{kind=link}

Risk aversion continues to be the main theme in the markets today, on the back of global coronavirus pandemic and plunge in oil price. US trading is halted for 15 minutes after DOW tanks more than -1800 pts at open while S&P 500 drops -7%.. The selloff triggered a key market circuit breaker which halts trading for 15minutes. In the currency markets, commodity currencies remain the weakest ones, led by Canadian. Yen, Euro and Swiss are the strongest. Dollar remains mixed as it reversed much of earlier gains against commodity currencies.

Europe is currently the major focal point in the global coronavirus outbreak. Italy’s number hit 7375 with 366 deaths. Cases in France (1209), Germany (1151) and Spain (1036) breaks 1000 level. Swiss (374), the Netherlands (321), UK (280), Sweden (248) Belgium (239) Norway 183) and Austria (112) are up and coming. French President Emmanuel Macron took initiatives today and called on EU partners to take urgent actions to coordinate sanitary measures, research efforts and economic response. He’s going to hold a call with EU leaders on Tuesday. Situation in South Korea (7478) eased a bit but remains devastating in Iran (7161). The US, with 566 cases and 22 deaths, is also closely watched.

In Europe, currently, FTSE is down -7.78%. DAX is down -7.57%. CAC is down -7.80%. German 10-year yield is down -0.192 at -0.904. Earlier in Asia, Nikkei dropped -5.07%. Hong Kong HSI dropped -4.23%. China Shanghai SSE dropped -3.01%. Singapore Strait Times dropped -6.03%. Japan 10-year JGB yield rose 0.0024 to -0.143.

Eurozone Sentix plunged to -17, a new Lehman moment in the making

Eurozone Sentix Investor Confidence dropped sharply to -17 in March, down from 5.2, missed expectation of -11. That’s the lowest level since April 2013. Current Situation index dropped from 4.0 to -14.3, lowest since October 2019. Expectations index plunged from 6.5 to -20.0, lowest since August 2012.

Global Overall index dropped form 8.1 to -12.0, lowest since July 2009. Current Situation index dropped from 10.5 to -8.8, lowest since November 2009. Expectations index dropped from 5.8 to -15.3, lowest since October 2011. Regional readings suggested Eurozone, Germany, Eastern Europe, Japan, Asia ex-Japan and Latin America are all in recession. Swiss, Austria, USA and global are in downturn.

Also released in European session, Germany trade surplus narrowed to EUR 18.5B in January, below expectation of EUR 18.8B. Industrial production rose 3.0% mom in January versus expectation of 1.5% mom. Swiss unemployment rate was unchanged at 2.3% in February.

Germany unveils EUR 12.4B coronavirus relieve package

German government announced additional EUR 12.4B in state investment to help companies hit by the coronavirus outbreak. The package agreed by the coalition include liquidity support to companies suffering coronavirus related cash crunch There will be expansions to access to the government subsidized scheme called “Kurzabeit”.

Olaf Scholz, finance minister, pledged that Germany was prepared “to do everything needed to stabilise the economy and secure jobs”. “We will ensure that there is always enough liquidity available for business”. He added that it’s impossible to say if Germany will slip into recession this year.

Italian PM Conte promised massive shock therapy to overcome coronavirus impacts

Italian Prime Minister Giuseppe Conte promised “massive shock therapy” to overcome the impact of the coronavirus outbreak. The country announced on Sunday massive lockdown across much of its north, including the financial capital Milan. He told La Repubblica, “we will not stop here. We will use a massive shock therapy. To come out of this emergency we will use all human and economic resources.

Conte will meet representatives of opposition to discuss new economic measures. the coalition government is also studying various initiatives. Meanwhile, he also called for EU to loosen borrowing limit to allow room for more fiscal measures. He said, “Europe cannot think of confronting an extraordinary situation with ordinary measures.”

BoJ Kuroda: Uncertainty heightening, sentiment deteriorating, markets unstable

BoJ Governor Haruhiko Kuroda told the parliament today, “uncertainty over Japan’s economic outlook is heightening. Investor sentiment is deteriorating somewhat, with market moves unstable.”

He added, “we’ll take appropriate action without hesitation as needed with an eye on the impact of the spread of the coronavirus, particularly through domestic and overseas market moves.”

The comments raises the chance of some sort of policy stimulus to be announced after meeting on March 18-19. But it’s unsure which part of BoJ’s toolbox would be adopted.

Japan Q1 GDP contracted more than expected by -1.8% qoq. Bank lending rose 2.1% yoy in February versus expectation of 1.9% yoy. Current account surplus narrowed to JPY 1.63T in January.

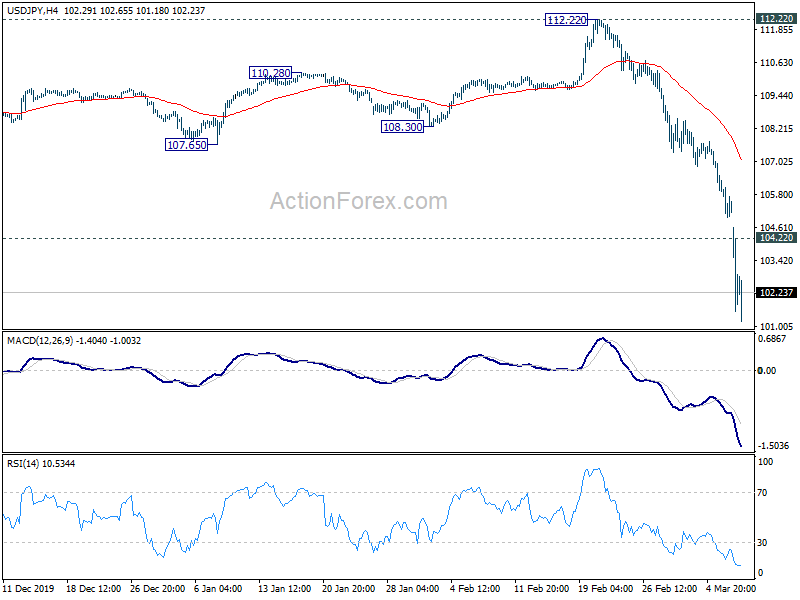

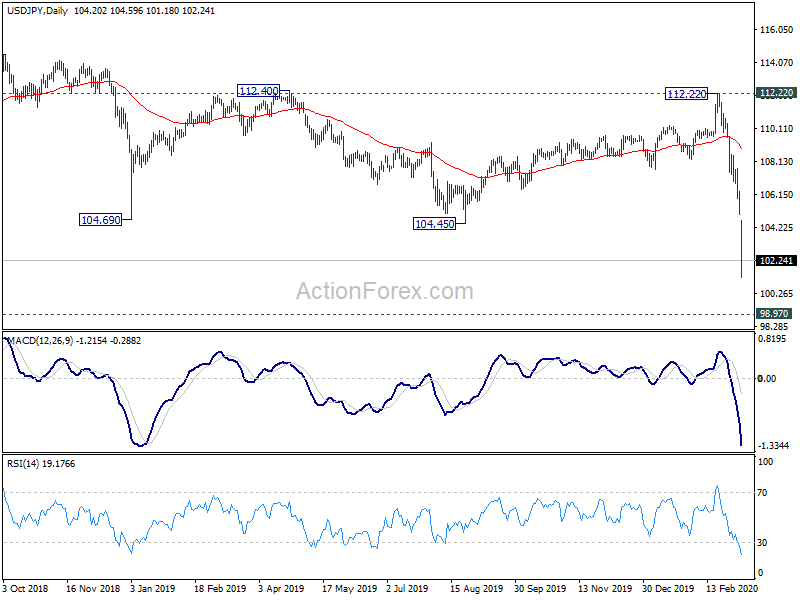

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 104.79; (P) 105.56; (R1) 106.13; More..

Intraday bias in USD/JPY remains on the downside at this point. Current down trend should target next key support level at 98.97. On the upside, above 104.99 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 112.22 resistance to bring fall resumption.

In the bigger picture, fall from 118.65 (Dec 2016) is still in progress. It’s seen as part of a larger consolidative pattern from 125.85 (2015 high). Such decline could could extend through 98.97 (2016 low). For now, risk will remain on the downside as long as 112.22 resistance holds, even in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Feb | 2.10% | 1.90% | 1.90% | |

| 23:50 | JPY | GDP Q/Q Q4 | -1.80% | -1.70% | -1.60% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 | 1.20% | 1.30% | 1.30% | |

| 23:50 | JPY | Current Account (JPY) Jan | 1.63T | 1.66T | 1.71T | 1.85T |

| 05:00 | JPY | Eco Watchers Survey: Current Feb | 27.4 | 35.6 | 41.9 | |

| 06:45 | CHF | Unemployment Rate Feb | 2.30% | 2.30% | 2.30% | |

| 07:00 | EUR | Germany Industrial Production M/M Jan | 3.00% | 1.50% | -3.50% | -2.20% |

| 07:00 | EUR | Germany Trade Balance (EUR) Jan | 18.5B | 18.8B | 19.2B | 19.0B |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Mar | -17 | -11 | 5.2 | |

| 12:15 | CAD | Housing Starts Feb | 210K | 205.0K | 213.2K | 214K |

| 12:30 | CAD | Building Permits M/M Jan | 4.00% | 2.30% | 7.40% | 9.90% |