{kind=link}

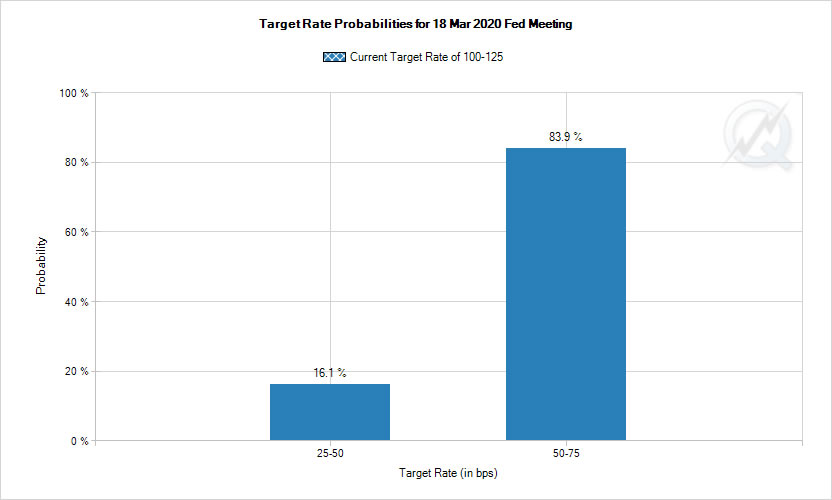

Dollar and Canadian remain the worst performing major currencies for the week and stay pressured. Both Fed and BoC s are perceived as having more room for rate cuts, comparing to, say, ECB and BoJ. Indeed, as the Wuhan coronavirus continues to spread to the world quickly, markets are seeing 100% chance of another -50bps Fed cut in less than two week’s time on March 18. Job data from US and Canada will be the main focuses together, but they’re unlikely to alter respective policy paths.

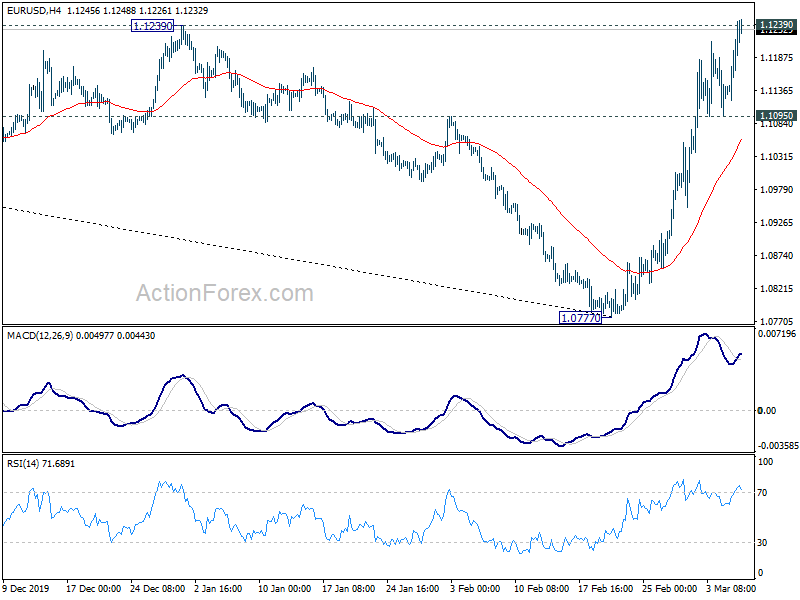

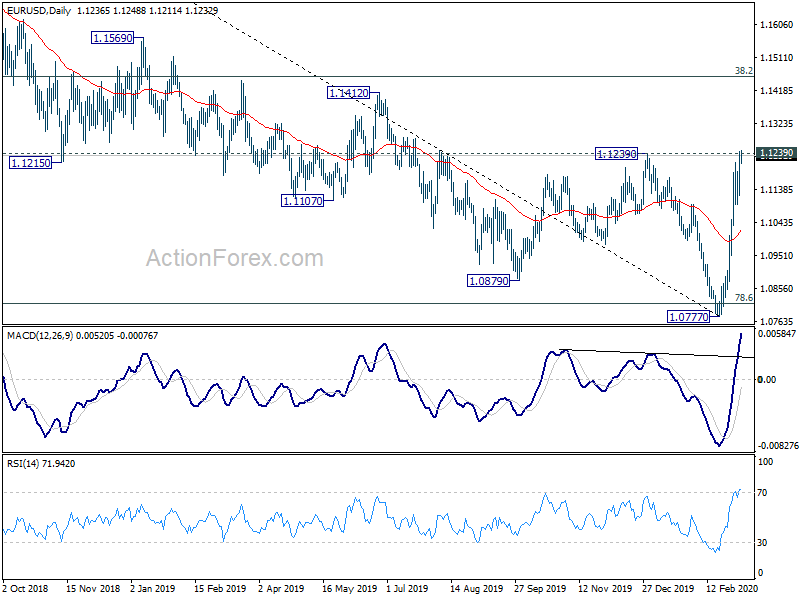

Technically, EUR/USD is now pressing 1.1239 key resistance. Decisive break will confirm medium term bottoming at 1.0777 and turn outlook bullish. Nevertheless, break of 1.1095 minor support will suggest rejection by 1.1239 and retain near term bearishness. EUR/CHF is currently staying in range above 1.0584 temporary low despite mild weakness this week. Outlook remains bearish with 1.0737 resistance intact and break of 1.0584 will resume larger down trend. EUR/GBP also fails to break through 0.8786 key resistance so far. Break of 0.8594 support will suggest rejection by 0.8786 and bring retest of 0.8276 low. If happens, selloff in EUR/CHF and EUR/GBP could trigger a pull back in EUR/USD.

In Asia, currently, Nikkei is down -2.96%. Hong Kong HSI is down -2.15%. China Shanghai SSE is down -0.98%. Singapore Strait Times is down -1.76%. Japan 10-year JGB yield is down -0.0315 at -0.142. Overnight, DOW dropped -3.58%. S&P 500 dropped to 3.39%. NASDAQ dropped -3.10%. 10-year yield dropped to new record low at 0.899 before closing at 0.926, down -0.066.

Global coronavirus cases hit over 98000

Global spread of China’s Wuhan coronavirus continues to accelerate as it’s now affecting 90% countries and territories. Total infections reached 98424, with 3386 deaths. China’s increase in cases continue stabilize at low level, with 143 new cases yesterday to accumulated total of 80552. 30 new deaths were reported, bringing total to 3042.

South Korea remains the most affected country with 6284 cases and 40 deaths. Italy’s cases surged to 3858, with 148 deaths. Iran reported a total of 3513 cases with 108 deaths. Other countries are also catching up, including Germany (545 cases), France (423 cases, 7 deaths), Japan (364 cases, 6 deaths), Spain (282 cases, 3 deaths), USA (226 cases, 13 deaths), Switzerland (120 cases, 1 death), Singapore (117 cases), UK (116 cases, 1 death) and Hong Kong (105 cases). Sweden (94 cases), Norway (91 cases), (Netherlands 82 cases), will break 100 level soon.

Fed Williams: Coronavirus poses evolving risks to the economy

New York Fed President John Williams said the outbreak and subsequent spread of the coronavirus “has brought with it new risks to the economic outlook”. “Repercussions” have been “especially strong” in hardest-hit countries, including China, South Korea, Japan, Italy, and Iran. In the US, there were also reports of “supply disruptions and weakening demand” and concerns around tourism and travel sectors, in particular.

Fed’s -50bps rate cut this week was “strong policy action” that provides “meaningful support to the economy and will help sustain the economic expansion. But “the outlook is evolving and highly uncertain”. He added, “in the weeks and months ahead, we will continue to closely monitor developments and their implications for the economic outlook.”

He also noted Fed is monitoring conditions in the money markets closely. “We remain flexible and ready to make adjustments to our operations as needed to ensure that monetary policy is effectively implemented and transmitted to financial markets and the broader economy.”

Fed Kaplan: It’s wise to act boldly on coronavirus epidemic

Dallas Fed President Robert Kaplan hailed Fed’s emergency rate cut this week to counter the impact of coronavirus epidemic. He told Chicago Council on Global Affairs “it’s wise to act sooner, more boldly, and it increases the likelihood that we’ll need to use less policy ammunition” later on.

Separately, he told Bloomberg, “a week is an eternity”, regarding what Fed would do in the upcoming March meeting. “I am going to be watching very, very carefully the path of diagnosed cases,” Kaplan said. “We’re just going to have to see what the actual developments are over the next 10 days, two weeks. That will be a key factor, yes, I will be using to judge what’s appropriate and whether we can wait longer.”

Minneapolis Fed President Neel Kashkari also said it was “prudent” for Fed’s -50bps rate cut. He added, “this was insurance that we took out because nobody knows how bad the virus is going to be. If everybody pulls back at the same time, that in itself can lead to a recession,” he added.

BoC Poloz: Canada’s resilience could be seriously tested by COVID-19

BoC Governor Stephen Poloz warned in a speech yesterday that the economy’s “resilience” could be “seriously tested by COVID-19”, depending on the “severity and duration of its effects”. Global economy will, “at the very least, be significantly disrupted” by the coronavirus in H1. Consumer and business confidence “could be set back for a longer period of time”, causing growth to “slow more persistently”.

He added that monetary policy can contribute in the current situation by “buffering their effects on consumer and business confidence, thereby helping the economy bridge the situation.” And, “this contribution can be especially powerful when the shock is global and the response is coordinated.” BoC lowered interest rate by -50bps on Wednesday, following the same move by Fed on Tuesday.

Poloz also reiterated that “Governing Council stands ready to adjust monetary policy further if required”. And, “we continue to closely monitor economic and financial conditions, in close coordination with other G7 central banks and fiscal authorities.”

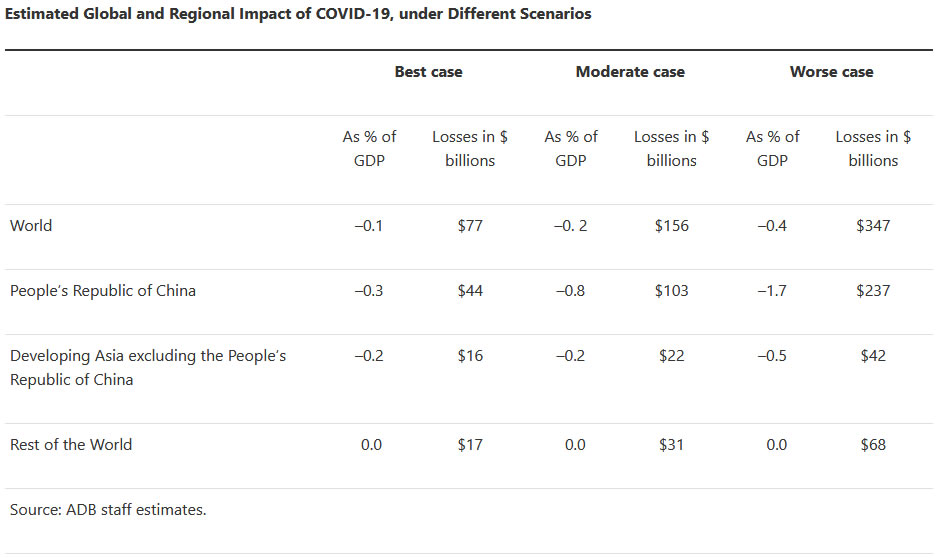

ADB: World to lose 0.4% GDP in worse case scenario of coronavirus

The Asian Development Bank warned that ongoing coronavirus outbreak will have a “significant impact on developing Asian economies”, through numerous channels, including “harp declines in domestic demand, lower tourism and business travel, trade and production linkages, supply disruptions, and health effects”.

“There are many uncertainties about COVID-19, including its economic impact,” said ADB Chief Economist Yasuyuki Sawada. “This requires the use of multiple scenarios to provide a clearer picture of potential losses. We hope this analysis can support governments as they prepare clear and decisive responses to mitigate the human and economic impacts of this outbreak.”

In the “worse case” scenario, the world will lose USD 347B or -0.4% of GDP. China will lose USD 237B, or -1.7%B. Developing Asian excluding China will lose USD 42B or -0.5%.

On the data front

Australia retail sales dropped -0.3% mom in January verus expectation of 0.0% mom. AiG performance of services index dropped to 47, down form 47.4. Japan labor cash earnings rose 1.5% yoy in January versus expectation of 0.2% yoy. Household spending dropped -3.9% yoy, versus expectation of -4..0% yoy.

Looking ahead, Germany factor orders, France trade balance, Italy retail sales and Swiss foreign currency reserves will be fetarued in European session. Main focus will be on US non-farm paryolls but the data is unlikely to alter Fed’s easing path. US trade balance, Canada trade balance, employment and Ivey PMI will also be published.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1160; (P) 1.1202; (R1) 1.1285; More…

Focus remains on 1.1239 key resistance in EUR/USD. Decisive break there should confirm medium term bottoming at 1.0777. Near term outlook will be turned bullish for 1.1456 fibonacci level next. Nevertheless, break of 1.1095 minor support will suggest rejection by 1.1239, and retain near term bearishness. Intraday bias will be turned back to the downside for retesting 1.0777 low instead.

In the bigger picture, as long as 1.1239 resistance holds, larger down trend from 1.2555 (2018 high) is still in favor to extend through 1.0777 low. However, sustained break of 1.1239 will also have 55 week EMA (1.1154) decisive taken out. That should confirm medium term bottoming, with bullish convergence condition in weekly MACD. Further rise could then be seen back to 38.2% retracement of 1.2555 to 1.0777 at 1.1456 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Feb | 47 | 47.4 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jan | 1.50% | 0.20% | 0.00% | -0.20% |

| 23:30 | JPY | Overall Household Spending Y/Y Jan | -3.90% | -4.00% | -4.80% | |

| 0:30 | AUD | Retail Sales M/M Jan | -0.30% | 0.00% | -0.50% | |

| 5:00 | JPY | Leading Economic Index Jan P | 91.9 | 91.6 | ||

| 7:00 | EUR | Germany Factory Orders M/M Jan | 1.50% | -2.10% | ||

| 7:45 | EUR | France Trade Balance (EUR) Jan | -4.9B | -4.1B | ||

| 8:00 | CHF | Foreign Currency Reserves (CHF) Feb | 764B | |||

| 9:00 | EUR | Italy Retail Sales M/M Jan | 0.30% | 0.50% | ||

| 9:00 | Italy | Retail Sales n.s.a Y/Y Jan | 0.90% | |||

| 13:30 | USD | Nonfarm Payrolls Feb | 178K | 225K | ||

| 13:30 | USD | Unemployment Rate Feb | 3.60% | 3.60% | ||

| 13:30 | USD | Average Hourly Earnings M/M Feb | 0.30% | 0.20% | ||

| 13:30 | USD | Trade Balance (USD) Jan | -48.8B | -48.9B | ||

| 13:30 | CAD | Net Change in Employment Feb | 34.5K | |||

| 13:30 | CAD | Unemployment Rate Feb | 5.50% | |||

| 13:30 | CAD | International Merchandise Trade (CAD) Jan | -0.4B | |||

| 15:00 | USD | Wholesale Inventories Jan F | -0.20% | -0.20% | ||

| 15:00 | CAD | Ivey PMI Feb | 57.3 |