{kind=link}

Dollar weakens notably in early US session after retail sales data showed another record decline in April. Stock futures also tumble after the news In particular, gold rides on the greenback’s selloff and it’s set to resume larger up trend. . Nevertheless, for the day, New Zealand, Australian Dollar and Sterling remain the worst performing ones. Yen, Swiss Franc, and Euro are the stronger ones,

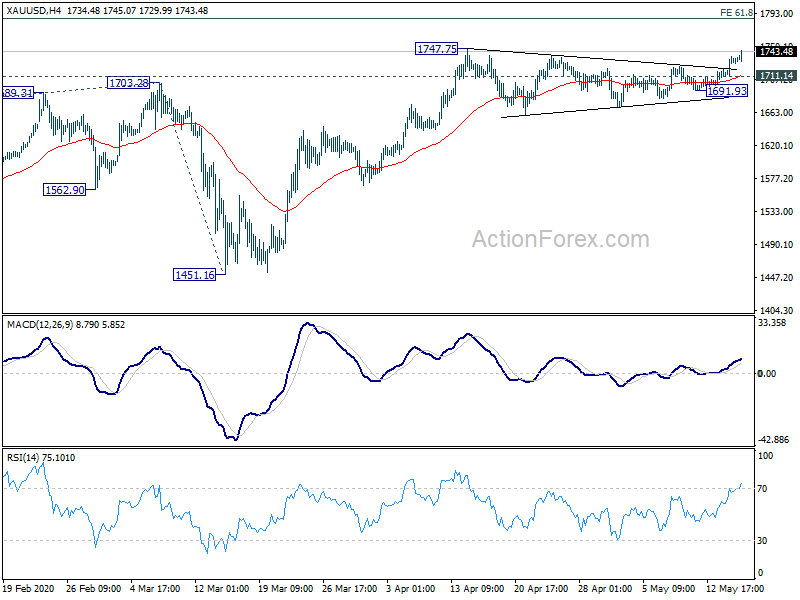

Technically, Gold is eyeing 1747.75 resistance. Decisive break there will target 61.8% projection of 1160.17 to 1703.28 from 1451.16 at 1786.80. Some further upside acceleration could be seen if this major hurdle is overcome. Sterling’s weakness is also worth a watch as EUR/GBP is resuming recent rebound from 0.8670 resumes after brief retreat. Reactions to 0.8987 near term fibonacci resistance would reveal the underlying strength of the cross.

In Europe, currently, FTSE is up 0.65%. DAX is up 0.69%. CAC is down -0.20%. German 10-year yield is down -0.016 at -0.556. Earlier in Asia, Nikkei rose 0.62%. Hong Kong HSI dropped -0.14%. China Shanghai SSE dropped -0.07%. Singapore Strait Times rose 0.05%. Japan 10-year JGB yield rose 0.0007 to -0.004.

US retail sales dropped record -16.4% in April

US retail sales dropped a record -16.4% mom in April to USD 403.9B, worse than expectation of -10.0% mom. That’s also nearly double the -8.3% drop in March, which was the prior worst reading since 1992. Ex-auto sales dropped -17.2% mom, much worse than expectation of -8.6% mom. Ex-gasoline sales dropped -15.5% mom. Ex-auto, ex-gasoline sales dropped -16.2% mom.

Also released, Empire State Manufacturing index rebounded sharply from -78.2 to -48.5 in May, much better than expectation of -65.0.

Very limited progress made after disappointing Brexit negotiations

UK Brexit chief Brexit negotiator David Frost said “very limited progress” were made on the “most significant outstanding issues” with EU after completing the latest round of negotiations. He further warned that if EU persists in its “novel and unbalanced proposals on the so-called level playing field,” two sides won’t be able to reach an agreement.

“We very much need a change in EU approach for the next round,” Frost added. “The U.K. will continue to work hard to find an agreement, for as long as there is a constructive process in being, and continues to believe that this is possible.”

On the other hand, EU chief Brexit negotiation Michel Barnier said the third round of Brexit talks was “disappointing”. But he insisted, “We’re not going to bargain away our values for the benefit of the British economy.”

Eurozone GDP dropped -3.8% in Q1, EU contracted -3.3%

Eurozone GDP contracted -3.8% qoq in Q1. EU GDP contracted -3.3% qoq. Both are worst declines since the series started in 1995. Annually Eurozone GDP contracted -3.2% yoy while EU GDP contracted -2.6% yoy, both were worst since Q3 2009. Employment in dropped -0.2% qoq in both Eurozone and EU, worst declines since 2013.

German recession expected to accelerate in Q2, but recovery began in May

Germany’s GDP shrank -2.2% qoq in Q1, slightly worse than expectation of -2.0% qoq, worst in more than a decade. Also, as Q4’s figure was revised down to -0.1% qoq, the country was already in a technical recession with two straight quarters of contraction.

The contraction is expected to accelerate in Q2, with economists forecasts a -10% decline in GDP. But Germany’s Economy Ministry sounded relatively optimistic. It said in an email statement: “The recovery began with the cautious lifting of the lockdown at the beginning of May. But this process will take a longer time due to the continuation of the corona pandemic.”

China industrial production grew again, but retail sales contracts

China’s industrial production grew 3.9% yoy in April, above expectation of 1.5% yoy. That’s the first expansion reading this year as activity was returning to normal from coronavirus pandemic. However, consumption remained weak as retail sales contracted -7.5% yoy in April, matched expectations. That’s already better than -15.8% contraction of sales in March. Fixed asset investment contracted -10.3% ytd yoy in April, worse than expectation of -10.0%.

Suggested reading: More Stimuli Needed to Support China’s Gradual Economic Recovery

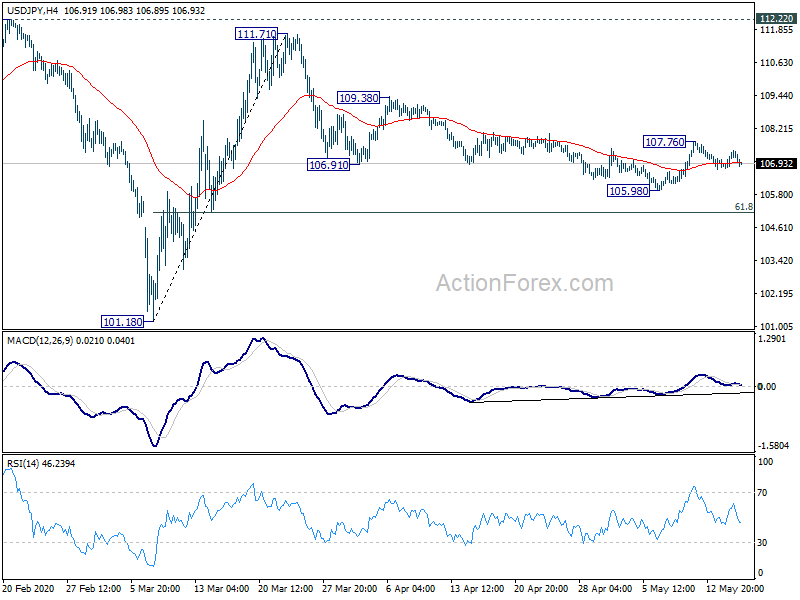

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.89; (P) 107.13; (R1) 107.48; More...

USD/JPY is extending the retreat from 107.76 temporary top and intraday bias stays neutral first. Outlook is unchanged that corrective fall from 111.71 should have completed with three waves down to 105.98. Further rise is expected as long as 105.98 support holds. On the upside, break of 107.76 will turn bias back to the upside for 109.38 resistance first. However, break of 105.98 will dampen our bullish view and bring deeper decline.

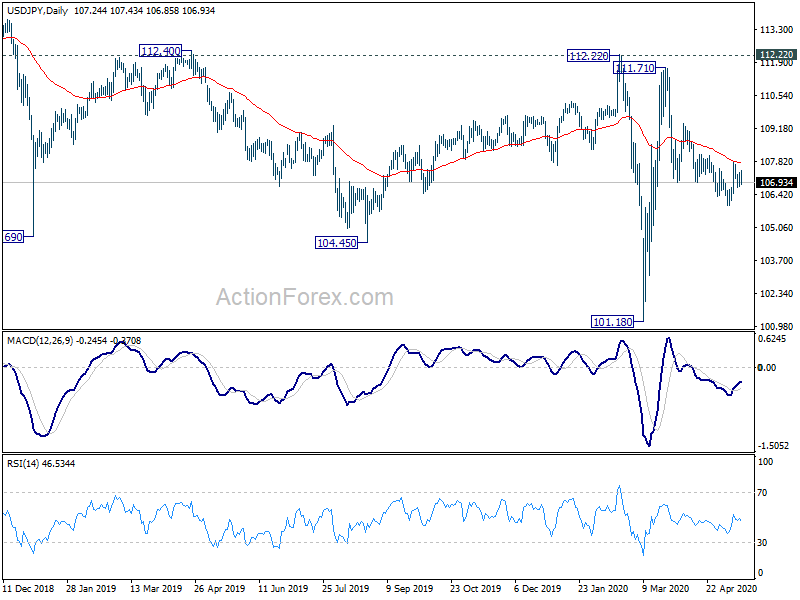

In the bigger picture, at this point, whole decline from 118.65 (Dec 2016) continues to display a corrective look, with well channeling. There is no clear sign of completion yet. Break of 101.18 will target 98.97 (2016 low). Meanwhile, sustained break of 112.22 should confirm completion of the decline and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ Manufacturing Index Mar | 38 | 53.2 | 53.7 | |

| 23:50 | JPY | PPI Y/Y Apr | -2.30% | -1.60% | -0.40% | |

| 02:00 | CNY | Retail Sales Y/Y Apr | -7.50% | -7.50% | -15.80% | |

| 02:00 | CNY | Industrial Production Y/Y Apr | 3.90% | 1.50% | -1.10% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Apr | -10.30% | -10.00% | -16.10% | |

| 08:00 | EUR | Germany GDP Q/Q Q1 P | -2.20% | -2.10% | 0.00% | -0.10% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Mar | 23.5B | 17.2B | 25.8B | |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | -3.80% | -3.80% | -3.80% | |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 P | -0.20% | -2.00% | 0.30% | |

| 12:30 | CAD | Foreign Securities Purchases (CAD) Mar | -9.78B | 20.61B | 19.42 B | |

| 12:30 | USD | Empire State Manufacturing Index May | -48.5 | -65 | -78.2 | |

| 12:30 | USD | Retail Sales M/M Apr | -16.40% | -10.00% | -8.70% | -8.30% |

| 12:30 | USD | Retail Sales ex Autos M/M Apr | -17.20% | -8.60% | -4.50% | -4.00% |

| 13:15 | USD | Industrial Production M/M Apr | -11.60% | -5.40% | ||

| 13:15 | USD | Capacity Utilization Apr | 65.00% | 72.70% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index May P | 68 | 71.8 | ||

| 14:00 | USD | Business Inventories Mar | -0.50% | -0.40% |