{kind=link}

US-China tension continues to be a major theme today, driving global stocks and US futures down. Developments are happening on many fronts. There will be proposed law changes to allow private entities to sue China for coronavirus damages. Investment of federal retirement funds in Chinese stocks could be blocked. President Donald Trump might revert to tariffs as punishments. Also, it’s reported that the administration is turbo-charging the initiative to move the global supply chain out of China.

In the currency markets, Canadian Dollar is currently the strongest one, followed by Yen and Dollar. New Zealand Dollar is the weakest, followed by Sterling and Euro. The common currency is somewhat weighed down by poor sentiment indicator. Markets are trying to reverse April’s moves. Yet, it might take more time to confirm if risk aversion is really back. 22941 support in DOW is a key near term level to defend, which DOW is still quite far above. 67.29 support in AUD/JPY is another level to watch.

In Europe, currently, FTSE is flat. DAX is down -3.55%. CAC is down -3.97%. German 10-year yield is up 0.039 at -0.549. Earlier in Asia, Hong Kong HSI dropped -4.18%. Singapore Strait Times dropped -2.31%. Japan and China were on holiday.

Eurozone Sentix investor confidence improved to -41.8, current situation hit all time low

Eurozone Sentix Investor confidence improved slightly from -42.9 to -41.8 in May. But Current Situation Index tumbled further form -66.0 to -73.0, hitting a record low. That’s also the fourth decline in a row. Expectations index, on the other hand, improved from -15.8 to -3.0.

Sentix said the Eurozone economy has experienced a “breath-taking crash” in recent weeks that goes “far beyond the distortions caused by the financial crisis. Nevertheless “dawn comes in the guise of easing the hard restrictions on economic activity. Countries like Germany and Austria are in a position to gradually lift the often drastic measures.”

Eurozone PMI manufacturing finalized at 33.4, any recovery will be frustratingly slow

Eurozone PMI Manufacturing was finalized at 33.4 in April, down from March’s 44.5. Markit said that coronavirus related measures impacted heavily on demand and production. Also, confidence sank to record low and job losses mount. Readings for all major member states are deep in contractionary region. Greece, Italy, France, Austria hit record low. Spain, Germany, Ireland and the Netherlands hit lowest level in more than a decade.

Chris Williamson, Chief Business Economist at IHS Markit, said: “With virus curves flattening and talk now moving to lifting some of the pandemic restrictions, April will have hopefully represented the eye of the storm in terms of the virus impact on the economy, meaning the rate of decline will now likely start to moderate. Barring any second wave of infections, which would throw any recovery off course, the news should start to improve as we see more people and businesses get back to work.

“However, the PMI is indicating an industrial sector that has collapsed at a quarterly rate of decline measured in double digits, and any recovery will be frustratingly slow. Steps needed to keep workers safe will mean even businesses that are able to restart production will generally be running at low capacity, and most will be operating in an environment of greatly reduced demand. Not only will household spending remain historically weak, not least due to ongoing shop closures, but business spending on inputs and machinery and equipment will also remain subdued for some time.”

Also released, Swiss SVME PMI dropped to 40.7 in April, down from 43.7, beat expectation of 34.1.

S&P affirms New Zealand’s rating with positive outlook

S&P Global affirmed New Zealand’s “AA/A-1+” foreign currency and “AA+/A-1+” local currency sovereign credit ratings. A positive outlook is also retrained for the near future. The rating agency said the country’s “monetary policy flexibility, wealthy economy, and solid institutions” are enabling “decisive policy actions” and putting the country in a strong position for economic recovery after the coronavirus pandemic.

Also, “the positive outlook reflects our view that New Zealand’s strong fundamentals would allow its fiscal profile to strengthen after the Covid-19 outbreak subsides, leading to a rating upgrade in the next one to two years.”

Released from Australia, building permits dropped -4.0% mom in March, below expectation of -15.0% mom. TD securities inflation dropped -0.1% mom in April.

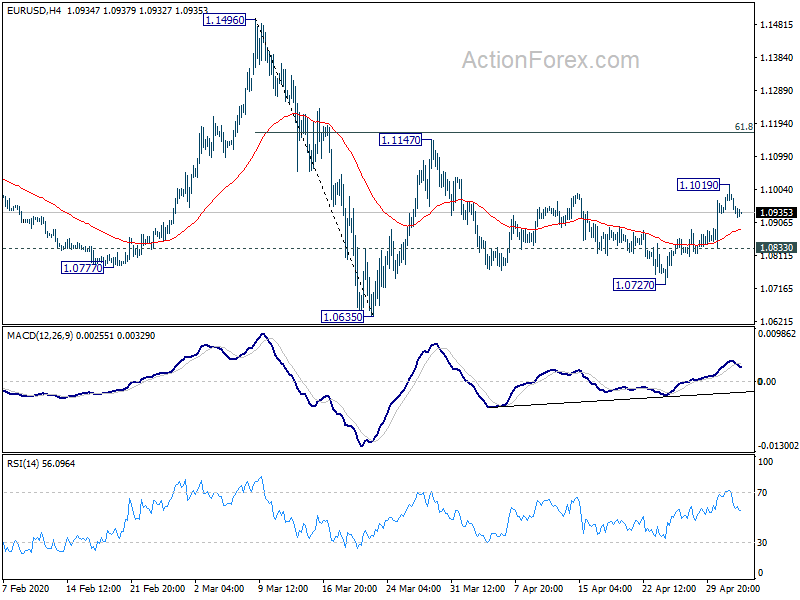

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0937; (P) 1.0978; (R1) 1.1020; More…

Intraday bias in EUR/USD is turned neutral with 4 hour MACD crossed below signal line. Another rise is mildly in favor as long as 1.0833 minor support holds. Corrective pattern from 1.0635 is in its third leg. Above 1.1019 will target 1.1147 resistance. But upside should be limited by 61.8% retracement of 1.1496 to 1.0635 at 1.1167. On the downside, break of 1.0833 will turn bias back to the downside for 1.0727 support and then 1.0635 low.

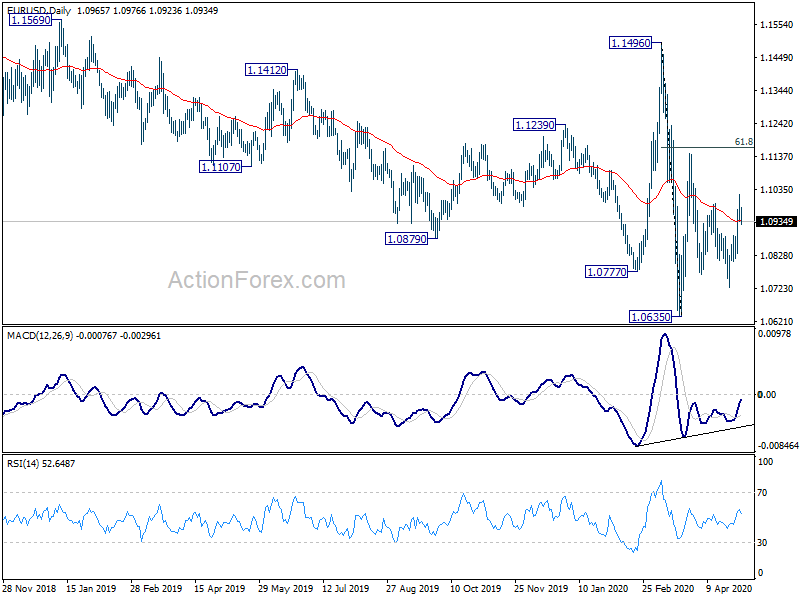

In the bigger picture, as long as 1.1496 resistance holds, whole down trend from 1.2555 (2018 high) should still be in progress. Next target is 1.0339 (2017 low). However, sustained break of 1.1496 will argue that such down trend has completed. Rise from 1.0635 could then be seen as the third leg of the pattern from 1.0339. In this case, outlook will be turned bullish for retesting 1.2555.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | AUD | TD Securities Inflation M/M Apr | -0.10% | 0.20% | ||

| 1:30 | AUD | ANZ Job Advertisements Apr | -53.10% | -10.30% | ||

| 1:30 | AUD | Building Permits M/M Mar | -4.00% | -15.00% | 19.90% | |

| 7:30 | CHF | SVME PMI Apr | 40.7 | 34.1 | 43.7 | |

| 7:45 | EUR | Italy Manufacturing PMI Apr | 31.1 | 30 | 40.3 | |

| 7:50 | EUR | France Manufacturing PMI Apr F | 31.5 | 31.5 | 31.5 | |

| 7:55 | EUR | Germany Manufacturing PMI Apr F | 34.5 | 34.4 | 34.4 | |

| 8:00 | EUR | Eurozone Manufacturing PMI Apr F | 33.4 | 33.6 | 33.6 | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence May | -41.8 | -30 | -42.9 | |

| 14:00 | USD | Factory Orders M/M Mar | -9.50% | 0.00% |