{kind=link}

Asian markets are relatively mixed in quiet trading as another week starts. Hong Kong stocks dip mildly following Sunday’s protests against the national security laws. But some optimism is seen in Japan with Nikkei’s rise. Movements in the stock indices are limited anyway. Sterling is trading mildly higher, followed by Canadian and then Aussie. Euro, Swiss and Yen are the weaker ones. But major pairs and crosses are generally bounded inside Friday’s range. Trading might continue to be subdued with UK and US on bank holiday today.

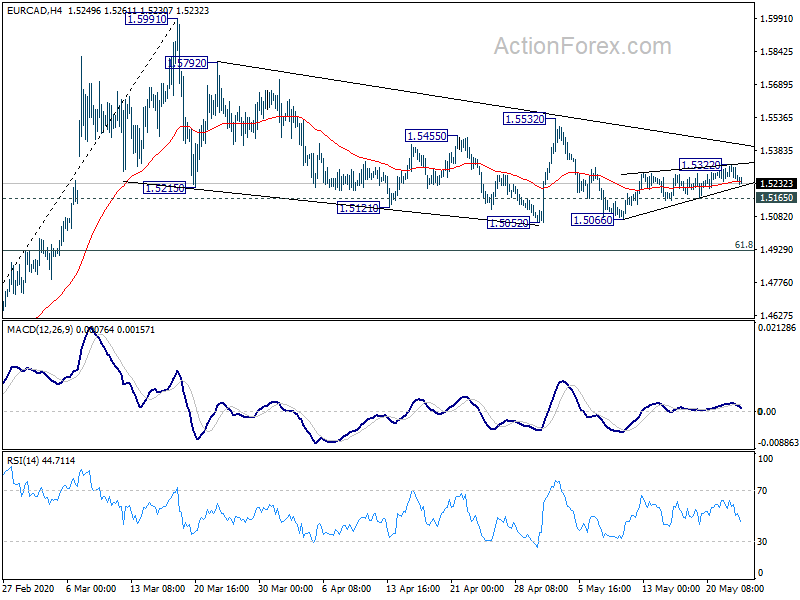

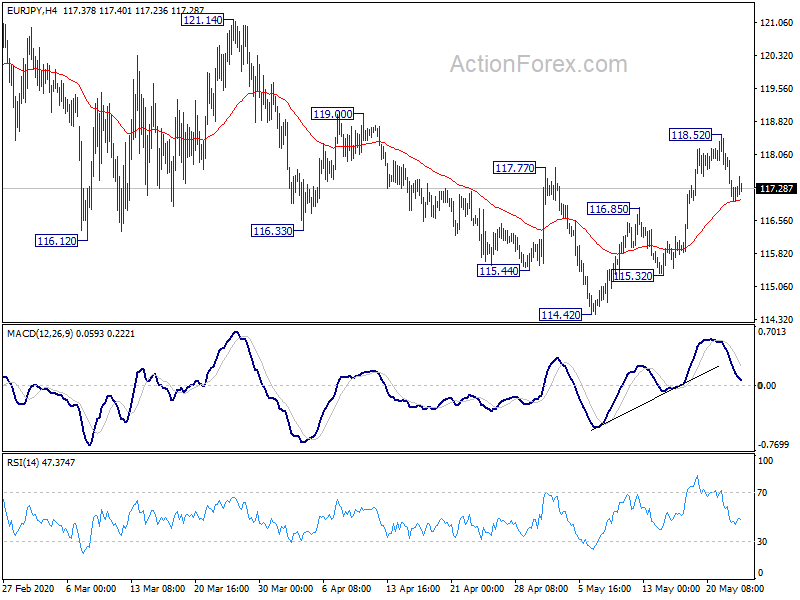

Technically, Euro might be a focus for today as EUR/USD, EUR/JPY and EUR/CAD are all struggling around 4 hour 55 EMA. Sustained trading below these levels could prompt some more downside for the common currency. In particular, EUR/CAD’s recovery from 1.0566 is clearly corrective in nature. Sustained trading below the 4 hour 55 EMA (now at 1.5242) will suggest that it’s completed at 1.5322 already. Further fall could be seen to 1.5165 minor support for confirmation, and then retest of 1.5052/5066 support zone.

In Asia, currently, Nikkei is up 1.45. Hong Kong HSI is down -1.0%. China Shanghai SSE is down -0.03%. Singapore market is closed. Japan 10-year JGB yield is up 0.0072 at 0.001.

EU Centeno: Franco-German recovery fund a critical part of larger and coordinated coronavirus response

In an interview with German weekly Welt am Sonntag, Eurogroup head Mario Centeno said that the Franco-German proposal of EUR 500B recovery fund could be a “critical part” in the “larger and coordinated” coronavirus response”. It would “allow us to protest the single market in the recovery phase”. He added that “the German-Franco proposal would be a great step towards a fiscal union and a properly functioning currency union, even if the recovery fund is only temporary.”

He admitted that “we will all come out of this crisis with higher debts”. Hence, it’s important for the Eurogroup to agree on a recovery fund that “spread the costs of the crisis over time”. The France-German initiative was also “one step forward in addressing the debt overload issue by proposing common debt issuance.”

On the economy, Centeno said the forecasts so far do not take into account the EUR 500B reconstruction funds and the frontloaded EU budget. He added, “this enormous stimulus will strongly accelerate economic recovery”. “By the end of 2022, most – if not all – EU countries will return to 2019 GDP levels”.

Australia goods exports dropped -12%, imports dropped -5% in Apr

In April’s preliminary data, Australia’s goods exports dropped -12% mom from March’s record high of AUD 35.8B to AUD 31.4B. The contraction was driven by exports of non-rural goods (down -8% mom) and non-monetary gold (down -47% mom).

Imports dropped -5% mom to AUD 23.1B. The decrease in imports were driven by intermediate and other goods (down -6% mom), non-monetary gold (down -42% mom) and capital goods (down -7% mom).

Fed’s Beige Book, some April and May data to watch

Any news regarding US-China tensions, coronavirus, vaccine and lockdown exits will remain the major market movers this week. Fed’s Beige Book economic report could also reveal more details regarding the economy. On the data front, April and May data are the more important ones.

US consumer confidence, durable goods orders, goods trade balance, PCE inflation; Germany ifo business climate, Gfk consumer sentiment; Eurozone confidence indicators, CPI; Japan industrial production and retail sale are the more important ones to watch.

Here are some highlights for the week:

- Monday: Germany GDP final, Ifo business climate.

- Tuesday: New Zealand trade balance, Japan SPPI, all industry index; Swiss trade balance; Germany Gfk consumer sentiment; UK CBI realized sales; US house price index, new homes sales, consumer confidence.

- Wednesday: Australia construction work done; Fed’s Beige Book report.

- Thursday: New Zealand ANZ business confidence; Australia private capital expenditure; Germany CPI; Canada current account; US GDP revision, durable goods orders, jobless claims, pending home sales.

- Friday: Japan Tokyo CPI, unemployment rate, industrial production, retail sales, consumer confidence, housing starts; Australia private sector credit; Germany import price, retail sales; Swiss KOF economic barometer; Eurozone M3, CPI; Canada GDP, RMPI and IPPI; US personal income and spending, goods trade balance, wholesale inventories, Chicago PMI.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 116.89; (P) 117.44; (R1) 117.87; More…..

Intraday bias in EUR/JPY remains neutral at this point and further rise is mildly in favor. On the upside, break of 118.52 will resume the rebound from 114.42 and target 121.14 resistance next. However, break of 116.85 resistance turned support, and sustained trading below 4 hour 55 EMA (now at 117.03), will argue the rebound has completed. Intraday bias will be turned back to the downside for 115.32 support for confirmation.

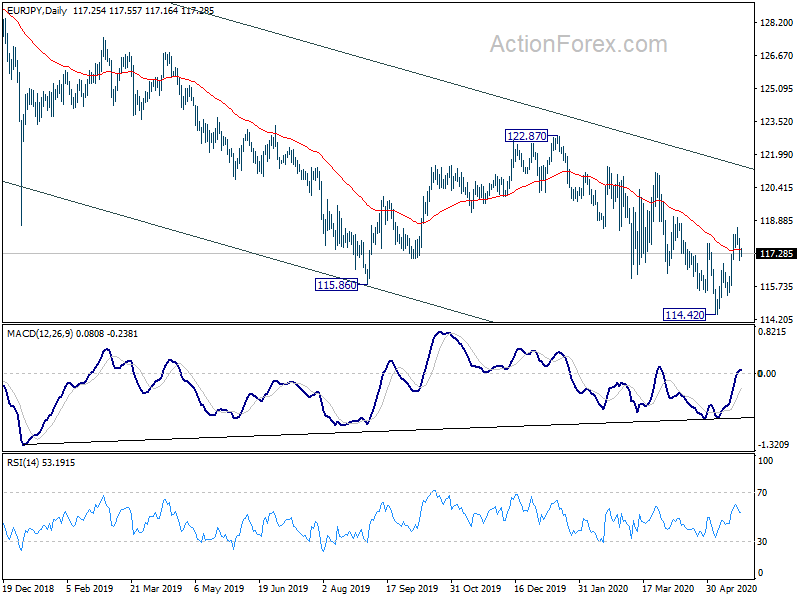

In the bigger picture, there is no clear sign of trend reversal yet. EUR/JPY is staying well inside falling channel and below falling 55 week EMA. Deeper fall could be seen to retest 109.48 (2016 low) next. On the upside, break of 122.87 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany GDP Q/Q Q1 F | -2.20% | -2.20% | ||

| 08:00 | EUR | Germany IFO – Business Climate May | 78.8 | 74.3 | ||

| 08:00 | EUR | Germany IFO – Current Assessment May | 81.9 | 79.5 | ||

| 08:00 | EUR | Germany IFO – Expectations May | 75 | 69.4 |