{kind=link}

Yen and Dollar trade generally higher in Asian session today. Trading is relatively subdued with Japan and China on holiday. Yet, the theme of US-China tension drives some risk-off moves. May didn’t start well as investors seemed to be rushing to reverse April’s risk-on moves. As for today, New Zealand Dollar is currently the weakest, followed by Australian and then Sterling.

Technically, there are two levels to watch to gauge is risk aversion is really coming back. Break of 0.6253 support in AUD/USD will mark completion of corrective rebound from 0.5506. Break of 1.4265 resistance in USD/CAD will also mark completion of the corrective pull back from 1.4667. 106.35 temporary low in USD/JPY will determine whether Dollar or Yen would lead if risk sentiments does turn negative.

In Asia, currently, Hong Kong HSI is down -4.03%. Singapore Strait Times is down -2.52%. Japan and China are on holiday.

Trump stepped up criticism on China and promised very conclusive report, HSI dives

Hong Kong stocks gapped sharply lower today and stays pressured, after US President Donald Trump stepped up his criticism on China’s handling of the coronavirus outbreak. He said the government was putting together a report that will be “very conclusive”. “My opinion is they made a mistake. They tried to cover it, they tried to put it out,” he said.

Trump’s comments came hours after Secretary of State Mike Pompeo told ABC, “I can tell you that there is a significant amount of evidence that this came from that laboratory in Wuhan.” A focus will turn to White House deputy national security adviser Matt Pottinger’s speech today, on US relationship with China. Part of the remarks will be delivered in Mandrin, which could carries some direct message to China.

As for US retaliations, an immediate focus would be on whether Trump would use executive order to block a government retirement fund to move some investments to Chinese equities. The so called Thrift Savings Plan, the federal government’s retirement fund, is set to transfer around USD 50B to mirror the MSCI All Country World Index, which includes China. The scheduled move would be carried out by mid-2020. Next would be new tariffs on Chinese goods as Trump indicated.

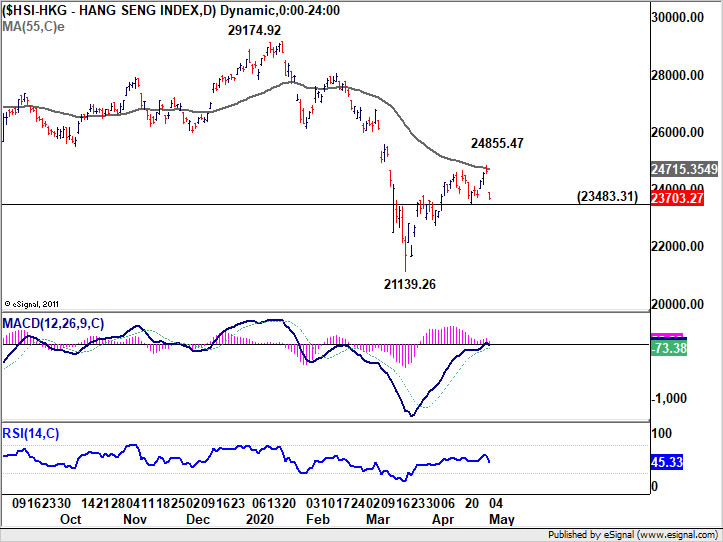

Hong Kong HSI is currently down -947 pts or -3.84% at the time of writing. Rejection by 55 day EMA suggests that rebound from 21139.26 might have completed at 24855.47 already. Focus will be on 23483.31 support. Break will confirm this view and bring retest of 21139.26 low.

S&P affirms New Zealand’s rating with positive outlook

S&P Global affirmed New Zealand’s “AA/A-1+” foreign currency and “AA+/A-1+” local currency sovereign credit ratings. A positive outlook is also retrained for the near future. The rating agency said the country’s “monetary policy flexibility, wealthy economy, and solid institutions” are enabling “decisive policy actions” and putting the country in a strong position for economic recovery after the coronavirus pandemic.

Also, “the positive outlook reflects our view that New Zealand’s strong fundamentals would allow its fiscal profile to strengthen after the Covid-19 outbreak subsides, leading to a rating upgrade in the next one to two years.”

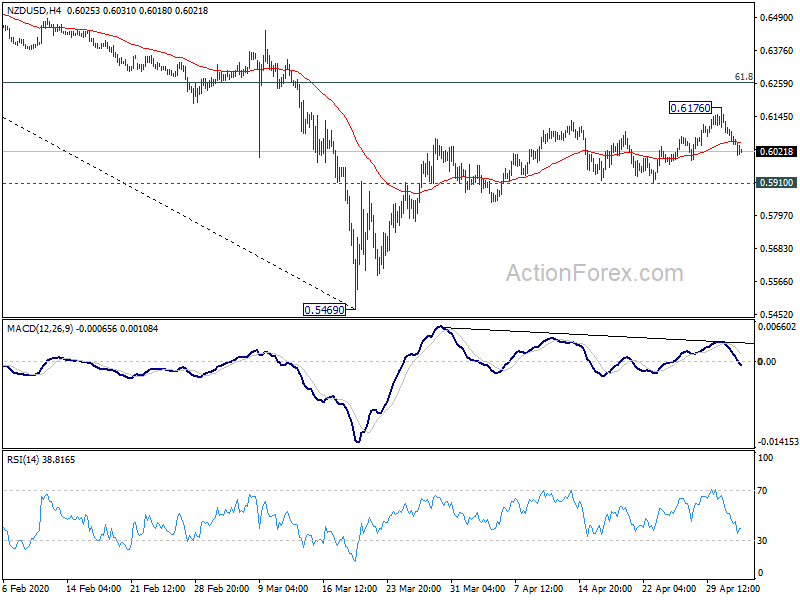

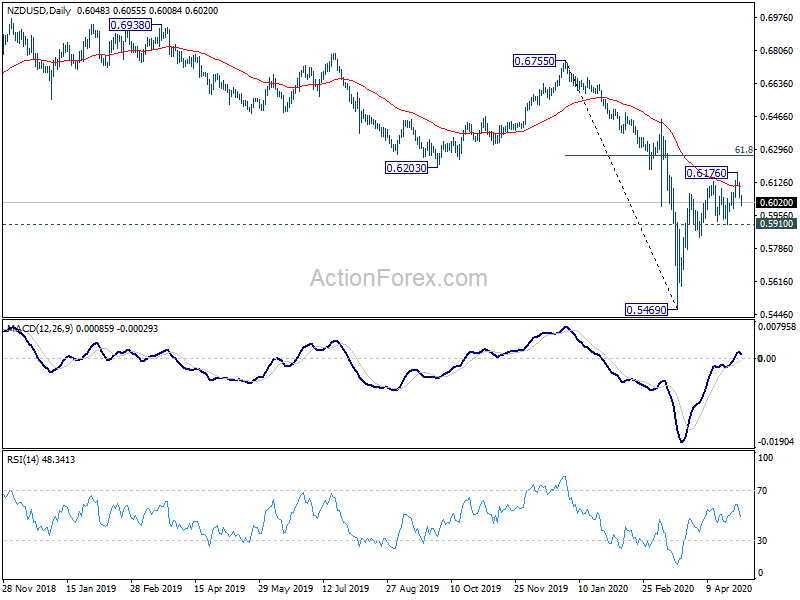

NZD/USD, however, follows risk appetite lower today. Bearish divergence condition in 4 hour MACD suggests short term topping at 0.6176. Focus is back on 0.5910 support. Break there will indicate completion of the corrective rebound from 0.5469. Near term outlook will be turned bearish for retesting this low. In case of another rise, we’d anticipate strong resistance from 61.8% retracement of 0.6755 to 0.5469 at 0.6264 to limit upside.

RBA and BoE to stand pat, US ISM non-manufacturing and NFP watched

Two central banks will meet this week. RBA is generally expected to keep cash rate unchanged at 0.25%. Other stimulus measures, including targeting 3-year bond yield, term funding facility operation and QE, will be maintained too. Main focuses will indeed be on Friday’s monetary policy statement. Economic projections would likely be revised sharply lower. The extent of the downgrade and the path painted could give some hints on policymakers’ mind regarding how long the current stimulus would stay.

BoE will also meet and it’s expected to keep bank rate at 0.10% and asset purchase target at GBP 645B. There are some speculations that BoE would eventually be forced to expand the asset purchases down the road, but timing is not there yet. Some attention would be on the voting and any hints of a bias on further easing.

On the economic data front, US ISM non-manufacturing and non-farm payroll will catch most attentions. China trade balance, Canada employment, and New Zealand employment will also be watched too.

Here are some highlights for the week:

- Monday: Swiss SVME PMI; Eurozone PMI manufacturing final, Sentix investor confidence; US factory orders.

- Tuesday: RBA rate decision, Australia AiG construction; New Zealand building permits; Swiss SECO consumer climate, CPI; Eurozone PPI; UK PMI services final; Canada trade balance; US ISM non-manufacturing, trade balance.

- Wednesday: New Zealand employment; Australia retail sales; Germany factory orders; Eurozone PMI services final, retail sales; UK construction PMI; US ADP employment.

- Thursday: Japan monetary base; China Caixin PMI services, trade balance; Australia trade balance; Germany industrial production; BoE rate decision; Swiss currency reserve; US Challenger job cuts, jobless claims, non-farm productivity; Canada Ivey PMI.

- Friday: RBA monetary policy statement; Japan average cash earnings, household spending; Germany trade balance; Swiss unemployment rate; Canada housing starts, employment; US non-farm payroll employment.

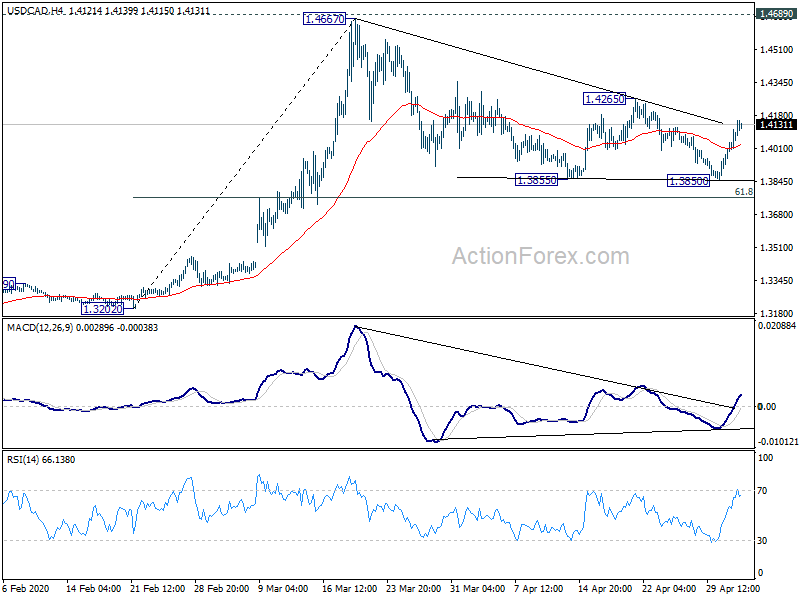

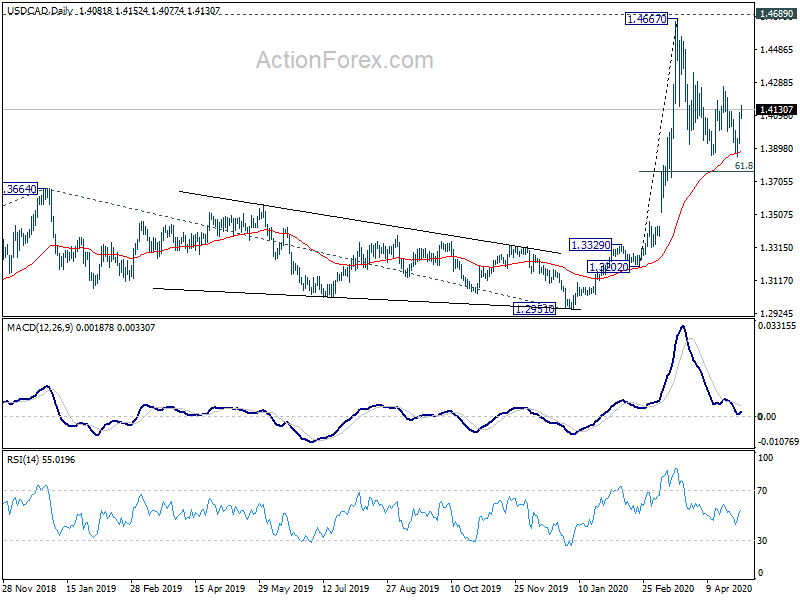

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3976; (P) 1.4043; (R1) 1.4153; More….

Intraday bias in USD?CAD stays neutral first and outlook is unchanged. Price actions from 1.4667 are seen as a corrective pattern. on the upside, break of 1.4265 resistance will indicate completion of the correction. Intraday bias will be turned back to the upside for retesting 1.4667. Intraday bias will be turned back to the upside for retesting 1.4667. In case of another fall, downside should be contained by 61.8% retracement of 1.3202 to 1.4667 at 1.3762 to bring rebound.

In the bigger picture, rise from 1.2061 is likely resuming whole up trend from 0.9056 (2007 low). Decisive break of 1.4689 will confirm this bullish case. Next medium term target is 161.8% projection of 1.2061 to 1.3664 from 1.2951 at 1.5545. Rejection by 1.4689 will bring some consolidations first. But outlook will remain bullish as long as 1.3664 resistance turned support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | AUD | TD Securities Inflation M/M Apr | -0.10% | 0.20% | ||

| 1:30 | AUD | ANZ Job Advertisements Apr | -53.10% | -10.30% | ||

| 1:30 | AUD | Building Permits M/M Mar | -4.00% | -15.00% | 19.90% | |

| 7:30 | CHF | SVME PMI Apr | 34.1 | 43.7 | ||

| 7:45 | EUR | Italy Manufacturing PMI Apr | 30 | 40.3 | ||

| 7:50 | EUR | France Manufacturing PMI Apr F | 31.5 | 31.5 | ||

| 7:55 | EUR | Germany Manufacturing PMI Apr F | 34.4 | 34.4 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Apr F | 33.6 | 33.6 | ||

| 8:30 | EUR | Eurozone Sentix Investor Confidence May | -30 | -42.9 | ||

| 14:00 | USD | Factory Orders M/M Mar | -9.50% | 0.00% |