{kind=link}

Euro tumbles broadly today, together with the Swiss Franc, after Germany’s constitutional court has ruled that ECB’s stimulus program is partly in conflict with the country’s law. ECB has to prove that it’s QE program isn’t providing monetary financing to heavily indebted governments. The German government is also required to get assurance from the ECB that economic and fiscal impact of QE was properly balanced against its monetary policy objectives. Otherwise, the Bundesbank may no longer participate in the implementation and execution of ECB’s program.

Staying in the currency markets, as lifted by rebound in oil prices and stock markets, Canadian Dollar is currently the strongest one, followed by Australian. Dollar is the third weakest following Euro and Swiss. Technically, EUR/USD’s decline today now put 1.0727 support back into focus, break will target 1.0635 low. Similarly, USD/CHF is eyeing 0.9802 resistance again and break will target 0.9901 high. Also, EUR/GBP and EUR/JPY are also eyeing 0.8670 and 115.44 support too. Break will resume recent declines.

In Europe, currently, FTSE is up 1.66%. DAX is up 1.83%. CAC is up 2.03%. German 10-year yield is down -0.010 at -0.572. Earlier in Asia, Hong Kong HSI rose 1.08%. Singapore Strait Times rose 0.34%. China and Japan were still on holiday.

US trade deficit rose to USD -44.4B, deficit with China shrank

US trade deficit rose 11.6% mom to USD -44.4B in March, larger than expectation of USD -41.0B. Imports dropped -6.2% mom to USD 232.2B. Exports dropped -9.6% to USD -187.7B.

Trade deficit with China decreased USD 4.2B to USD -15.5B. Exports to China rose USD 0.3B to USD 7.8B while imports dropped USD -3.9B to USD 23.2B. Trade deficit with EU rose USD 4.3B to USD 16.9B. Exports dropped USD -0.6B to USD 21.8 while imports rose USD 3.7B to USD 38.7B.

Bundesbank Weidmann: Rapid and strong economic recovery unlikely

Bundesbank President Jens Weidmann said a rapid and strong economic recovery is unlikely for Germany, as coronavirus measures are likely to remain in place for a long time. Though, he still expect a sustained recovery once the pandemic is totally over.

As for fiscal stimulus, Weidmann said it’s not the time for them yet as social distance measures remain in place. He added, “a stimulus programme could make sense if a recovery didn’t properly get going later on.”

From Eurozone, PPI dropped -1.5% mom, -2.8% yoy in March, versus expectation of -1.2% mom, -2.4% yoy.

UK PMI composite finalized at 13.8, suggest -7% GDP contraction in Q2 or more

UK PMI Services was finalized at 13.4 in April, down from March’s 34.6. The data indicated a contraction in the service sector activity on an unprecedented scale since survey started in July 1996. PMI Composite was finalized at 13.8, down from March’s 36.0. That’s by far the lowest recorded since the series began in 1998.

Tim Moore, Economics Director at IHS Markit: “Historical comparisons of the PMI with GDP indicate that the April survey reading is consistent with the economy falling at a quarterly rate of approximately 7%, but we expect the actual decline in GDP could be even greater, in part because the PMI excludes the vast majority of the self-employed and the retail sector.

“While output, new work and employment indices all hit all-time lows in April, survey respondents indicated a tentative upturn in their business expectations amid hopes that a gradual re-opening of the economy can be achieved in the summer. However, service providers looking to re-establish business operations overwhelmingly commented that capacity would remain well below previous levels for an extended period and any timings remain highly uncertain.”

Swiss SECO consumer climate dropped to -39, CPI dropped to -1.1%

Swiss SECO consumer climate dropped to -39 in Q2, down from -9. That’s well below the lowest level seen in the 2008-2009 financial and economic crisis. The only other time consumer sentiment values have been this low was in the early 1990s in the wake of the real estate crisis, when the Swiss economy suffered a prolonged recession with a dramatic rise in unemployment.

Looking at some details, expected economic development tumbled from -7.1 to -78.3. Past financial situation improved from -14.2 to -7.2. Expected financial situation improved from -8.0 to -23.6. Major purchases dropped from -8.3 to -48.0.

Also from Swiss, CPI dropped -0.4% mom, -1.1% yoy in April, well below expectation of -0.1% mom, -0.5% yoy.

RBA stands pat, scaled back bond purchases as markets improved

RBA left monetary policy unchanged today as widely expected. The cash rate is held at 0.25%. The bank “will not increase the cash rate target until progress is being made towards” the dual mandate of full employment and inflation target.

Target for 3-year government bond yield is also kept at 0.25%. Global financial markets are working “more effectively” and Australian government bond markets has “improved”. Hence, RBA scaled back the size and frequency of purchases, which “to date have totalled around $50 billion”. Though, the 3-year yield target will “remain in place” and the bank is “prepared to scale up” the purchases if necessary.

In the baseline scenario for the economy, RBA said output would fall by around -10% over H1 2020 and around -6% over the year. There would be a bounce-back of 6% in 2021. Unemployment rate would peak at around 10% over the coming months and stay above 7% by the end of 2020. Inflation will remain below 2% target over the next few years in the various scenarios considered. In the baseline scenario, inflation will be at 1-1.5% in 2021 and gradually picks up further from there.

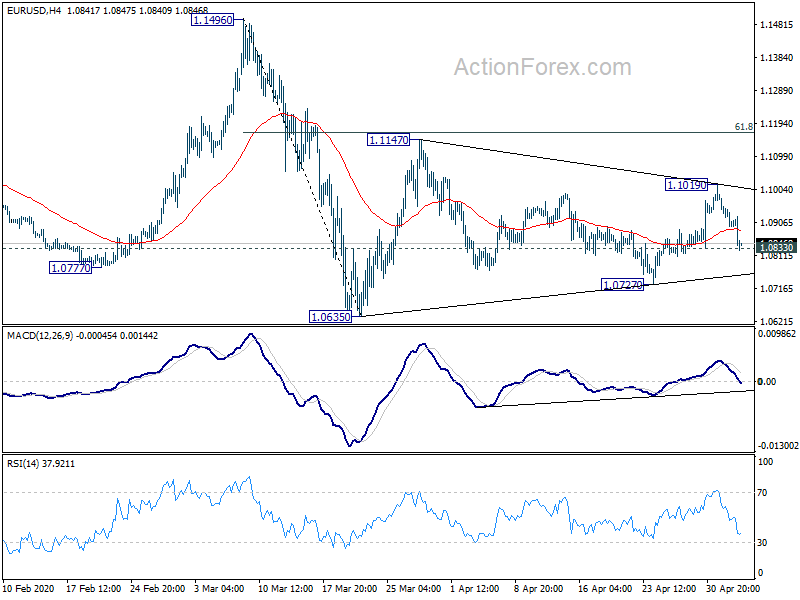

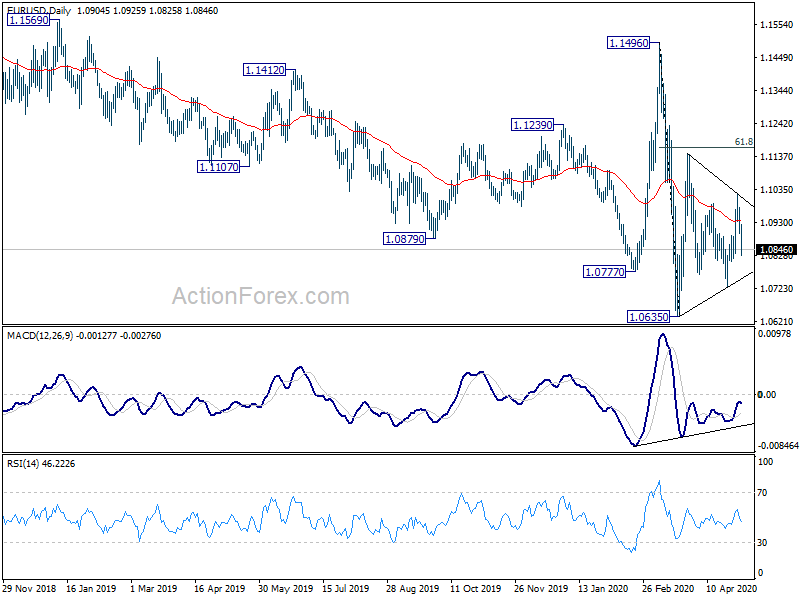

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0871; (P) 1.0925; (R1) 1.0955; More…

EUR/USD’s sharp fall today and breach of 1.0833 minor support suggests that rebound from 1.0727 has completed. Intraday bias is turned back to the downside for 1.0727 first. Break will target 1.0635 low next. On the upside, break of 1.1019 will turn bias to the upside for 1.1147 resistance. After all, corrective pattern from 1.0635 low is still in progress. But in case of rebound, upside should be by 61.8% retracement of 1.1496 to 1.0635 at 1.1167.

In the bigger picture, as long as 1.1496 resistance holds, whole down trend from 1.2555 (2018 high) should still be in progress. Next target is 1.0339 (2017 low). However, sustained break of 1.1496 will argue that such down trend has completed. Rise from 1.0635 could then be seen as the third leg of the pattern from 1.0339. In this case, outlook will be turned bullish for retesting 1.2555.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index Apr | 21.6 | 37.9 | ||

| 22:45 | NZD | Building Permits M/M Mar | -21.30% | 4.70% | 5.70% | |

| 01:00 | NZD | ANZ Commodity Price Apr | -1.10% | -2.10% | -2.00% | |

| 04:30 | AUD | RBA Interest Rate Decision | 0.25% | 0.25% | 0.25% | |

| 05:45 | CHF | SECO Consumer Climate Q2 | -39 | -40 | -9 | |

| 06:30 | CHF | CPI M/M Apr | -0.40% | -0.10% | 0.10% | |

| 06:30 | CHF | CPI Y/Y Apr | -1.10% | -0.50% | -0.50% | |

| 08:30 | GBP | Services PMI Apr F | 13.4 | 12.3 | 12.3 | |

| 09:00 | EUR | Eurozone PPI M/M Mar | -1.50% | -1.20% | -0.60% | -0.70% |

| 09:00 | EUR | Eurozone PPI Y/Y Mar | -2.80% | -2.40% | -1.30% | -1.40% |

| 12:30 | CAD | Trade Balance (CAD) Mar | -1.4B | -2.2B | -1.0B | -0.9B |

| 12:30 | USD | Trade Balance (USD) Mar | -44.4B | -41.0B | -39.9B | -39.8B |

| 13:45 | USD | Services PMI Apr | 27 | 27 | ||

| 14:00 | USD | ISM Non-Manufacturing PMI May | 37.5 | 52.5 |