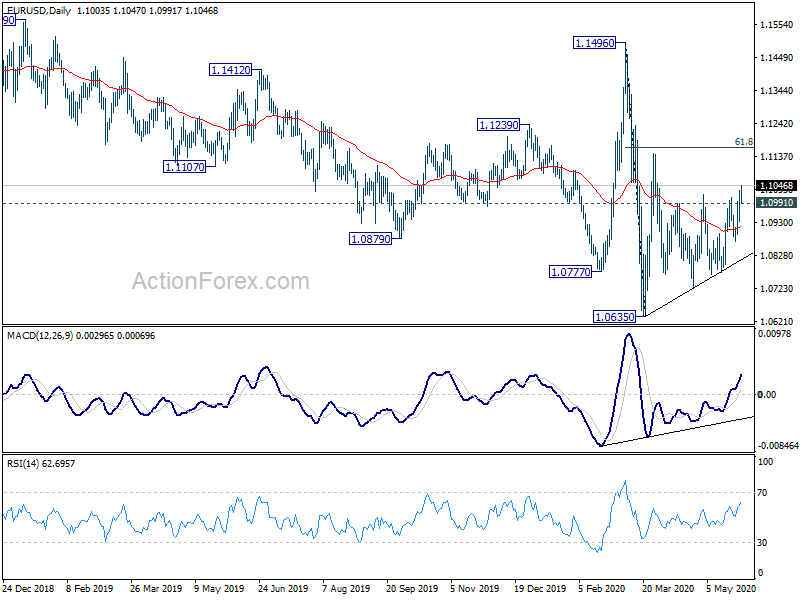

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0951; (P) 1.0991; (R1) 1.1048; More…

EUR/USD’s rally form 1.0774 is still in progress and intraday bias stays on the upside. It’s seen as a rising leg in the consolidation pattern from 1.0635. Next target is 1.1147 resistance. But upside should be limited by 61.8% retracement of 1.1496 to 1.0635 at 1.1167. On the downside, below 1.0991 minor support will turn intraday bias neutral first. Break of 1.0870 will turn bias to the downside for 1.0774 support.

In the bigger picture, as long as 1.1496 resistance holds, whole down trend from 1.2555 (2018 high) should still be in progress. Next target is 1.0339 (2017 low). However, sustained break of 1.1496 will argue that such down trend has completed. Rise from 1.0635 could then be seen as the third leg of the pattern from 1.0339. In this case, outlook will be turned bullish for retesting 1.2555.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence May | -41.8 | -45.6 | ||

| 01:30 | AUD | Private Capital Expenditure Q1 | -1.50% | -2.70% | -2.80% | -2.60% |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator May | 67.5 | 70.5 | 67 | 64.9 |

| 09:00 | EUR | Eurozone Industrial Confidence May | -27.5 | -25.4 | -30.4 | -32.5 |

| 09:00 | EUR | Eurozone Services Sentiment May | -43.6 | -28.4 | -35 | -38.6 |

| 09:00 | EUR | Eurozone Consumer Confidence May | -18.8 | -18.8 | -18.8 | -22 |

| 09:00 | EUR | Eurozone Business Climate May | -2.43 | -1.81 | -1.99 | |

| 12:00 | EUR | Germany CPI M/M May P | -0.10% | -0.10% | 0.40% | |

| 12:00 | EUR | Germany CPI Y/Y May P | 0.60% | 0.60% | 0.90% | |

| 12:30 | CAD | Current Account (CAD) Q1 | -11.1B | -10.2B | -8.8B | -9.3B |

| 12:30 | USD | Initial Jobless Claims (May 22) | 2123K | 2438K | 2446K | |

| 12:30 | USD | GDP Annualized Q1 P | -5.00% | -4.80% | -4.80% | |

| 12:30 | USD | GDP Price Index Q1 P | 1.40% | 1.30% | ||

| 12:30 | USD | Durable Goods Orders Apr | -17.20% | -18.10% | -15.30% | -16.60% |

| 12:30 | USD | Durable Goods Orders ex Transportation Apr | -7.40% | -14.00% | -0.60% | -1.70% |

| 14:00 | USD | Pending Home Sales M/M Apr | -21.80% | -15.00% | -20.80% | |

| 14:30 | USD | Natural Gas Storage | 113B | 81B | ||

| 15:00 | USD | Crude Oil Inventories | -2.5M | -5.0M |