{kind=link}

Dollar turned weaker overnight as markets on talks that Fed could eventually go into negative interest rates. Safe haven flows also continued to recede in generally, with NASDAQ extending recent rebound, even though DOW’s rally was still capped. Australian Dollar continues to surge higher, shrugging off RBA’s economic projections. Traders have instead welcomed news of the planned three-staged lockdown exit in Australia. Additionally, top US and China officials seemed to have held a positive phone call on trade. Focus will now turn to employment data from US and Canada.

Technically, EUR/USD recovers ahead of 1.0727 support, suggesting that consolidation is going to extend further. GBP/USD also recovers ahead of 1.2247 support, without indicating near term bearish reversal. AUD/JPY’s break of 68.98 resistance suggests that pull back from 70.16 has completed, maintain near term bullishness to resume rebound form 59.98. With current rebound, Gold’s focus is back on 1747.75 high and break will resume larger up trend.

In Asia, currently, Nikkei is up 2.14%. Hong Kong HSI is up 0.97%. China Shanghai SSE is up 0.91%. Singapore Strait Times is up 0.12%. Japan 10-year JGB yield is down -0.0001 at 0.001. Overnight, DOW rose 0.89%. S&P 500 rose 1.15%. NASDAQ rose 1.41%. 10-year year yield dropped -0.080 to 0.631.

Markets pricing in negative rate for Fed but policymakers reject

Dollar was sold off notably overnight, as stays pressured in Asian session, on talks that Fed might go into negative rates next year, despite objections by some policymakers. Fed fund futures are seeing a one-in-three chance of negative rates next year. Eurodollar options also cover rate at as low as -45bps by mid-2021. At the same time, two-year yield dropped to a record low below 0.14%.

Richmond Fed President Thomas Barkin told CNBC, “I think negative interest rates have been tried in other places and I haven’t seen anything personally that makes me think they are worth a try here.” He also said the US is probably right at the trough down the economic down turn already.

Philadelphia Fed President Patrick Harker said there would be a “high bar” for using negative interest rates as stimulus to the economic. Though, he also warned of re-opening the economy too quickly and “see a significant second wave of the virus”. There would be a “painful economic contraction of GDP in 2021 as shutdowns are reintroduced.”

USTR: Good progress made to make US-China trade agreement a success

As confirmed by a statement of US Trade Representative, Ambassador Robert Lighthizer, Treasury Secretary Steven Mnuchin held a phone call with Chinese Vice Premier Liu He today. Economic and trades issues were discussed, including the Phase One trade agreement between US and China.

The statement noted: “Both sides agreed that good progress is being made on creating the governmental infrastructures necessary to make the agreement a success. They also agreed that in spite of the current global health emergency, both countries fully expect to meet their obligations under the agreement in a timely manner. Meetings required by the agreement have been conducted via conference call and will continue on a regular basis.”

RBA projections -6% GDP contraction in 2020, unemployment rate to peak at 10% in June

In the statement of monetary policy, “the Board will not increase the cash rate target until progress is being made towards full employment and it is confident that inflation will be sustainably within the 2–3 per cent target band”. Additionally, “the Board is committed to do what it can to support jobs, incomes and businesses during this difficult period and to make sure that Australia is well placed for the expected recovery.”

In the latest projections, GDP could contract by as much as -6.00% in the year ended December 2020, then recovered by 6.00% in the year-ended December 2021. Unemployment rate would surge to 10% in June 2020, then gradually drop back to 6.50% in two year’s time, without reaching the pre-crisis level of 5.20%.

Path of headline inflation projected is rather rocky. CPI would tumble to -1.00% in June 2020, then surge to 2.75% by June 2021, then drop back to 1.25-1.50% before June 2022. Trimmed mean inflation would remain steady, though, at between 1.25-1.50% throughout projection horizon, without hitting the 2% target.

On the data front

Japan labor cash earnings rose 0.1% yoy in March, overall household spending dropped -6.0% yoy. Swiss will release unemployment rate in European session while Germany will release trade balance. Later in the day, US non-farm payroll will be the main focus. But don’t forget Canadian employment data too.

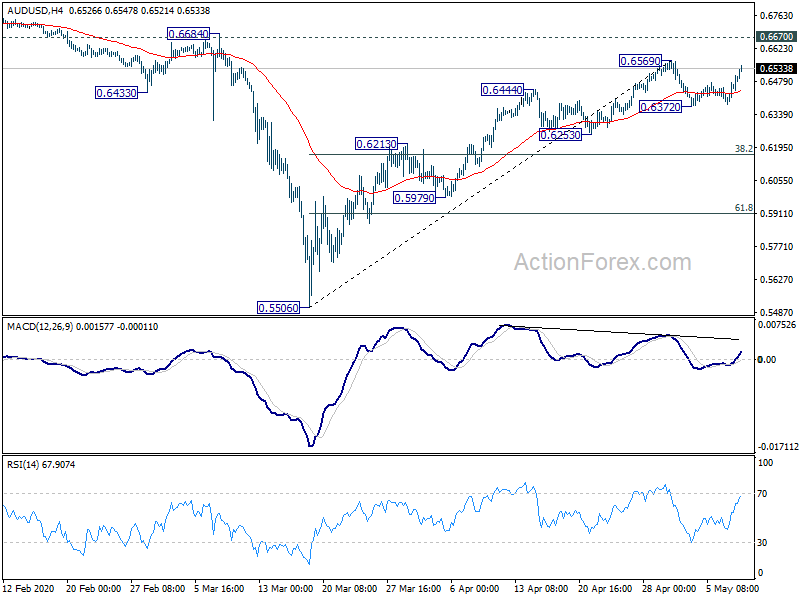

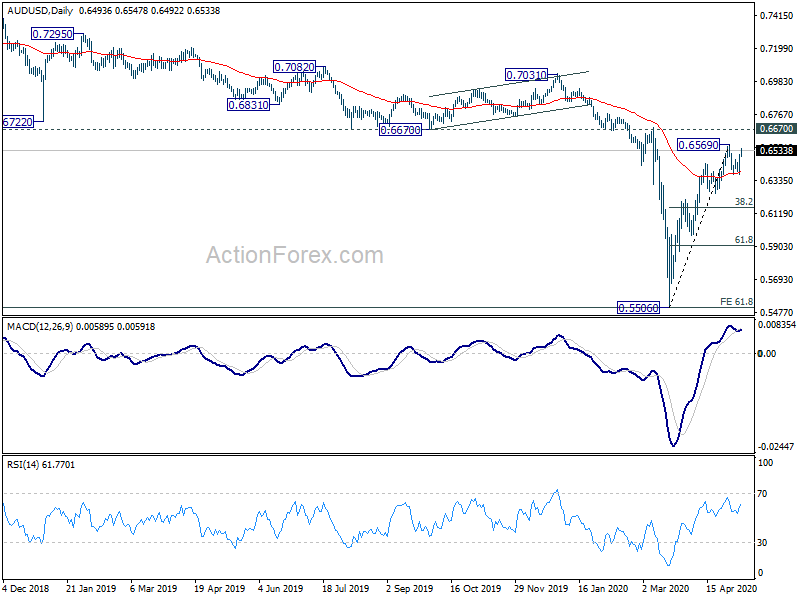

AUD/USD Daily Report

Daily Pivots: (S1) 0.6414; (P) 0.6460; (R1) 0.6541; More…

AUD/USD’s strong rebound argues that rise from 0.5506 is not over yet. Intraday bias stays neutral and focus is back on 0.6595. Break will turn bias to the upside for 0.6670 key resistance next. On the downside, though, break of 0.6372 support will revive the case of short term topping. Intraday bias will be turned back to the downside for 38.2% retracement of 0.5506 to 0.6569 at 0.6163.

In the bigger picture, there is no clear sign of trend reversal yet. The larger down trend from 1.1079 (2011 high) is still in favor to extend. 61.8% projection of 1.1079 to 0.6826 from 0.8135 at 0.5507 is already met. Sustained break there will pave the way to 0.4773 (2001 low). On the upside, however, sustained break of 0.6607 will suggest medium term bottoming and turn focus to 0.7031 resistance next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Mar | 0.10% | 0.10% | 0.70% | |

| 23:30 | JPY | Overall Household Spending Y/Y Mar | -6.00% | -6.70% | -0.30% | |

| 01:30 | AUD | RBA Monetary Policy Statement | ||||

| 05:45 | CHF | Unemployment Rate M/M Apr | 3.40% | 2.80% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Mar | 20.1B | 21.6B | ||

| 12:30 | CAD | Building Permits M/M Mar | -7.30% | |||

| 12:30 | CAD | Net Change in Employment Apr | -5000.0K | -1010.7K | ||

| 12:30 | CAD | Unemployment Rate Apr | 7.20% | 7.80% | ||

| 12:30 | USD | Nonfarm Payrolls Apr | -20000K | -701K | ||

| 12:30 | USD | Unemployment Rate Apr | 14.00% | 4.40% | ||

| 12:30 | USD | Average Hourly Earnings M/M Apr | 0.20% | 0.40% | ||

| 14:00 | USD | Wholesale Inventories Mar | -1.00% | -1.00% |