{kind=link}

Yen, Dollar and Swiss Franc remain generally weak today eventual risk rally starts to take a breather in European session. On the other hand, currency market have some what shifted from commodity currencies to Euro and Sterling. Euro is lifted by optimism on the Franco-German recovery fund plan. Sterling is boosted by UK’s new, post-Brexit, tariff regime.

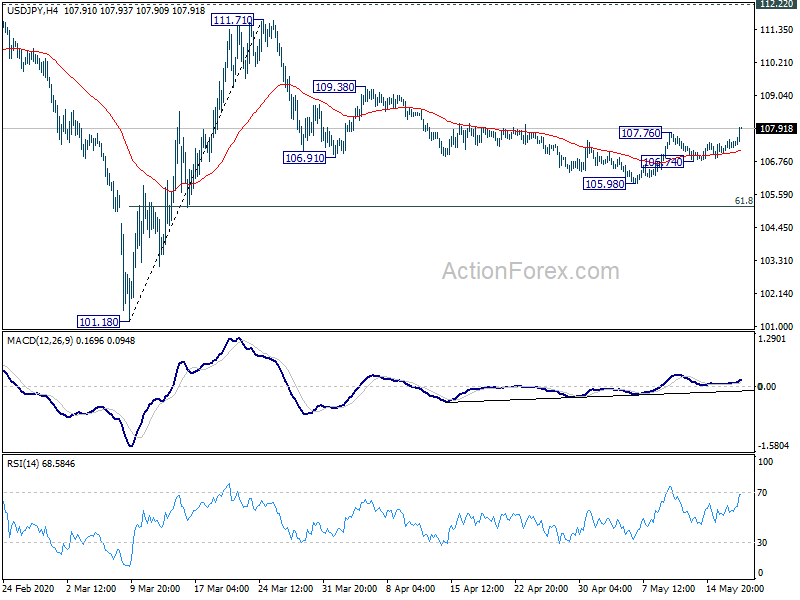

Technically, weakness in Yen is the clearest in the markets for today. USD/JPY’s break of 107.76 resistance suggests resumption of rebound from 105.98, for 109.38 resistance. EUR/JPY’s break of 117.77 resistance should take the rebound from 114.42 to 121.14. 133.18 resistance in GBP/JPY will be a focus today and break will align the near term bullish outlook with USD/JPY and EUR/JPY.

In Europe, currently, FTSE is down -0.47%. DAX is down -0.17%. CAC is down -0.62%. German 10-year yield is up 0.0323 at -0.439. Earlier in Asia, Nikkei rose 1.49%. Hong Kong HSI rose 1.89%. China Shanghai SSE rose 0.81%. Singapore Strait Times rose 1.66%. Japan 10-year JGB yield rose 0.0111 to 0.001.

German Maas very confident on EU support for Franco-German recovery plan

German Foreign Minister Heiko Maas said he’s “very confident” that the Franco-German Recovery Fund plan will get broad support from EU members. He added, “it is a first step to a European solution, we will have to discuss the details within Europe but we have agreed that we must find a solution quickly.”

Euro is apparently lifted by the development, in particular against Swiss Franc. Germany and France agreed to jointly propose the European Commission to borrow EUR 500B on behalf of the whole EU. It’s seen as a material step forward towards a joint fiscal capacity to support recovery out of the coronavirus pandemic. The Commission is expected to outline the proposal before the European summit on May 27.

German ZEW rose to 46.0, optimism is growing, but catching-up will take a long time

German ZEW Economic Sentiment rose to 46.0 in May, up from 25.2, beat expectation of 27.4. That’s the second increase in a row. However, Current Situation Index dropped slightly by -2.0 to -93.5, below expectation of -87.8. Eurozone ZEW Economic Sentiment rose to 51.0, up from 28.2, beat expectation of 30.0. Current Situation Index also dropped slightly by -1.1 to -95.0.

“Optimism is growing that there will be an economic turnaround from summer onwards. This is also reflected in the significant improvement in expectations for the individual sectors. According to the financial market experts surveyed, economic growth is expected to pick up pace again in the fourth quarter of 2020. However, the catching-up process will take a long time. Only in 2022 will economic output return to the level of 2019,” comments ZEW President Achim Wambach.

60% trade will come into UK tariff free with new UKGT regime

UK announced a new post-Brexit MFN tariff regime today, called the UK Global Tariff (UKGT). This will replace the EU’s Common External Tariff starting on January 1, 2021, at the end of the Brexit Transition Period.

Under the new regime, tariffs on a wide range of products will be eliminated. 60% of trade will come into UK tariff free on WTO terms, of through existing preferential access. Successful FTS negotiations will increase the total. Tariffs will be maintained on agricultural products such as lamb, beef and poultry. Car tariffs will be maintained at 10%.

“Our new Global Tariff will benefit UK consumers and households by cutting red tape and reducing the cost of thousands of everyday products,” International Trade Secretary Liz Truss said.

UK claimant counts jumped 8655k to 2.1m in April

In April, UK claimant count, a measure of number of people claiming unemployment benefits, jumped 865.5k to 2.097m. The range of forecasts for this data was wide, from 60k change to as many as 1.5m. The released data was slightly on the high side. Claimant count rate rose to 5.8%, highest in over two decades.

In the three month to March, unemployment rate unexpectedly dropped to 3.9%, down from 4.0%, better than expectation of 4.4%. Average earnings including bonus slowed to 2.4% 3moy, below expectation of 2.7% 3moy. Average earnings excluding bonus slowed to 2.7% 3moy, matched expectations.

RBA minutes: Best course of action was to maintain currency policy setting

In the minutes of May 5 meeting, RBA said the labor market s was expected to have “ongoing spare capacity”. Inflation was expected to stay below 2% “over the following few years. The continue to keep funding costs low and credits available to households and businesses. The “best course of action” was to maintain the currency policy setting, and monitor economic and financial outcomes.

RBA added that while outlook remained uncertain, if coronavirus infection rates continued to decline and restrictions were eased, “recovery could be expected to start later in 2020”. At the same time, the “substantial, coordinated and unprecedented fiscal and monetary response” was “softening” the “very significant economic contraction”.

Coronavirus job losses in Australia slowed

Australia’s Bureau of Statistics said today that coronavirus job losses has slowed down between mid-April and early May. Overall between March 14 and May 2, payroll jobs dropped by -7.3% and total wages paid dropped -5.4%. In the week between April 25 and May 2, jobs decreased by -1.1% only while wages even rose 0.9%.

Head of Labour Statistics at the ABS, Bjorn Jarvis, said: “The latest data shows a further slowing in the fall in COVID-19 job losses between mid-April and early May.” In addition to the fall in total jobs slowing, some industries were now showing a reduced impact in the most recent weeks.

RBNZ Bascand: We can re-evaluate if more stimulus is needed in three months time

RBNZ Deputy Governor Geoff Bascand said the central bank will know more about how the coronavirus shock is playing out in three months. And, “we can re-evaluate if we need to do more or take the foot off the pedal a little bit in three months’ time.”

He noted that negative interest rates were one of many monetary policy options available. “For now, we think the best thing we should be doing is large scale asset purchases and we’ve expanded that. We could expand it further if needed,” he added.

Separately, Assistant Governor Christian Hawkesby said the central bank is open to using all tools including buying foreign bonds. He added RBNZ’s economic projections assumed that New Zealand Dollar will depreciate.

Rleased from New Zealand, PPI inputs dropped -0.3% qoq in Q1. PPI output rose 0.1% qoq.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 107.08; (P) 107.29; (R1) 107.51; More..

USD/JPY’s rise from 105.98 short term bottom resumes by taking out 107.76 resistance. Intraday bias is turned back to the upside for 109.38 resistance. As noted before, corrective fall from 111.71 should have already completed at 105.98. Break of 109.38 will target 111.71 high. However, break of 106.74 minor support will dampen the bullish view and turn bias back to the downside.

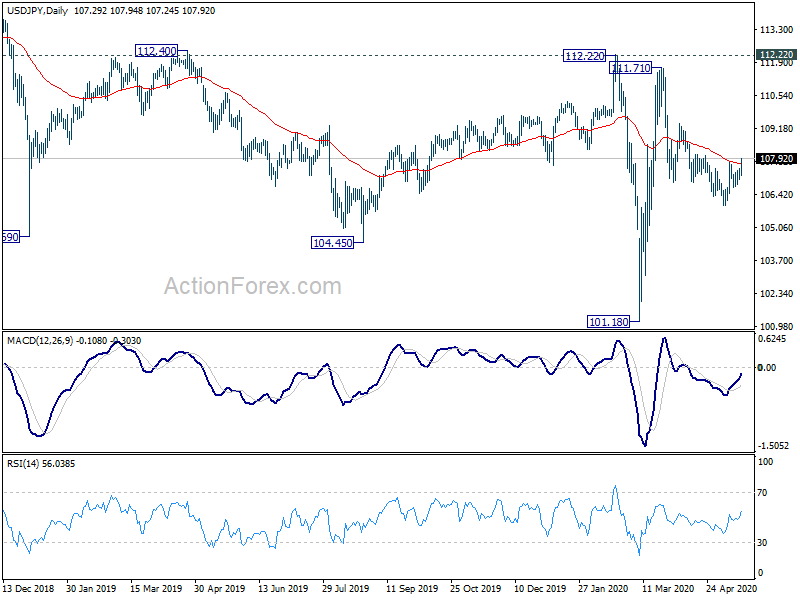

In the bigger picture, at this point, whole decline from 118.65 (Dec 2016) continues to display a corrective look, with well channeling. There is no clear sign of completion yet. Break of 101.18 will target 98.97 (2016 low). Meanwhile, sustained break of 112.22 should confirm completion of the decline and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q1 | -0.30% | 0.10% | 0.30% | |

| 22:45 | NZD | PPI Output Q/Q Q1 | 0.10% | 0.40% | ||

| 01:30 | AUD | RBA Minutes | ||||

| 04:30 | JPY | Industrial Production M/M Mar F | -3.70% | -3.70% | -3.70% | |

| 06:00 | GBP | ILO Unemployment Rate 3M Mar | 3.90% | 4.40% | 4.00% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Mar | 2.40% | 2.70% | 2.80% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Mar | 2.70% | 2.70% | 2.90% | |

| 06:00 | GBP | Claimant Count Change Apr | 856.5K | 12.1K | ||

| 06:00 | GBP | Claimant Count Rate Apr | 5.80% | 3.50% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment May | 51 | 33.5 | 28.2 | |

| 09:00 | EUR | Germany ZEW Current Situation May | -93.5 | -87.8 | -91.5 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | 46 | 27.4 | 25.2 | |

| 12:30 | USD | Building Permits Apr | 1.07M | 1.00M | 1.35M | 1.36M |

| 12:30 | USD | Housing Starts Apr | 0.89M | 0.95M | 1.22M | 1.28M |

| 14:00 | USD | Fed’s Chair Powell testifies |