{kind=link}

Global markets are set to end the week on a high note. There is optimism that Gilead’s coronavirus drug remdesivir could be the cure for the coronavirus. Also, traders responded positively to US President Donald Trump’s three-stage reopening plan. Commodity currencies are trading generally higher today. Dollar, Euro and Swiss Franc are the weakest.

Though, there are still some underlying risks. Firstly, oil price is having no cheer as WTI crude May future is down and pressing 18 handle. Secondly, gold is hovering below 1700, shrugging off Dollar’s weakness. Thirdly, there is also no apparent selling in the Japanese Yen. The overall picture might be different when the week finally closes.

In Europe currently, FTSE is up 3.26%. DAX is up 3.63%. CAC is up 3.96%. German 10-year yield is down -0.0046 at -0.479. Earlier in Asia, Nikkei rose 3.15%. Hong Kong HSI rose 1.56%. China Shanghai SSE rose 0.66%. Singapore Strait Times rose 0.09%. Japan 10-year JGB yield rose 0.0096 to 0.016.

Bundesbank Weidmann: An expansionary monetary and fiscal policy will remain necessary for some time, but not permanently

Bundesbank President Jens Weidmann said monetary policy is making a “major and important contribution within the scope of its mandate” to counter the impact of the coronavirus pandemic. But it’s “not yet possible” to say whether the coronavirus measures taken to date will be “enough” he added.

“The decisive factors for economic developments will be the further course of the pandemic, the length of the lockdown and whether the measures taken successfully address liquidity and potential solvency problems facing firms and households,” he said.

Weidmann admitted “an expansionary monetary and fiscal policy will in any case remain necessary for some time.” But he also argued that “the pandemic plainly shows how important a solid fiscal policy is.” “An extremely expansionary fiscal stance cannot be sustained permanently,” he said. “Going forward, then, all countries will have to focus on reducing the very high debt ratios and ensuring acceptance in the capital markets, and to do this in a way that is compatible with our fiscal rules.”

Eurozone CPI finalized at 0.7% in March, EU at 1.2%

Eurozone CPI was finalized at 0.7% yoy in March, down from February’s 1.2% yoy, half of 1.4% yoy a month ago. The highest contribution to the annual Eurozone inflation rate came from services (+0.60%), followed by food, alcohol & tobacco (+0.46%), non-energy industrial goods (+0.13%) and energy (-0.45%).

EU CPI was finalized at 1.2%, down from February’s 1.6% yoy, also down from 1.6% yoy a year ago. The lowest annual rates were registered in Spain, Italy, Cyprus and Portugal (all 0.1%). The highest annual rates were recorded in Hungary, Poland (both 3.9%) and Czechia (3.6%). Compared with February, annual inflation fell in twenty-six Member States and rose in one.

China GDP contracted -6.8% in Q1, but March data show improvements

China’s GDP contracted -6.8% quarter over year in Q1. That’s the worst performance since at least 1992 as the country was brought to paralysis coronavirus outbreak. The contraction was also slightly larger than expectation of -6.0%.

In March, retail sales dropped -15.8% yoy, after tumbling for -20.5% yoy in the first two months, versus expectation of -8.8% yoy. Industrial production dropped -1.1% yoy, much less severe than expectation of -5.6% yoy. Fixed asset investments contracted -16.1% ytd yoy in January-March period, below expectation of 15.1% yoy, improved from January-February’s -24.5% ytd yoy.

Suggested reading: China’s GDP Contracted the Most in Decades as Driven its Self-Produced Coronavirus.

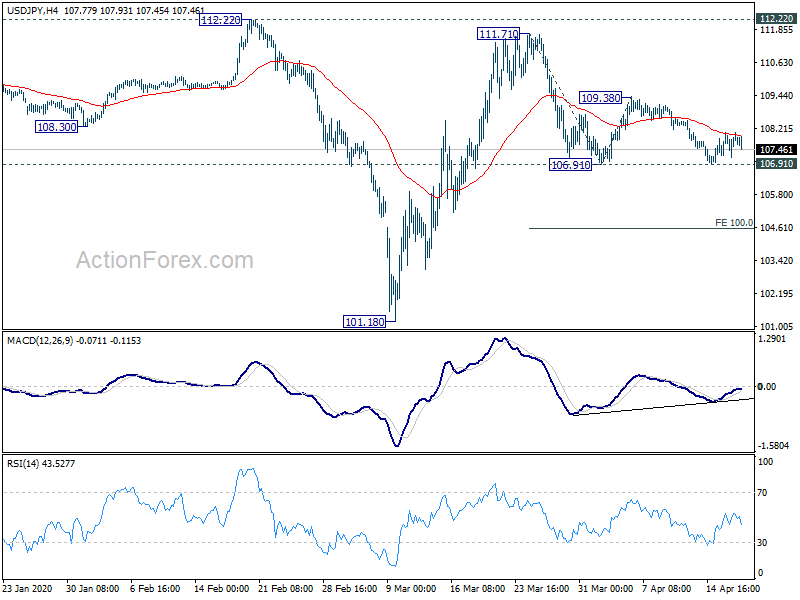

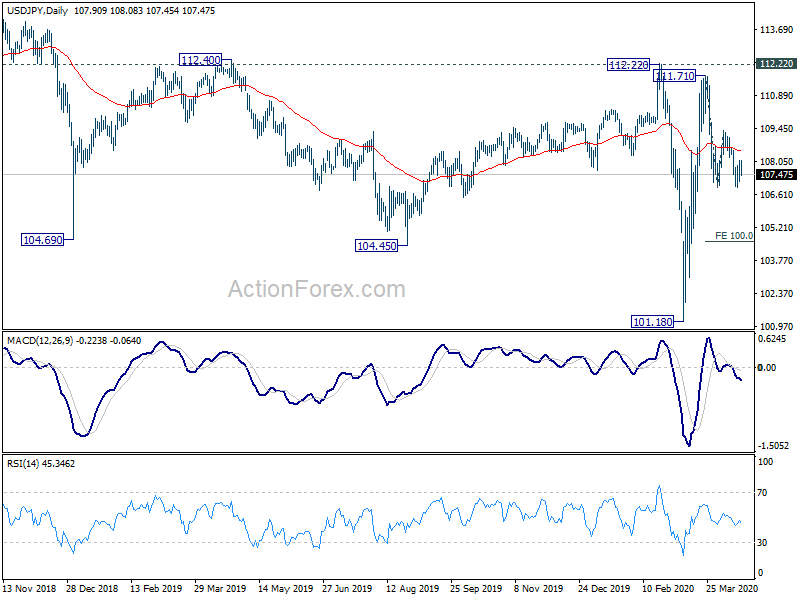

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 107.33; (P) 107.70; (R1) 108.24; More...

USD/JPY is still staying in range above 106.91 support and intraday bias remains neutral. On the downside, firm break of 106.91 support will resume whole decline from 111.71. Intraday bias will be turned to the downside for 100% projection of 111.71 to 106.91 from 109.38 at 104.58. On the upside, break of 109.38 will suggest that fall from 111.71 has completed. Intraday bias will be turned back to the upside for 111.71/112.22 resistance zone.

In the bigger picture, at this point, whole decline from 118.65 (Dec 2016) continues to display a corrective look, with well channeling. There is no clear sign of completion yet. Break of 101.18 will target 98.97 (2016 low). Meanwhile, sustained break of 112.22 should confirm completion of the decline and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 2:00 | CNY | GDP Q/Y Q1 | -6.80% | -6.00% | 6.00% | |

| 2:00 | CNY | Retail Sales Y/Y Mar | -15.80% | -8.80% | -20.50% | |

| 2:00 | CNY | Industrial Production Y/Y Mar | -1.10% | -5.60% | -13.50% | |

| 2:00 | CNY | Fixed Asset Investment YTD Y/Y Mar | -16.10% | -15.10% | -24.50% | |

| 4:30 | JPY | Tertiary Industry Index M/M Feb | -0.50% | -0.20% | 0.80% | |

| 4:30 | JPY | Industrial Production M/M Feb F | -0.30% | 0.40% | 0.40% | |

| 8:00 | EUR | Italy Trade Balance (EUR) Feb | 6.09B | 0.54B | 0.55B | |

| 9:00 | EUR | Eurozone CPI Y/Y Mar F | 0.70% | 0.70% | 0.70% | |

| 9:00 | EUR | Eurozone CPI – Core Y/Y Mar F | 1.00% | 1.00% | 1.00% |