{kind=link}

The financial markets are, generally speaking, a bit mixed today. European stocks are slightly in red while US futures are down. But losses are very limited. Bulls are still in overwhelming control. In the currency markets, Swiss Franc drops sharply as recent volatile trading continues. Dollar attempted for a rebound earlier today but quickly lost steam. Commodity currencies are engaging in consolidations, awaiting next move in the risk markets.

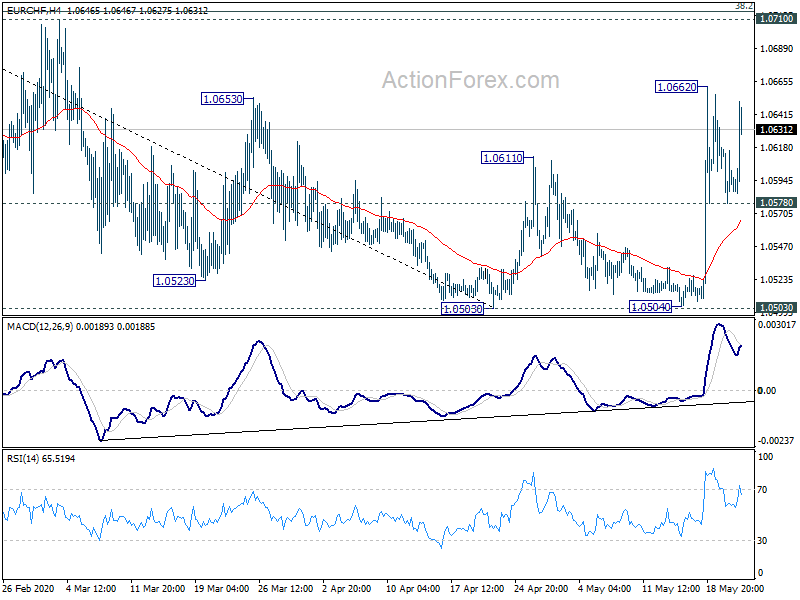

Technically, EUR/CHF rebounds strongly after drawing support from 1.0578 minor support. near term outlook stays cautiously bullish and break of 1.0662 resistance will target 1.0710 cluster resistance zone.

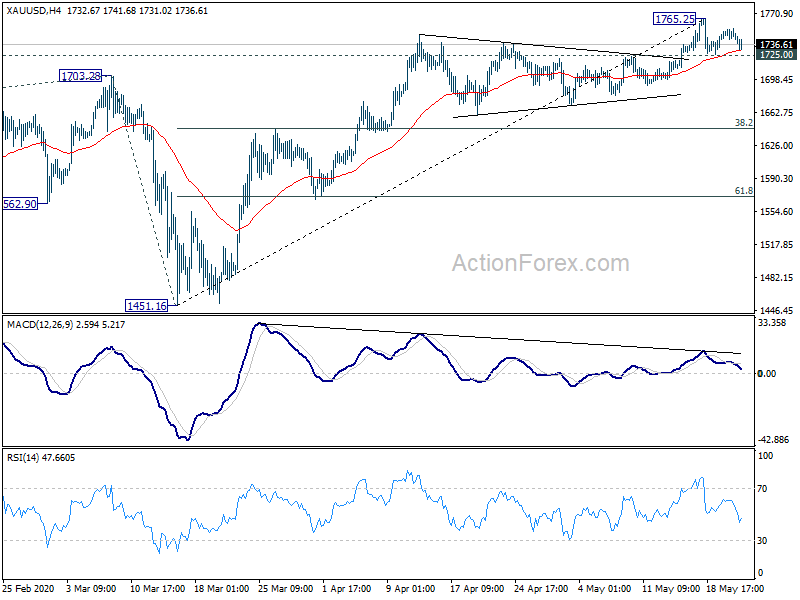

Gold’s recovery lost momentum after hitting 1753.81 and weakens again. We’re favoring the case that price actions from 1765.25 would eventually correct whole rise from 1451.16. Break of 1725.00 minor support will affirm our view and target 38.2% retracement of 1451.16 to 1765.25 at 1645.26.

In Europe, currently, FTSE is down -0.39%. DAX is down -0.98%. CAC is down -0.77%. German 10-year yield is down -0.021 at -0.486. Earlier in Asia, Nikkei dropped -0.21%. Hong Kong HSI dropped -0.49%. China Shanghai SSE dropped -0.55%. Singapore Strait Times dropped -0.26%. Japan 10-year JGB yield dropped -0.0023 to 0.000.

US initial jobless claims dropped to 2.4m, continuing claims rose to 25m

US initial jobless claims dropped -249k to 2438k in the week ending May 16. Four-week moving average of initial claims dropped -501k to 3042k. Continuing claims rose 2525k to 25073k in the week ending May 9. Four-week moving average of continuing claims rose 2314k to 22002k.

Philadelphia Fed Manufacturing Business Outlook rose to -43.1 in May, up from April’s 40-year low of -56.6. 58% of firms reported decreasing activity versus 15% which reported increase.

From Canada, ADP employment dropped -226.7k in April. New Housing price index rose 0.0% mom in April.

UK PMI composite rose to 28.9, looks set to see a frustratingly slow recovery

UK PMI Manufacturing rose to 40.6 in May, up from 32.6, above expectation of 33.5. PMI Services rose to 27.8, up from 13.4, above expectation of 22.1 too. PMI Composite rose to 28.9, up from 13.8.

Chris Williamson, Chief Business Economist at IHS Markit, said: “The UK looks set to see a frustratingly slow recovery, given the likely slower pace of opening up the economy relative to other countries which have seen fewer COVID-19 cases. Virus related restrictions, widespread job insecurity and weak demand will be exacerbated by growing business uncertainty regarding Brexit. We are consequently expecting GDP to fall by almost 12% in 2020. While the quarterly rate of decline looks likely to peak at around 20% in the second quarter, the recovery will be measured in years not months.”

Eurozone PMI composite rose to 30.5, still point to -10% Q2 GDP contraction

Eurozone PMI Manufacturing rose to 35.4, up from 18.1, below expectation of 38.0. PMI Services rose to 28.7, up from 12.0, above expectation of 23.9. PMI Composite rose to 30.5, up from 13.6.

Chris Williamson, Chief Business Economist at IHS Markit said: “Second quarter GDP is still likely to fall at an unprecedented rate, down by around 10% compared to the first quarter, but the rise in the PMI adds to expectations that the downturn should continue to moderate as lockdown restrictions are further lifted heading into the summer.”

“An additional concern is that demand is likely to remain extremely weak for a prolonged period, putting further pressure on companies to make more aggressive job cuts as government job retention schemes expire. We therefore expect GDP to slump by almost 9% in 2020 and for a full recovery to take several years.”

Germany PMI Manufacturing rose to 36.8 in May, up from 34.5, but missed expectation of 40.0. PMI Services rebounded strongly to 31.4, up from 16.2, beat expectation of 26.0. PMI Composite rose to 31.4, up from 17.4.

France PMI Manufacturing improved to 40.3 in May, up from 31.5, above expectation of 40.3. PMI services rebounded notably to 29.4, up from 10.2, just missed expectation of 30.0. PMI Composite rose to 30.5, up sharply from 11.1.

RBA Lowe: Extraordinarily unlikely to use negative rates

RBA Governor Philip Lowe said together that “restoring confidence on the health front is a precondition for a strong recovery. “We might get a vaccine, we might get some anti-viral medication, but it’s also possible that we don’t. So we have an incredible lot riding on the work of the scientists.”

Looking ahead, “one obvious source of uncertainty is the pace at which the various restrictions are eased. Another source of uncertainty is the level of confidence that people have about their future, both in terms of their health and their own finances.

He added that the central bank was prepared to scale up the bond purchases if necessary. However, it was “extraordinarily unlikely to cut interest rates into negative.

Australia CBA PMI composite recovered to 26.4, May should mark the low point

Australia CBA PMI Composite rose to 26.4 in May, up from 21.7. PMI Services improved from 19.5 to 25.5. However, PMI Manufacturing dropped from 44.1 to 42.8.

CBA Head of Australian Economics, Gareth Aird said: “May should mark the low point in the PMIs and we would expect activity to lift from here on a monthly basis. Company views on the economic outlook have improved and the lift in confidence is welcome. That said, it will be a long time before activity returns to pre-COVID-19 levels. And deflationary pressures highlight the huge amount of slack we have now in the economy.”

RBNZ Ha: Won’t lower OCR until next March since banking system is not ready

New Zealand Dollar is trying to extend this week’s recovery as the chance of RBNZ negative rates is fading. RBNZ chief economist Yuong Ha said in a webinar that he didn’t expect interest rate to be lowered further from the current level of 0.25% this year.

“We expect to hold it there for the next 12 months, until March next year,” he said. “We’re not planning on taking it lower at this stage, simply because the banking system is not ready for lower OCR rates at the moment. We’ve given the banking system until the end of the year to get ready so that the option is there for the Monetary Policy Committee in a year’s time.”

Though, he also noted that the MPC has “the ability to continue to monitor, revise, reassess and re-evaluate our decisions and the effectiveness of our decisions and do whatever it takes to get us back to our medium-term objectives.”

Separately, Westpac also revised their forecast and expect RBNZ to cut OCR to -0.50% in April 2021, rather than November 2020. It said the timing of negative rate “would depend on how long it takes for trading banks to become operationally ready for a negative OCR”. As RBNZ has asked trading banks to ready themselves for negative OCR by December 1 this year, a negative OCT “will be operationally possible from the start of 2021.

Japan exports dropped most in a decade in April

In non seasonally adjusted term, Japan’s export dropped -21.9% yoy in April to JPY 5.2T. That’s the worst decline since 2008. Exports to US dropped a massive -37.8% yoy, worst since 2009. Exports to China dropped -4.1% yoy. Imports dropped -7.2% yoy to JPY 6.1T. Trade surplus came in at JPY 930B. In seasonally adjusted terms, exports dropped -10.4% mom to JPY 5.2T while imports rose 0.2% mom to 6.2T. Trade deficit widened to JPY -1.0T.

Japan PMIs: Potential hit to Q2 could be as large as 20% on previous year

PMI Manufacturing dropped to 31.7 in May, down from 34.7. PMI Services recovered to 25.3, up from 21.5. PMI Composite recovered to 27.4, up from 25.8.

Joe Hayes, Economist at IHS Markit, said: “Plummeting demand for goods is finally catching up with manufacturing sector… Taking April and May data together, they’re indicative of GDP falling at an annual rate in excess of 10% and the economy is going to contract for a third straight quarter. Potential hit to Q2 could be as large as 20% on the previous year.” Also, “damage to the manufacturing sector could continue to worsen as global trade conditions deteriorate and the global economic recovery is slow”.

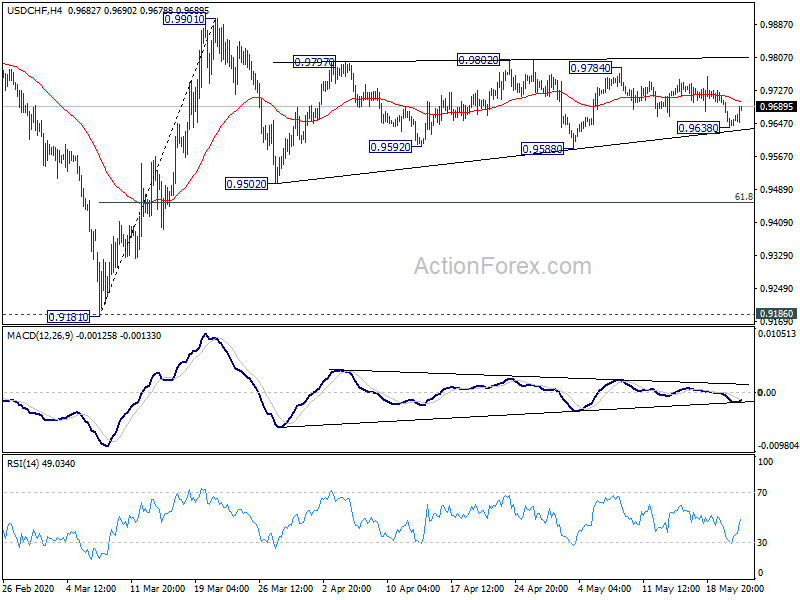

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9618; (P) 0.9668; (R1) 0.9697; More…

USD/CHF recovers again after hitting 0.9638 and intraday bias is turned neutral. Overall outlook is unchanged that corrective pattern from 0.9901 is still in progress. Another fall cannot be ruled out and break of 0.9638 will target 0.9588 support and below. But downside should be contained by 61.8% retracement of 0.9181 to 0.9901 at 0.9456 to rebound. On the upside, break of 0.9784 resistance will target a test on 0.9901 high.

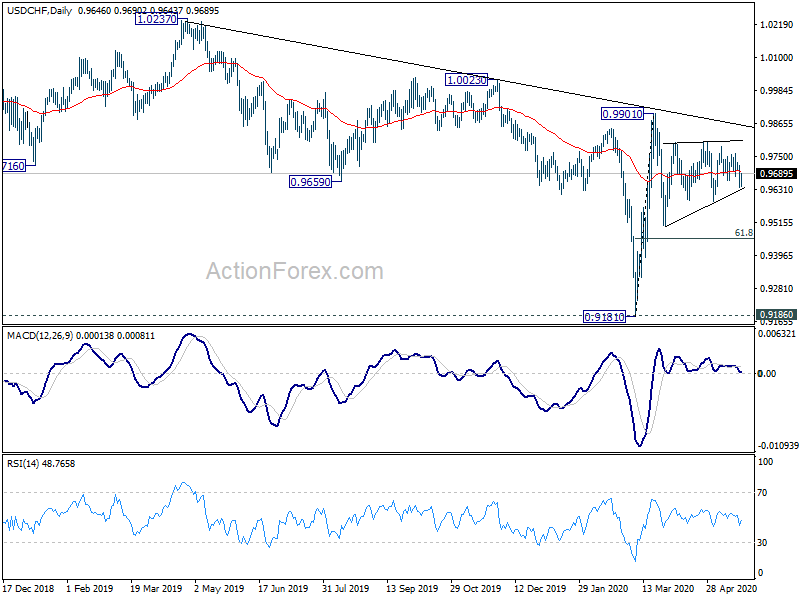

In the bigger picture, decline from 1.0237 is seen as the third leg of the pattern from 1.0342 (2016 low). It could have completed at 0.9181 after hitting 0.9186 key support (2018 low). Break of 0.9901 will extend the rebound form 0.9181 through 1.0023 resistance. After all, medium term range trading will likely continue between 0.9181/1.0237 for some more time.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | CBA Manufacturing PMI May P | 42.8 | 44.1 | ||

| 23:00 | AUD | CBA Services PMI May P | 25.5 | 19.5 | ||

| 23:50 | JPY | Trade Balance (JPY) Apr | -1.00T | -0.78T | -0.19T | -0.38T |

| 00:30 | JPY | Jibun Bank Manufacturing PMI May P | 38.4 | 41.9 | ||

| 07:15 | EUR | France Manufacturing PMI May P | 40.3 | 36 | 31.5 | |

| 07:15 | EUR | France Services PMI May P | 29.4 | 30 | 10.2 | |

| 07:30 | EUR | Germany Manufacturing PMI May P | 36.8 | 40 | 34.5 | |

| 07:30 | EUR | Germany Services PMI May P | 31.4 | 26 | 16.2 | |

| 08:00 | EUR | Eurozone Manufacturing PMI May P | 39.5 | 38 | 33.4 | |

| 08:00 | EUR | Eurozone Services PMI May P | 28.7 | 23.9 | 12 | |

| 08:30 | GBP | Manufacturing PMI May P | 40.6 | 33.5 | 32.6 | |

| 08:30 | GBP | Services PMI May P | 27.8 | 22.1 | 13.4 | |

| 10:00 | GBP | CBI Industrial Order Expectations May | -62 | -50 | -56 | |

| 12:30 | CAD | New Housing Price Index M/M Apr | 0.00% | -0.10% | 0.30% | |

| 12:30 | CAD | ADP Employment Change Apr | -226.7K | -177.3K | ||

| 12:30 | USD | Initial Jobless Claims (May 15) | 2438K | 2400K | 2981K | 2687K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey May | -43.1 | -40 | -56.6 | |

| 13:45 | USD | Manufacturing PMI May P | 38 | 36.1 | ||

| 13:45 | USD | Services PMI May P | 30 | 26.7 | ||

| 14:00 | USD | Existing Home Sales Apr | 4.30M | 5.27M | ||

| 14:30 | USD | Natural Gas Storage | 83B | 103B |