{kind=link}

ECB’s massive coronavirus pandemic program do have notably impact on peripheral bond markets. In particulars, Italian and Spanish bond yields dropped sharply today, with Italy 10-year yield back below 1.9% currently, Spanish 10-year yield below 0.9%. The boost to other markets is not that apparent though, as European stocks are quick to reverse initial gains and turn red.

In the currency markets, selling focus has indeed turned to Euro now. Technically, EUR/USD breaches 1.0777 low, which suggests that larger up trend is likely resuming. Deep retreat is also seen in EUR/GBP after hitting 0.9499. Nevertheless, for today, commodity currencies remain the weakest ones, led by New Zealand Dollar. Dollar is the best performing one.

In Europe, currently, FTSE is down -1.86%, DAX is down -1.04%. CAC is down -0.68%. German 10-year yield is down -0.0007 at -0.218. Earlier in Asia, Nikkei dropped -1.04%. Hong Kong HSI dropped -2.61%. China Shanghai SSE dropped -0.98%. Singapore Strait Timed dropped -4.73%. Japan 10-year JGB yield rose 0.0236 to 0.091.

US initial jobless claims jumped 70k to 281k, clearly attributable to coronavirus impacts

US initial jobless claims rose 70k to 281k in the week ending March 14, well above expectation of 220k. It was also the highest reading since September 2017. Four-week moving average of initial claims rose 16.5k to 232.25. Continuing claims rose 2k to 1.701m in the week ending March 7. Four-week moving average of continuing claims dropped -7k to 1.703m.

DOL said, “During the week ending March 14, the increase in initial claims are clearly attributable to impacts from the COVID-19 virus. A number of states specifically cited COVID-19 related layoffs, while many states reported increased layoffs in service related industries broadly and in the accommodation and food services industries specifically, as well as in the transportation and warehousing industry, whether COVID-19 was identified directly or not.”

Also released, US current account deficit narrowed to USD -110B in Q4, versus expectation of USD -109B. Canada new housing price index rose 0.4% mom in February, above expectation of 0.1% mom. Canada ADP employment rose 7.2k in February.

SNB stands pat at -0.75%, expects negative inflation and growth this year

SNB kept sign deposit rate unchanged at -0.75% today. It noted that coronavirus is posing “exceptionally large challengers” for Switzerland, and the expansionary monetary policy is “more necessary than ever” for ensuring appropriate monetary conditions. The central bank is “intervening more strong” in the FX markets to stabilize the situation. Both negative interest and interventions are “necessary to reduce the attractiveness of Swiss franc investments”.

Additionally, SNB is raising the exemption threshold as of April 2020 to reduce the negative interest burden on the banking system. The threshold factors will increase from 25 to 30. It’s also examining whether a “relaxation of countercyclical buffer” would be possible.

New conditional inflation forecast is lowered primarily due to “lower oil prices, significantly weaker growth prospects and stronger Swiss franc”. Inflation is expected to be in slightly negative territory at -0.3% this year, turned slightly positive to 0.3% in 2021, then rise to 0.7% in 2022. Growth is “likely to be negative” for 2020 as a whole.

Chairman Thomas Jordan emphasized key coronavirus measures “do not come from central banks”. Instead, they come from “medical measures and also from the fiscal side”. For the central bank, “we have to provide the financial system with enough liquidity to ensure the credit flow to the economy does not dry up…so firms can survive this very difficult situation.”

Ifo: German economy could shrank -1.5% this year in better case scenario

Ifo institute said in its spring forecast that the global economy is “collapsing” as a result of coronavirus pandemic. Global GDP would grow only 0.1% this year, comparing with 2.6% last year. World trade would see a decline of -1.7%. There are also “considerable” downside risks in the forecast.

German economy could shrink by -1.5% this year. That could reduce growth rate by almost -3%, comparing with a situation without the outbreak. The full effect of the coronavirus crisis will be seen in Q2, leading to -4.5% contraction in GDP. By first half of 2021, production of goods and services should then “gradually return to a normal level”. In a second scenario, which includes bigger production restrictions, economic output will shrink by -6%

ECB wins European praises with PEPP

ECB’s massive EUR 750B Pandemic Emergency Purchase Programme announced overnight won praises from top European politicians. French President Emmanuel Macron said he gives “full support for the exceptional measures taken this evening by the ECB.” He added,”it is now up to us, the European states, to step up to the plate via our budgetary interventions and to show a bigger financial solidarity at the heart of the euro zone.”

Also from France, Finance Minister Bruno Le Maire said “The plan that the European Central Bank announced is the right one… It’s a massive plan because it foresees 750 billion euros ($813 billion) in asset purchases, it will have a strong economic impact because it will allow companies to be better financed and it will have a major political impact, it will reduce the risk of fragmentation in the euro zone.”

Germany’s Economy Minister Peter Altmaier also said, “I hope these measures will also make it clear to the stock markets, to the markets today that Europe will protect its interests and Europe is determined to overcome this crisis”.

ECB launches EUR 750B Pandemic Emergency Purchase, will considering lifting self-impose limits

In a unexpected move, ECB announced a massive EUR 750B Pandemic Emergency Purchase Programme (PEPP) late yesterday. The temporary program is for countering the “serious risks to monetary policy transmission mechanism” and the economy outlook posed by “outbreak and escalating diffusion” of the coronavirus. Purchases of private and public sector securities will be conducted until the end of 2020, including all asset categories under the existing APP.

ECB Governing Council pledged to “ensure that all sectors of the economy can benefit from the supportive financing conditions that enable them to absorb this shock”. Also, it’s “fully prepared to increase the size” of the purchases and adjust the composition, “by as much as necessary and for as long as needed”. The central bank will also consider to revise the “self-imposed limits” that might hamper its actions.

“Extraordinary times require extraordinary action,” ECB President Christine Lagarde said. “There are no limits to our commitment to the euro. We are determined to use the full potential of our tools, within our mandate.”

Suggested readings on ECB:

- ECB Research: Emergency Meeting – All In With EUR750bn Package

- (ECB) ECB Announces €750 Billion Pandemic Emergency Purchase Programme (PEPP)

RBA cuts rate to 0.25%, starts government bond purchases

RBA announces a package of coronavirus response today. Firstly, cash rate is cut by 25bps to 0.25%. Additionally, the central bank will start purchases of government bonds to keep 3 year yield at around 0.25%, starting tomorrow. A three-year funding facility will also be set up to provide credit support to small and medium-sized businesses. Lastly, exchange settlement balances will be remunerated at 10 basis points, instead of zero.

The central said, “the various elements of this package reinforce one another and will help to lower funding costs across the economy and support the provision of credit, especially to small and medium-sized businesses.” “Today’s policy package from the Reserve Bank complements the welcome fiscal response from governments in Australia. Together, these measures will support jobs, incomes and businesses through this difficult period and they will also assist the Australian economy in the recovery.”

Suggested readings on RBA:

- RBA Announced Emergency Rate Cut, Initiated QE

- RBA and Commonwealth Treasury Announce Initiatives to Support the Financial System

- (RBA) Statement by Philip Lowe, Governor: Monetary Policy Decision

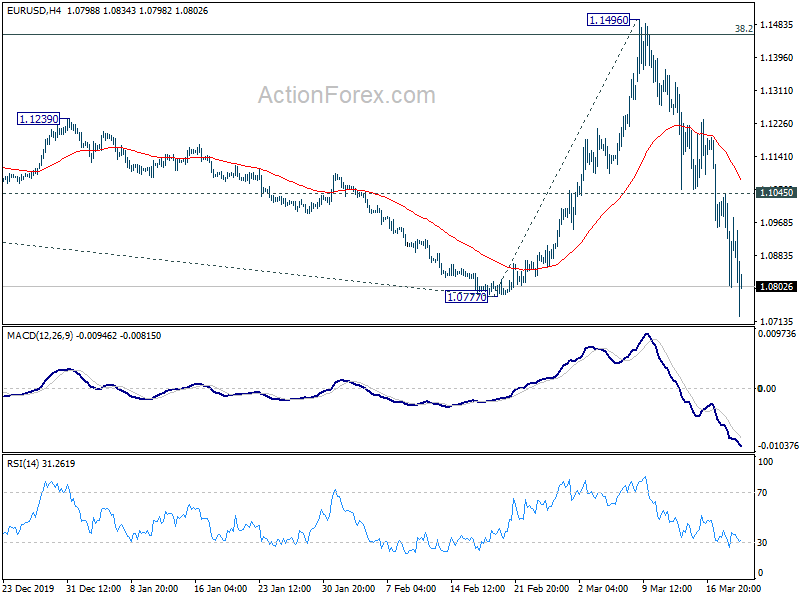

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0957; (P) 1.1001; (R1) 1.1024; More…

EUR/USD drops to as low as 1.0725 today and break of 1.0777 low argues that medium term down trend might be resuming. Intraday bias stays on the downside for now. Sustained trading below 1.0777 will pave the way to 61.8% projection of 1.2555 to 1.0777 from 1.1496 at 1.0397. ON the upside, though, break of 1.1045 resistance will indicate short term bottoming and turn bias to the upside for rebound.

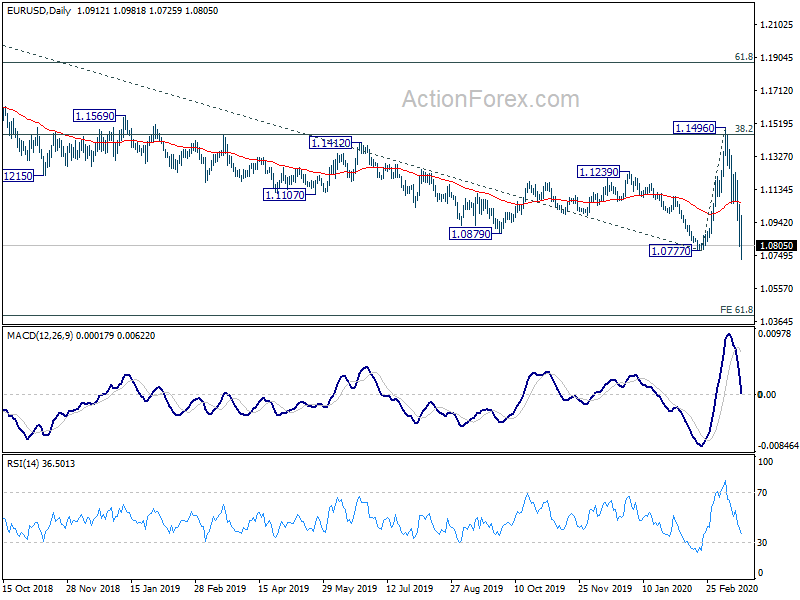

In the bigger picture, rebound from 1.0777 low faced heavy rejection from 38.2% retracement of 1.2555 to 1.0777 at 1.1456, as well as 55 month EMA. The development argues that price actions from 1.0777 medium term pattern were just correcting the down trend from 1.2555 (2018 high). Further decline is in favor to retest 1.0339 (2017 low). Nevertheless, sustained break of 1.1456 will raise the chance of medium term bullish reversal and target 61.8% retracement at 1.1876.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q4 | 0.50% | 0.50% | 0.70% | 0.80% |

| 23:30 | JPY | National CPI Core Y/Y Feb | 0.60% | 0.60% | 0.80% | |

| 00:30 | AUD | Employment Change Feb | 26.7K | 8.5K | 13.5K | 12.9K |

| 00:30 | AUD | Unemployment Rate Feb | 5.10% | 5.30% | 5.30% | |

| 00:30 | AUD | RBA Bulletin | ||||

| 03:30 | AUD | RBA Rate Decision | 0.25% | 0.50% | ||

| 04:30 | JPY | All Industry Activity Index M/M Jan | 0.80% | 0.20% | 0.00% | -0.10% |

| 07:00 | CHF | Trade Balance (CHF) Feb | 3.57B | 4.23B | 4.78B | |

| 08:30 | CHF | SNB Interest Rate Decision | -0.75% | -0.75% | -0.75% | |

| 12:30 | CAD | ADP Employment Change Feb | 7.2K | 25.9K | ||

| 12:30 | CAD | New Housing Price Index M/M Feb | 0.40% | 0.10% | 0.00% | |

| 12:30 | USD | Initial Jobless Claims (Mar 13) | 281K | 220K | 211K | |

| 12:30 | USD | Current Account (USD) Q4 | -110B | -109B | -124B | -125B |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Mar | 10.2 | 36.7 | ||

| 14:30 | USD | Natural Gas Storage | -5B | -48B |